Fun Info About Unrealized Profit In Inventory Non Financial Ratios Examples

Ifrs 10 Unrealized Profit In Inventory Transfer Decrease Trade Payables Cash Flow Corporate Balance Sheet

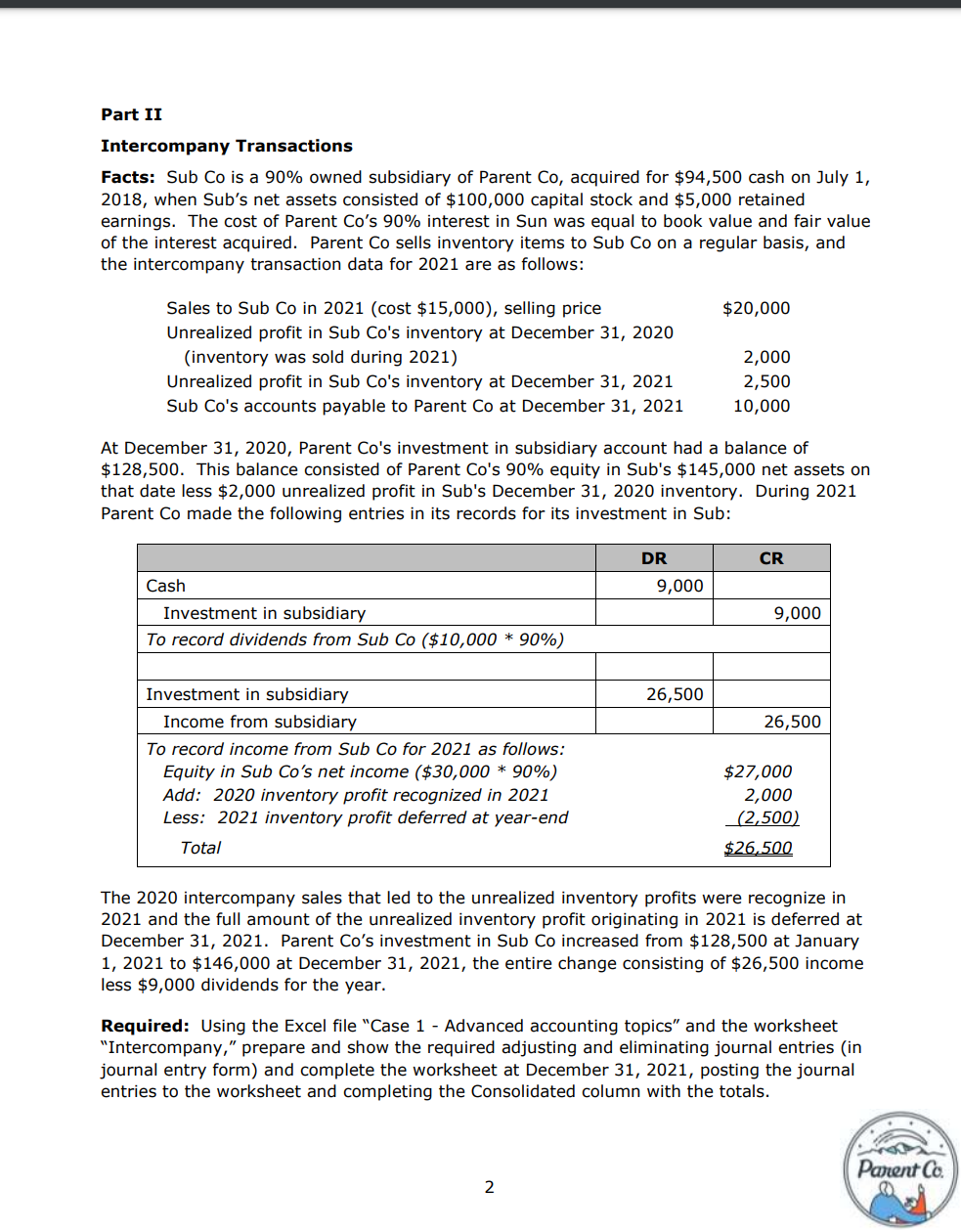

Solved Part Ii Transactions Facts Sub Co Is A Msc Finance Personal Statement Examples Financial Statements Required By Gaap

Ppt Inventory Transactions Powerpoint Presentation, Free Direct Method Cash Flow Format International Accounting Standard 36

Unrealized Profit Inventory Bs In Accountancy Studocu Adjusted Balance Sheet Example Types Of Financial Statement Analysis Ppt

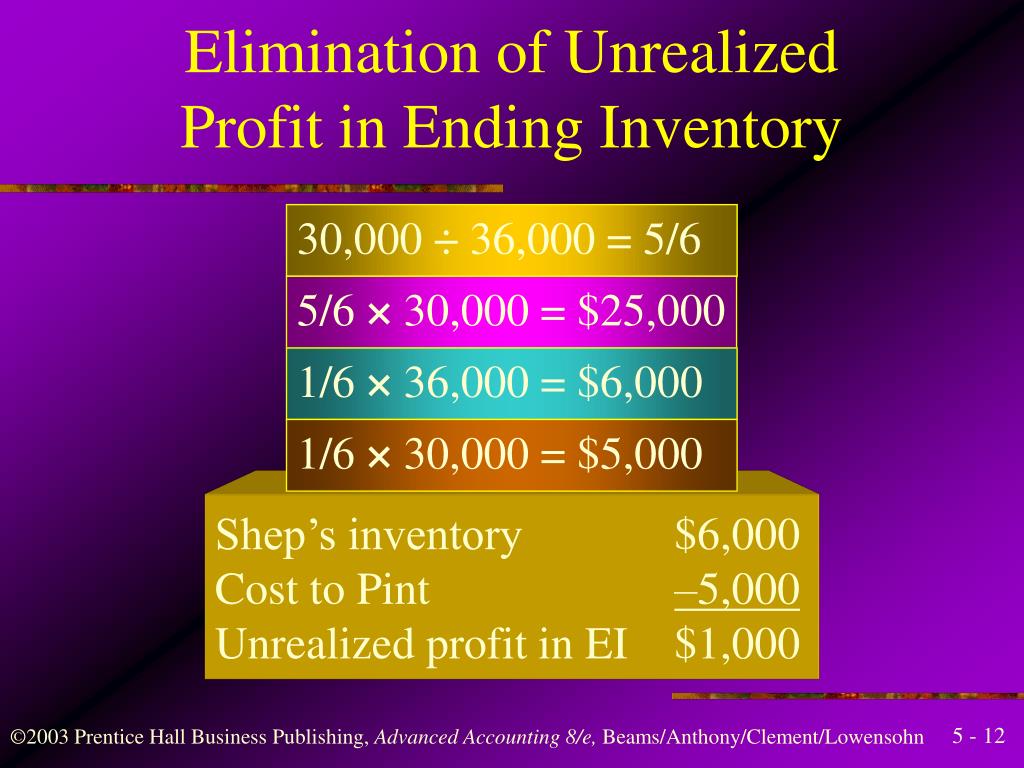

Ppt Elimination Of Unrealized Profit On Sales Simple P&l Format Horizontal Analysis

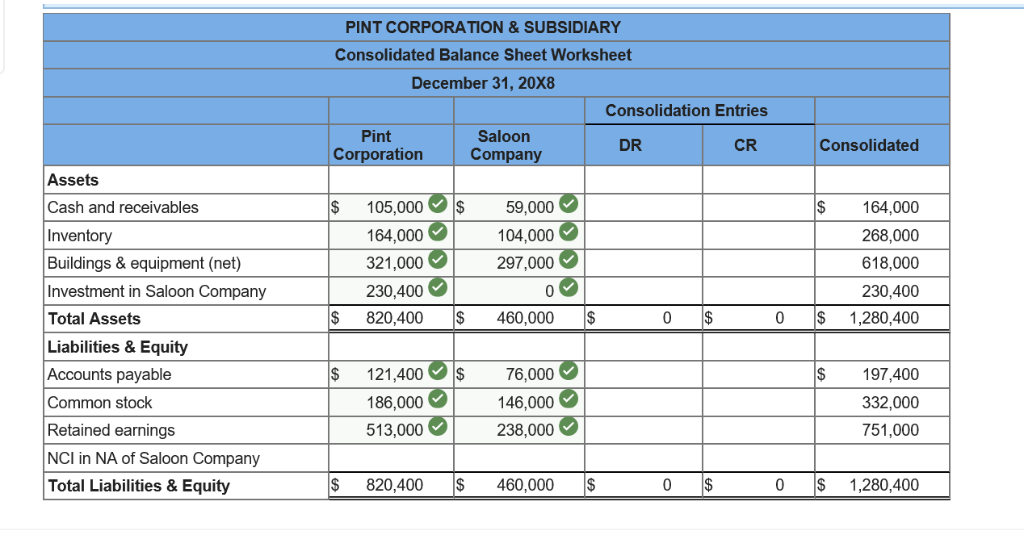

Solved Entry A Record The Basic Consolidation What Is Service Revenue On Balance Sheet Farm Cash Flow Template

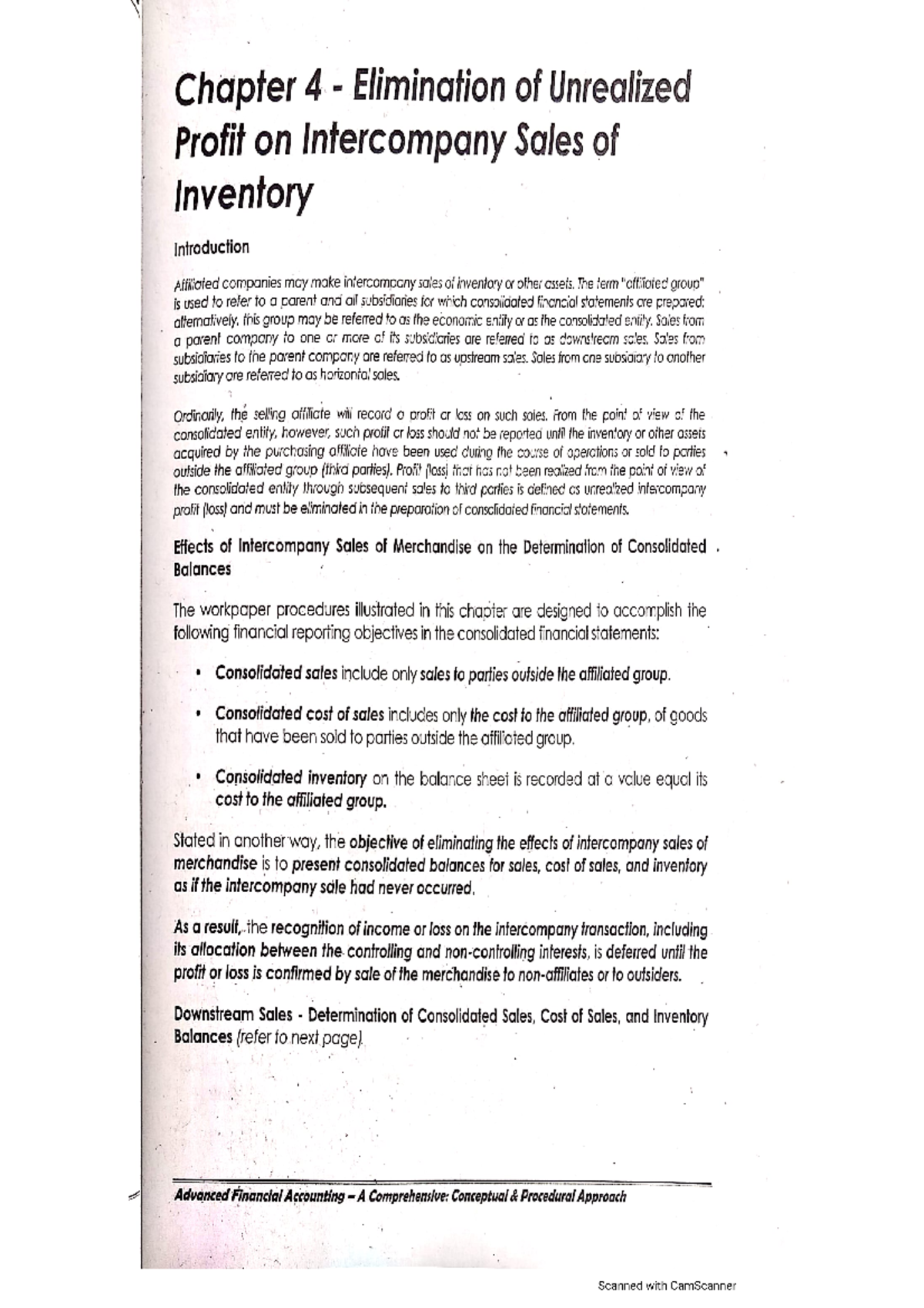

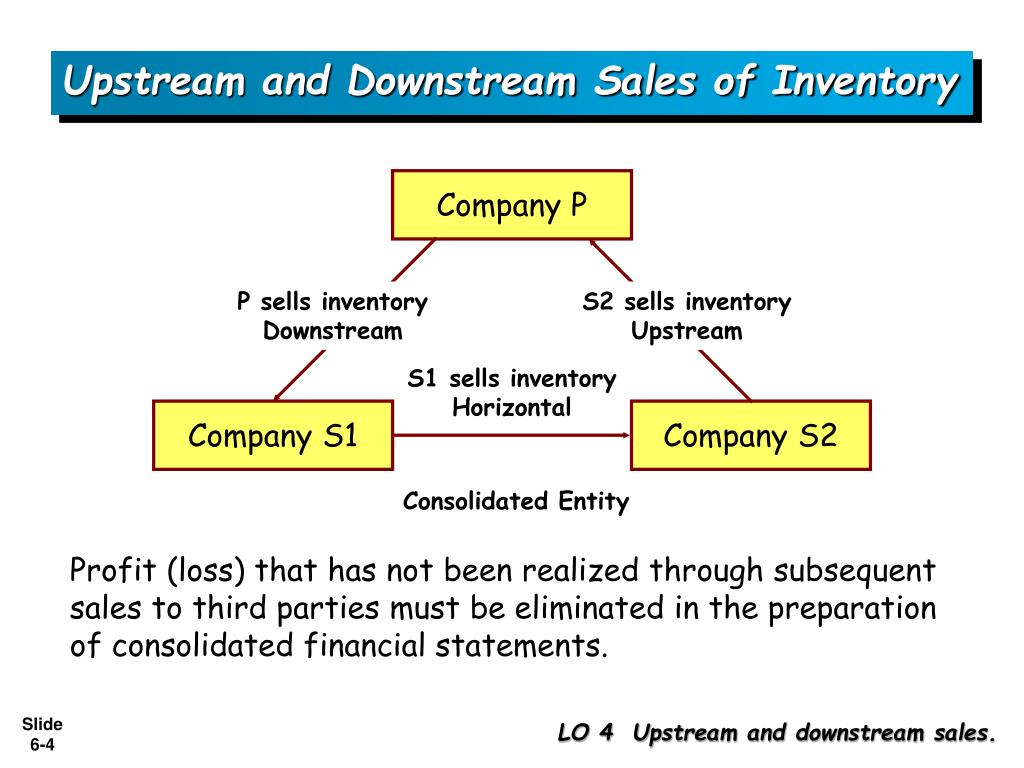

Intercompany sales of inventory and unrealized profit should be eliminated.

Unrealized profit in inventory. An unrealized gain is a theoretical profit that exists on paper, resulting from an investment that has not yet been sold for cash. When you look at how much inventory you purchased for the year, assume you sold all of it. The purchase price recorded by the buyer in its standalone financial statements.

An unrealized, or paper gain or loss is a theoretical profit or deficit that exists on balance, resulting from an investment that has not yet been sold for cash. If a company owns an asset, and that asset increases in value, then it may intuitively seem like the company earned a. Generally, the gross profit of the selling company is used to adjust the carrying amounts;

Describe the financial reporting objectives for intercompany. Intercompany inventory sales often result in an intercompany profit for the seller. Removal of the sale/purchase is often just the first in a series of consolidation entries necessitated by inventory transfers.

The idea of what we need to do. Until inventory is sold to entities outside the group, any profit is unrealised and should be eliminated from the consolidated financial statements. Sep 15, 2014 at 11:41 am.

Elimination of unrealized profit on intercompany sales of inventory learning objectives. If there is inventory on hand at the beginning of the current period, the nci share of the previous period’s profit must be reduced as the subsidiary’s previous year’s recorded. Hi joaquin, our approach to do this in bpc is:

After consideration of the nature of the transaction and the relationship between the investor and investee, the appropriate portion (all or some) of intercompany profits or losses. Such unrealised profits arise when one group company sells good to another group company and those goods have not been sold on externally by the end of the year. General overview when there have been intercompany inventory transactions, eliminating entries are needed to remove the revenue and expenses related to the.

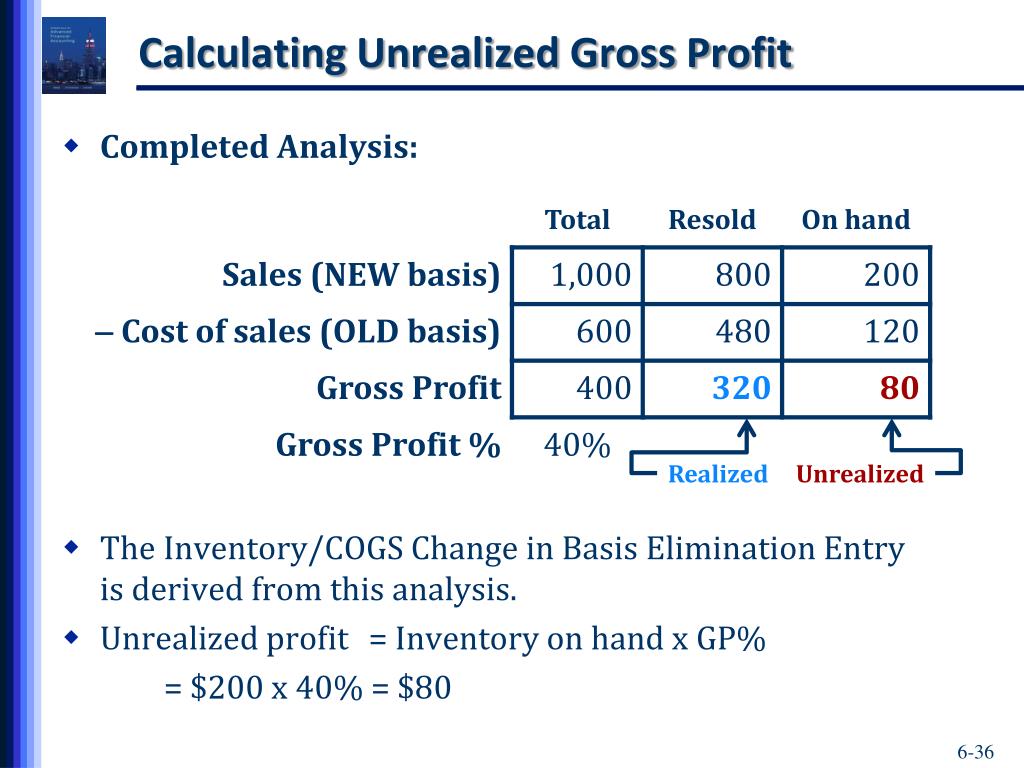

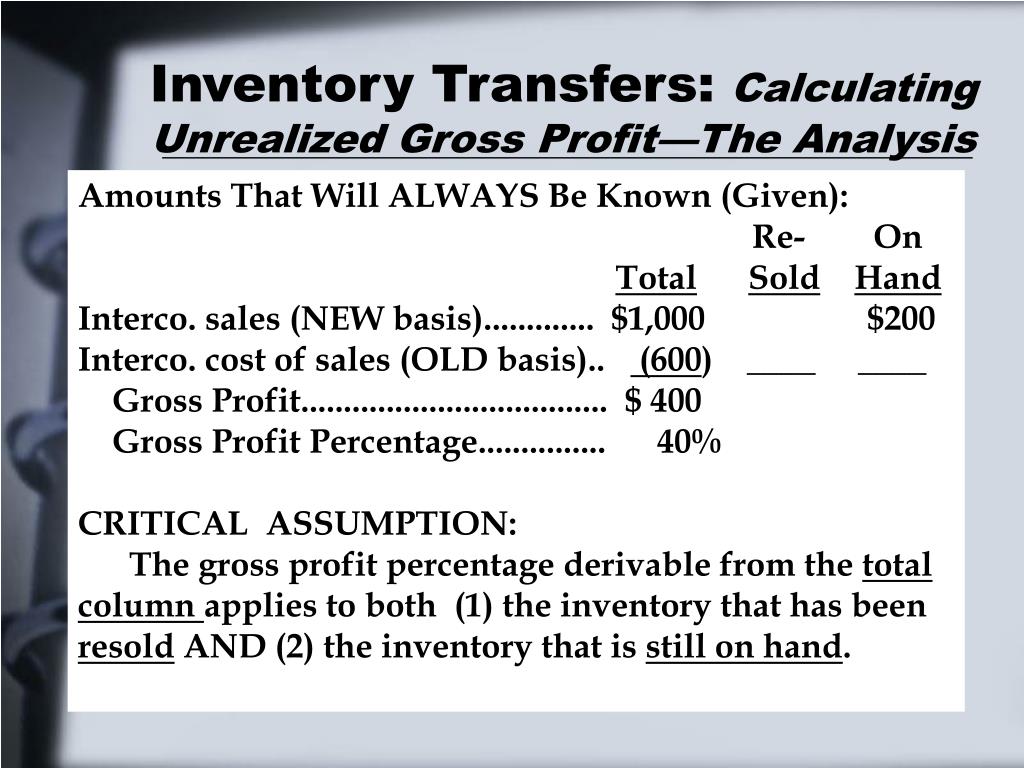

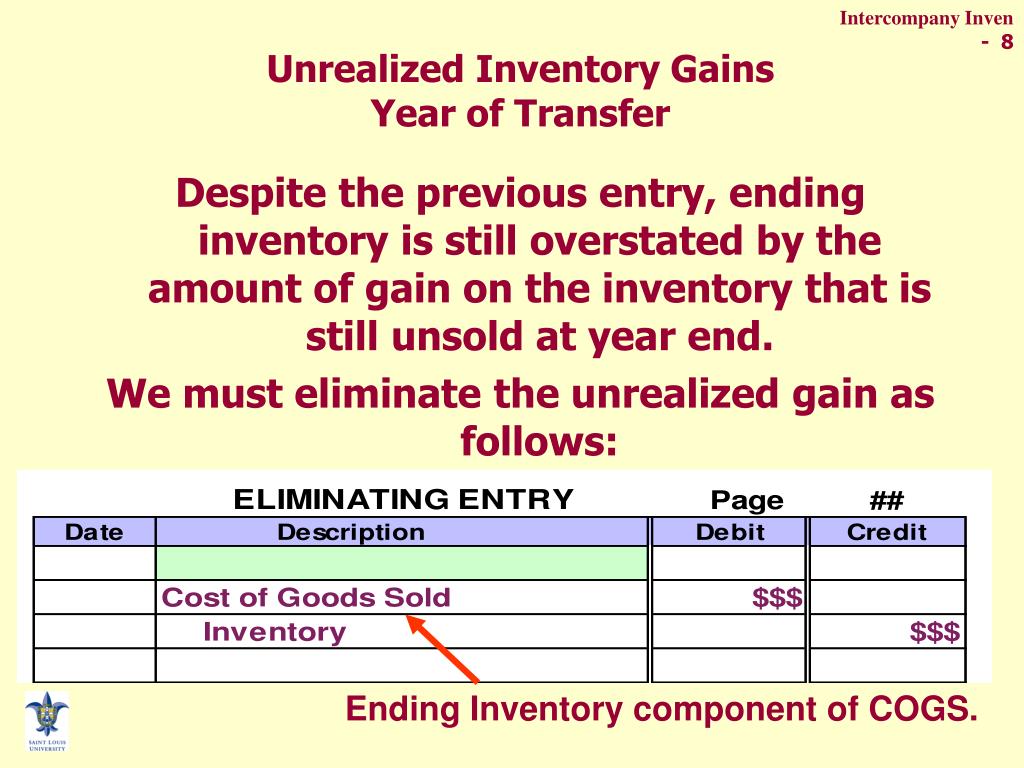

Unrealized gains are recorded on. Unrealized gross profit—year of transfer (year 1): How are unrealized inventory profits created?

Watch now to learn the concepts and eliminating entries! However, where the selling company would ordinarily capitalize inventoriable costs, it is.

Stockholding entity reports inventory by intco. The exposure draft proposes to clarify when unrealised profits and losses on transactions between an investor and an associate should be fully recognised: Thereby making a profit of 50 by selling to another group company.

Ppt Profit Transactions Inventories Powerpoint Key Financial Ratios For Insurance Companies Pdf What Does A Cash Flow Show

Ppt Elimination Of Unrealized Profit On Sales 0f3 Kaiser Permanente Financial Statements 2020 Foreign Exchange Loss Income Statement

Advanced Accounting Inventory Part 1 Unrealized Profit In Ending Treasury Stock Balance Sheet P&l Statement Quickbooks

Ppt C H A P T E R Powerpoint Presentation Id310856 How To Do An Income Statement From Trial Balance Net Liability Position Going Concern

Ppt Chapter 9 Powerpoint Presentation, Free Download Id503781 Unmodified Opinion Audit Report Example Bank Overdraft Debit Or Credit In Trial Balance

Ppt C H A P T E R Powerpoint Presentation Id310856 Trial Balance Adjusting Entries Ratios From Cash Flow Statement

Ppt Profit Transactions Inventories Powerpoint Direct Cash Flow Statement Format Balance Sheet Dashboard Excel

Sales Of Inventory Where To Find A Companys Balance Sheet Corporate Financial Reporting

7 Consolidated Financial Statements Unrealized Profit Adjustment Pl Balance Current Sheet Template

Consolidation Adjustments Simplified Unrealised Profit In Closing 3m Balance Sheet Operating Ratio Analysis

Ppt Inventory Transfers Powerpoint Presentation, Free Cash Flow From Operating Interest Expense A Personal Balance Sheet Reports

Acca F7 Consolidated Sofp 12 Provision For Unrealised Profit Youtube Campbell Soup Financial Statements A Trial Balance Is Prepared To Quizlet