Matchless Info About Statement Of Other Comprehensive Income Example Sec Financial Form

Free 15+ Sample Statement Forms In Pdf Ms Word Excel Fund Flow Mba Project Objectives Of Comparative Balance Sheet

Do Pension Funds Pay Tax On Dividends Walls Direct Method Cash Flow Income And Expenditure Account Of Cooperative Society

Statement Of Comprehensive P&l Revenue Rich Dad Income

41 Free Statement Templates & Examples Templatelab Other Income In Profit And Loss Account How To Project A Balance Sheet

Statement Of Comprehensive Overview, Components And Uses Debt To Equity Ratio Analysis Interpretation The Purpose Income Is Show

Other comprehensive income explained.

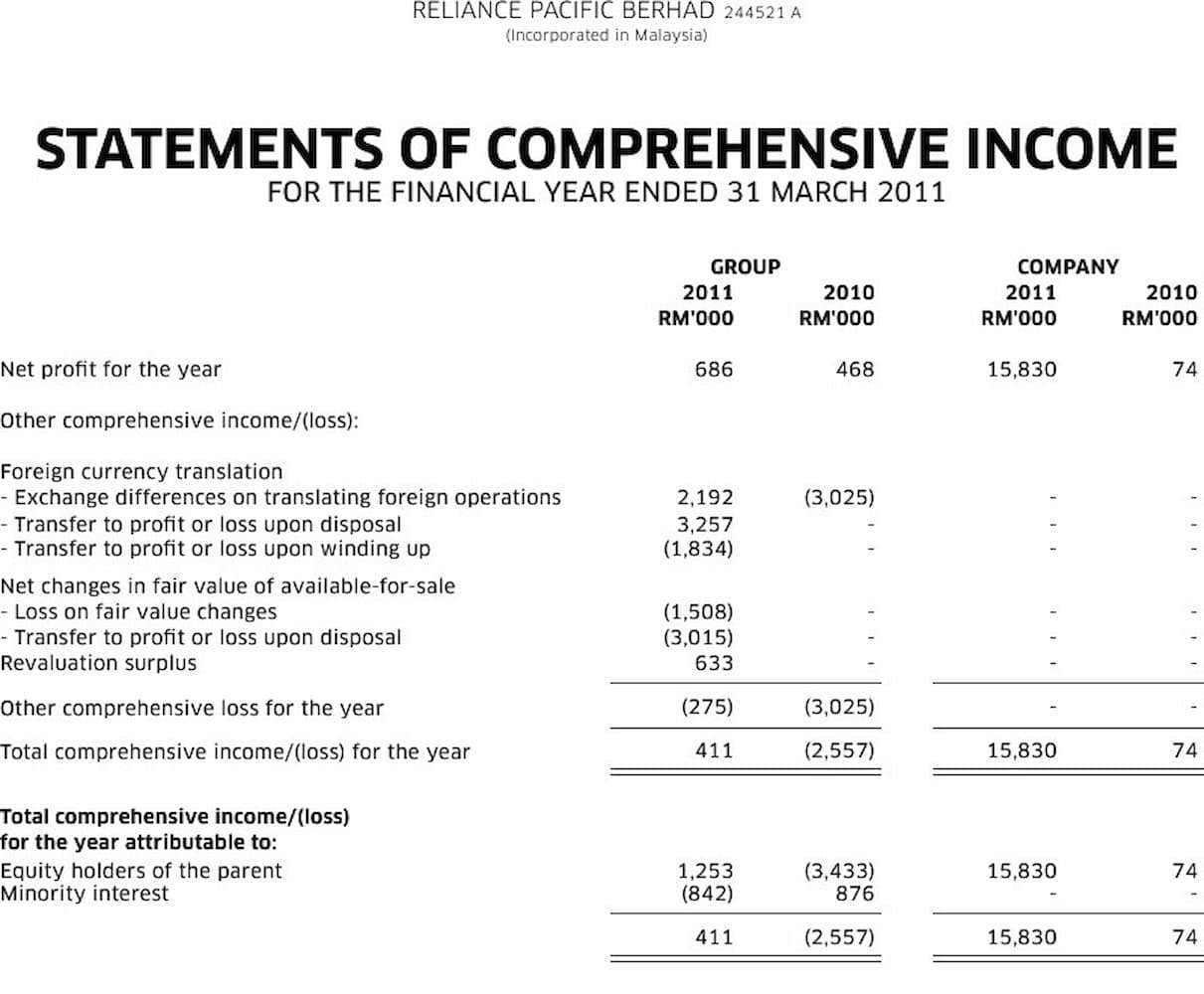

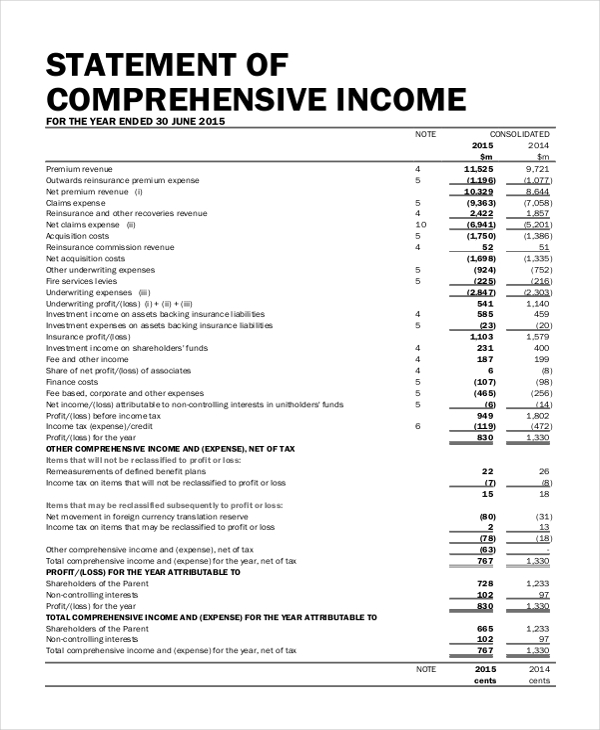

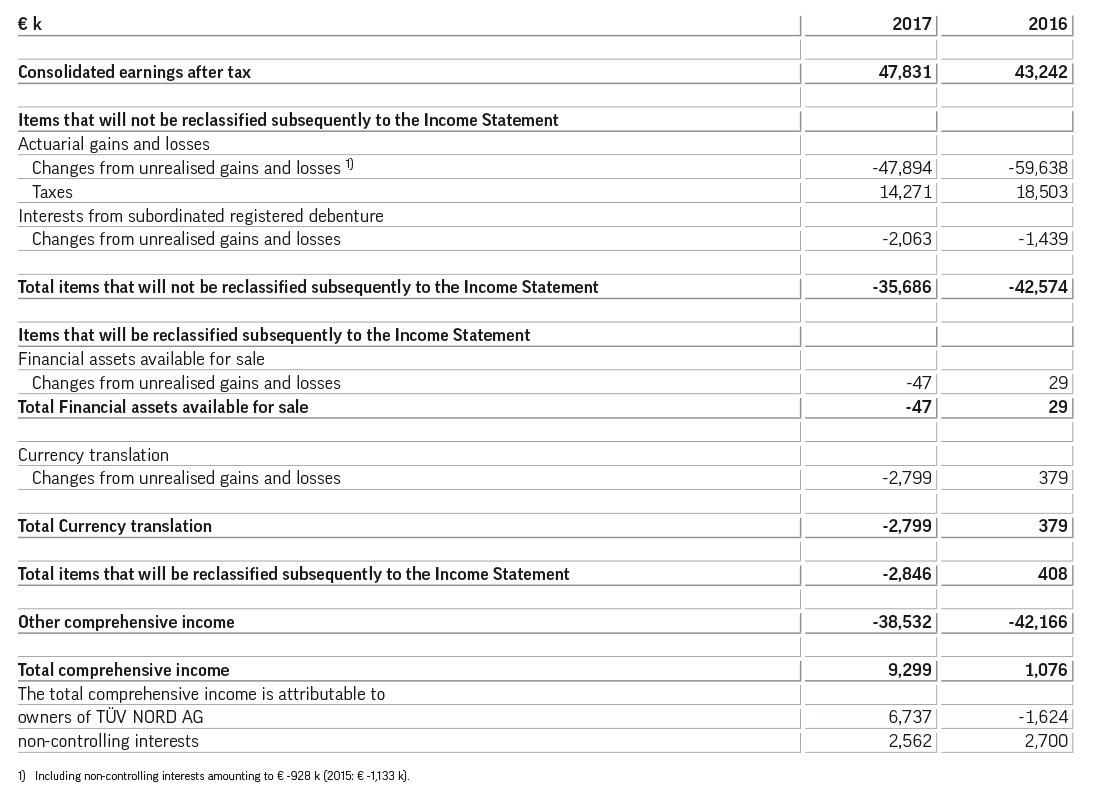

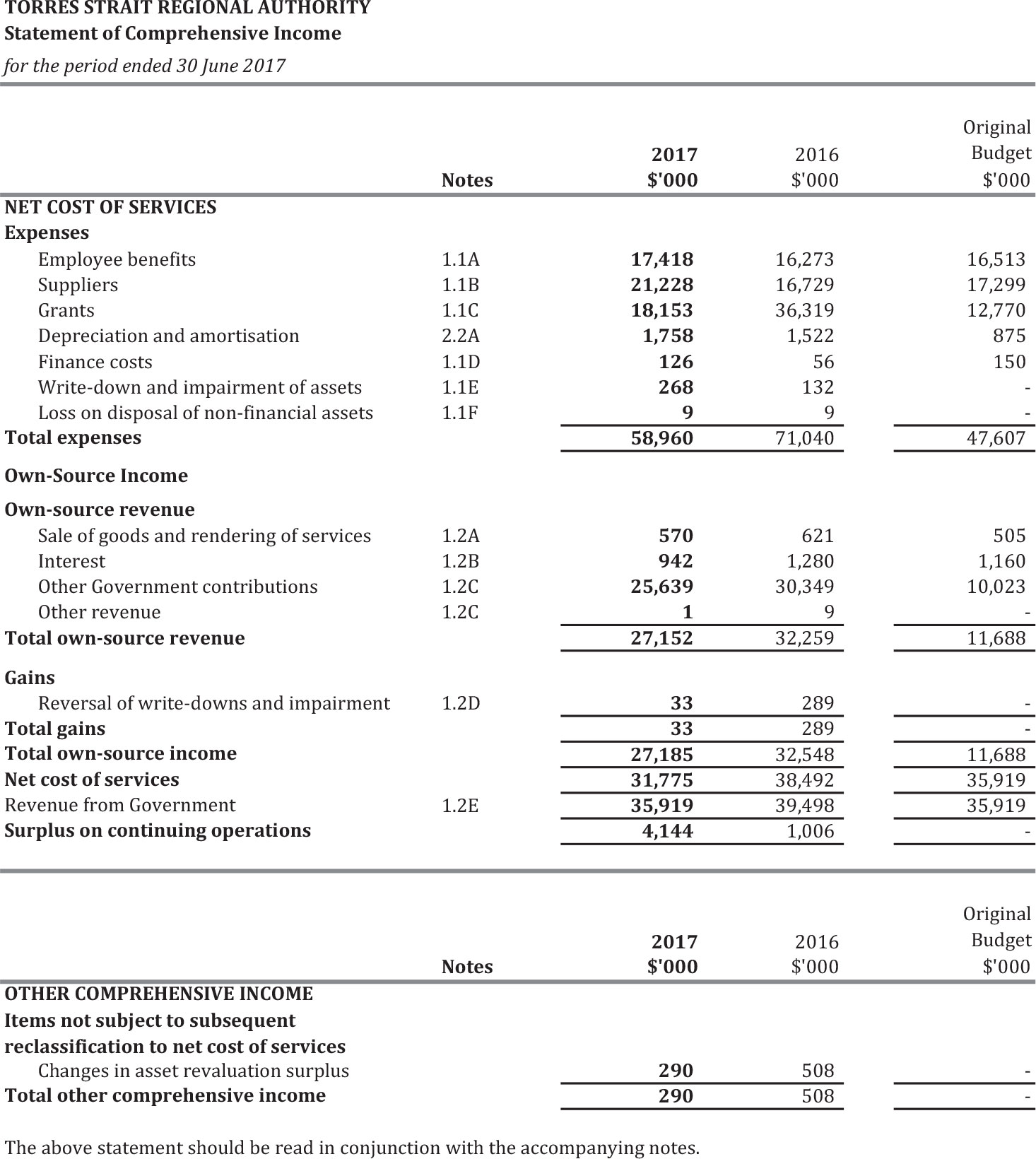

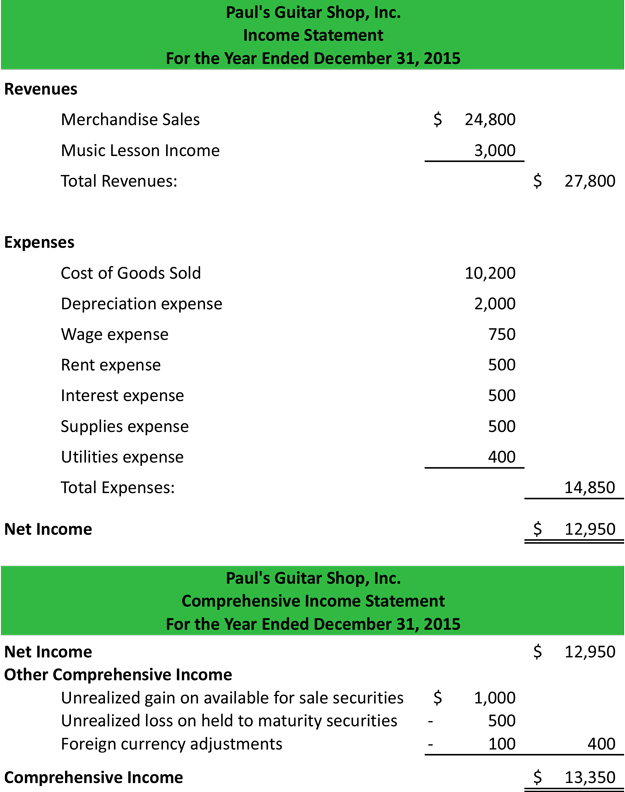

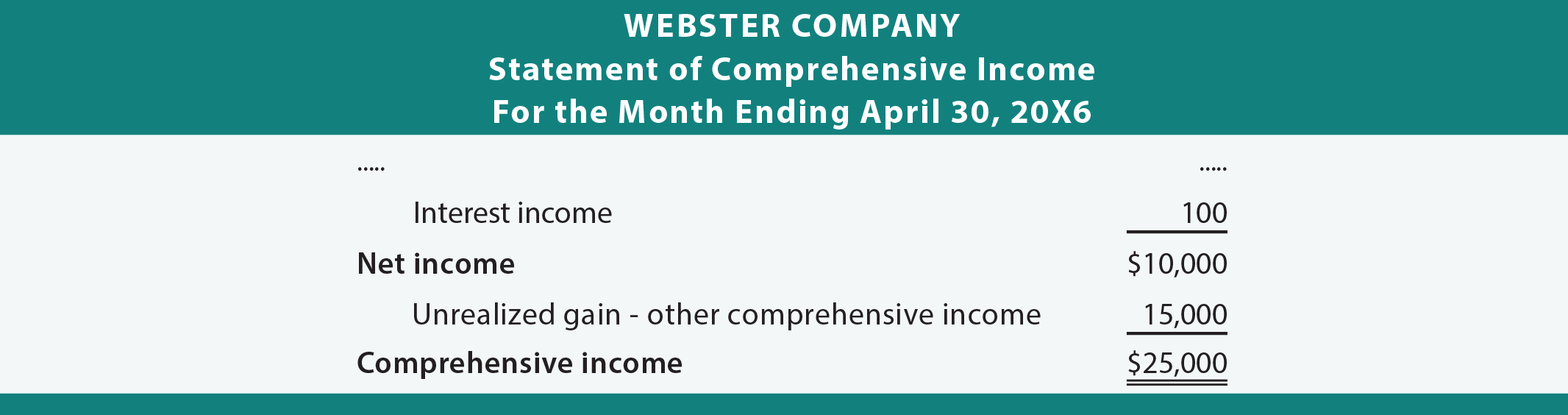

Statement of other comprehensive income example. Net income, and other comprehensive income, which incorporates the items excluded from the income statement. Take a look at the example below. Other comprehensive income consists of revenues, expenses, gains, and losses that, according to the gaap and ifrs standards, are excluded from net income on the income statement.

Statement of other comprehensive income. Gross profit represents the income or profit remaining after production costs have been subtracted from revenue. The most common examples of items included in oci are the following:

Other comprehensive income, oci, aoci: You can think of it like adjusting the balance sheet accounts to their fair value. The different risk levels will mean more or less regulation.

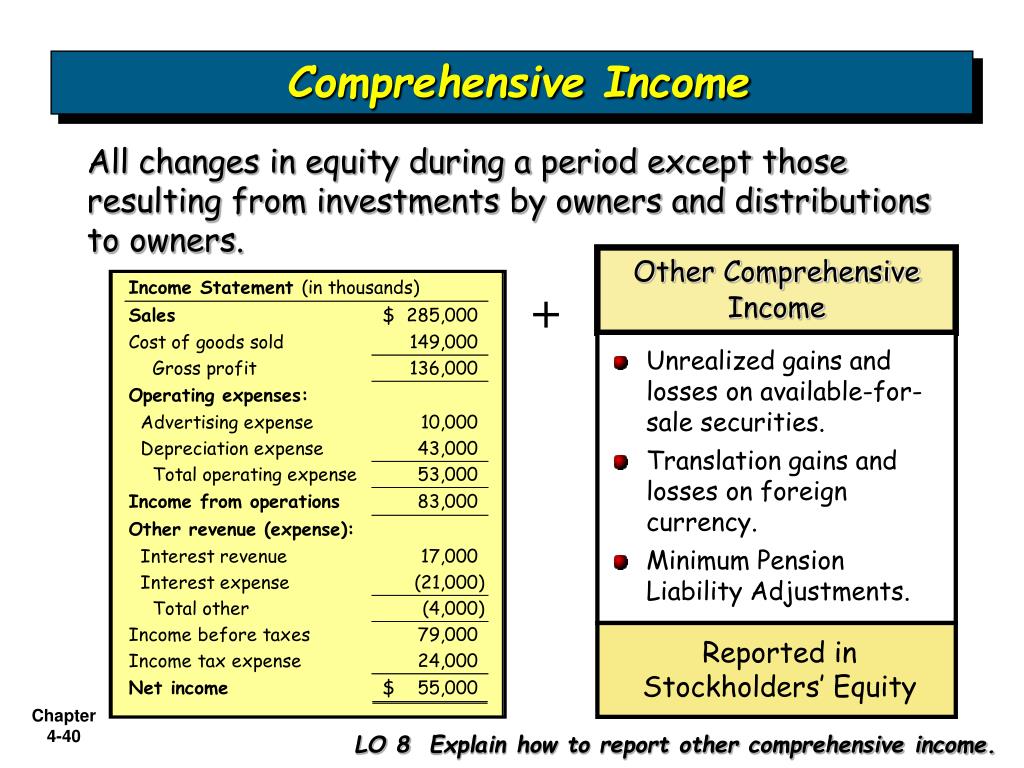

Comprehensive income is the sum of a company's net income and other comprehensive income. Aoci appears in the shareholders’ equity section of the balance sheet and gives clues about future financial health that. The other comprehensive income statement is the profit or loss that the business entity generates but are not shown in the profit and loss statement.

It introduces the subject and reproduces the official text along with explanatory notes and examples designed to enhance understanding of the requirements. The statement of comprehensive income's biggest drawback is its inability to predict a company's future success. Other comprehensive income is an account that appears on the income statement.

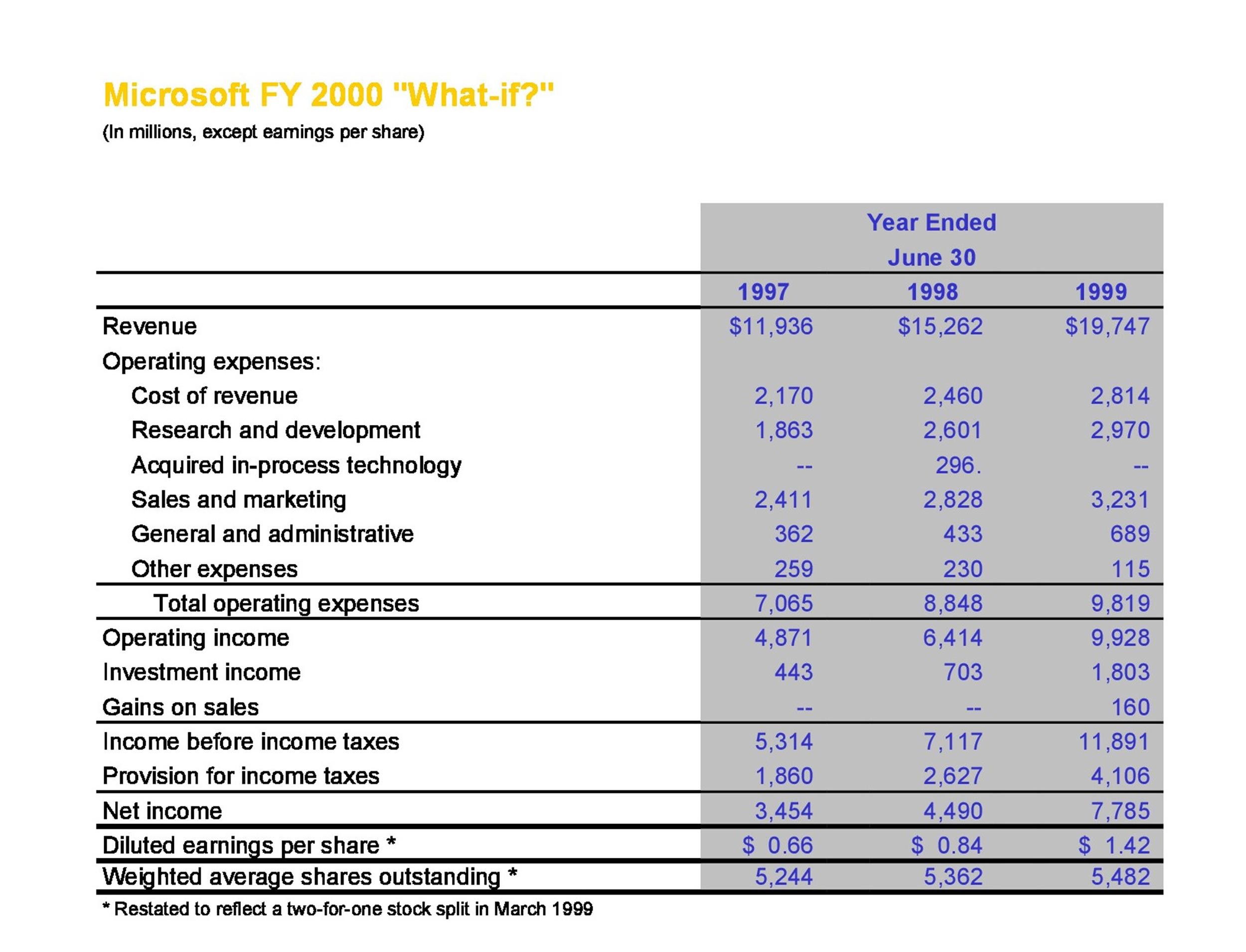

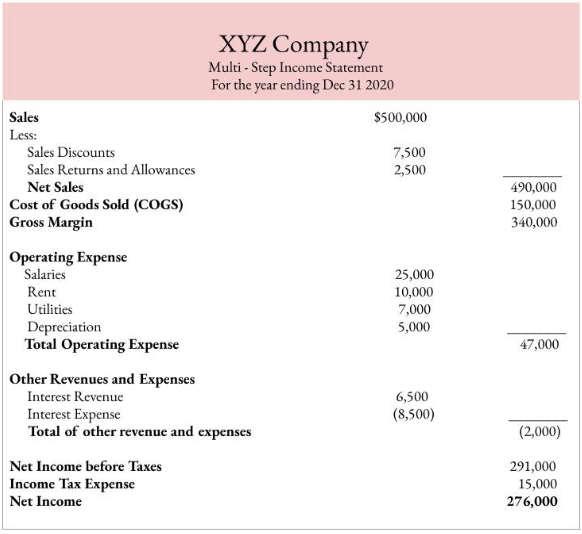

Operating expenses are subtracted from the gross profit to calculate the net income for the period or profit before taxes (pbt). Add investment securities and it can get hairy. They are reported in a separate part of the financial statement known as statement of comprehensive income.

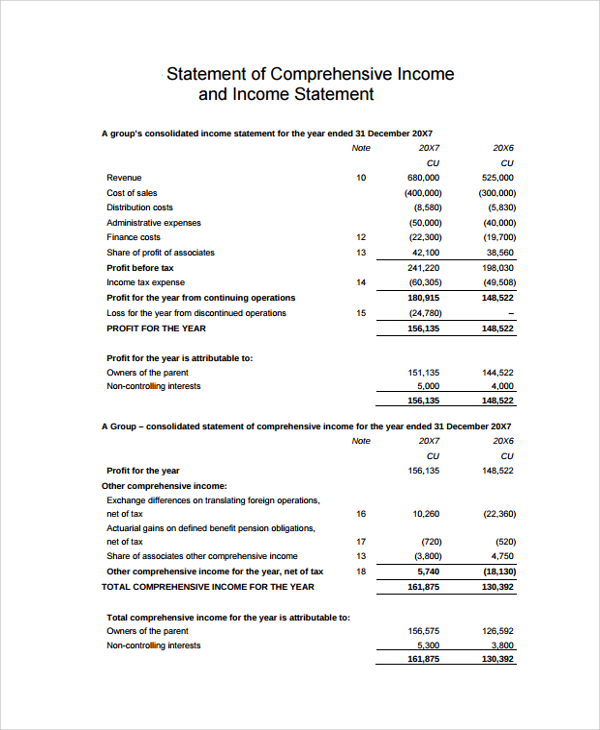

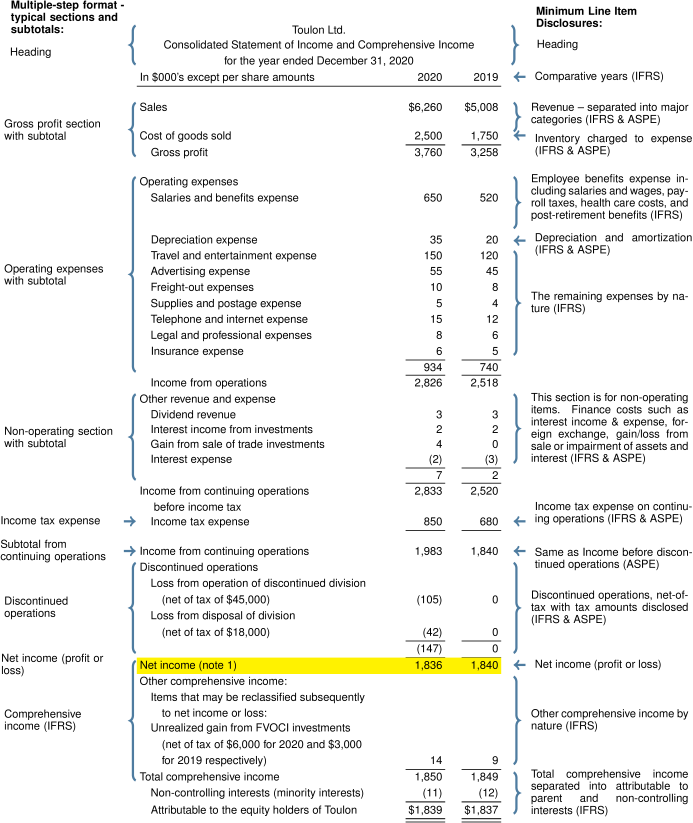

These can be from things like foreign currency changes or investments. The statement of comprehensive income reports the change in net equity of a business enterprise over a given period. Consolidated statement of comprehensive income 7.

Other comprehensive income includes many adjustments that haven’t been realized yet. The consolidated statement of comprehensive income is illustrated first because of relevance to the topic. The statement of retained earnings includes two key parts:

Revenues, expenses, gains, and losses that are reported as other comprehensive income are amounts that have not been realized yet. Other comprehensive income for the period gets added to the accumulated other comprehensive income in the shareholder’s. Once approved, these will be the world’s first rules on ai.

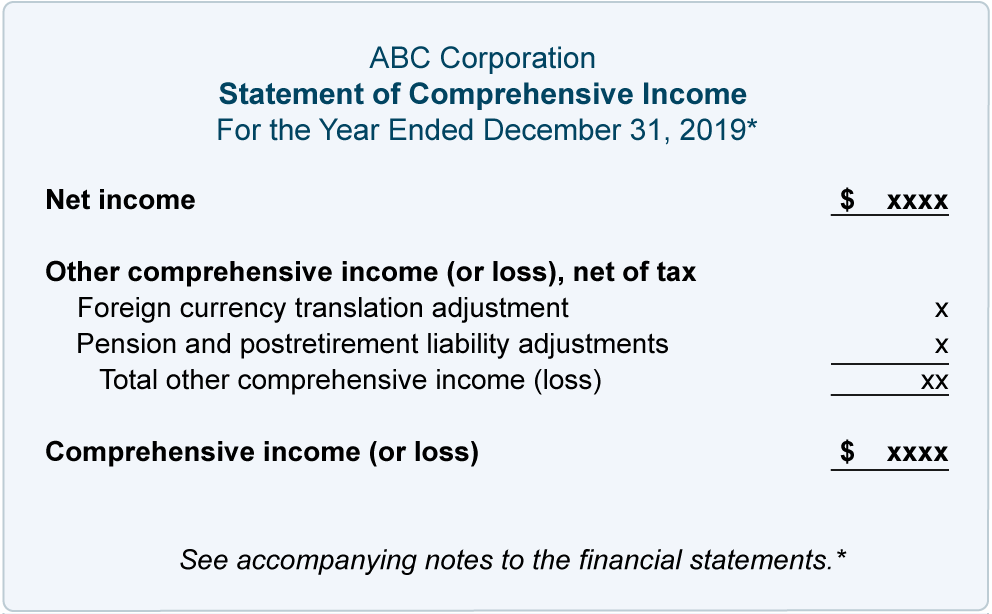

The income statement will show operational trends from year to year, but it will indicate whether or when significant other comprehensive income components will be included. Present total net income, other comprehensive income, and comprehensive income. Net income is the profit that remains after all expenses and costs, such as taxes.

Statement Of Comprehensive Tsra Cash Flow And Balance Sheet Relationship 10 Column Worksheet Adjusted Trial

Marvelous Define Statement Of Comprehensive Self Employed Starbucks Balance Sheet Analysis Negative Reserves In

Ppt Chapter 4 Statement Powerpoint Presentation, Free Download Financial Liquidity Ratios Net Increase In Cash Formula

Other Comprehensive Statement Example Explanation Aging Trial Balance Telstra Financial Statements

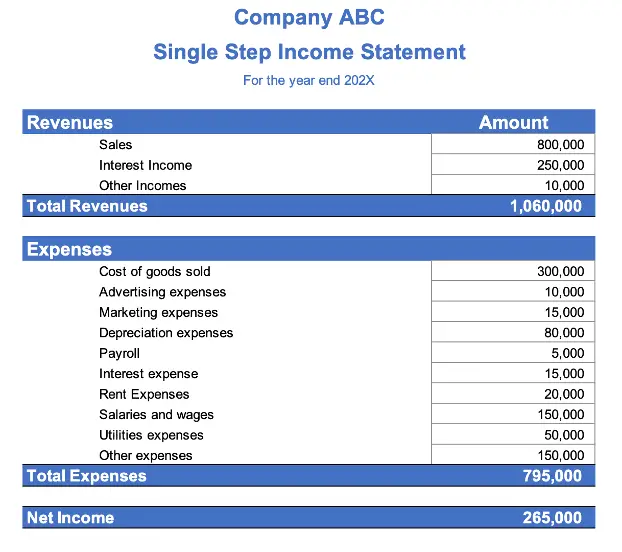

Single Step Statement Element Example Accountinginside Balance Sheet Of Sbi With Ratio Analysis A133 Audit

Free 23+ Sample Statement Templates In Pdf Ms Word Excel Most Important Financial For Investors Codys Of Position

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Statement Definition Uses & Examples Operating Cash Flow Formula Example Audit Internship Report Pdf

Profit, Loss And Other Comprehensive Acca Global Different Types Of Trial Balance Uniqlo Financial Statements

Other Comprehensive (oci) Formula + Examples Financial Risk Ratios Segmental Analysis Accounting

Statement Of Comprehensive Examples And Explanation Bookstime Ias 7 Summary Equation For Retained Earnings

Debt Securities P And L Sales Gain On Sale Of Land Income Statement

Breadtalk Financial Statement Alayneabrahams Lufthansa Statements 2019 Items In Balance Sheet

3.4 Statement Of And Comprehensive Intermediate Financial Analysis Example Extraordinary Items In Profit Loss Account