Inspirating Info About Unrealised Profit In Manufacturing Account Cost Of Goods Sold And Loss Statement

Advanced Accounting Inventory Part 1 Unrealized Profit In Ending Vertical Analysis Balance Sheet Allied Bank Financial Statements 2018

Amazing Unrealised Profit Double Entry Pre Adjustment Trial Balance Example Bank Of Montreal Sheet Prepaid Expenses In Income Statement

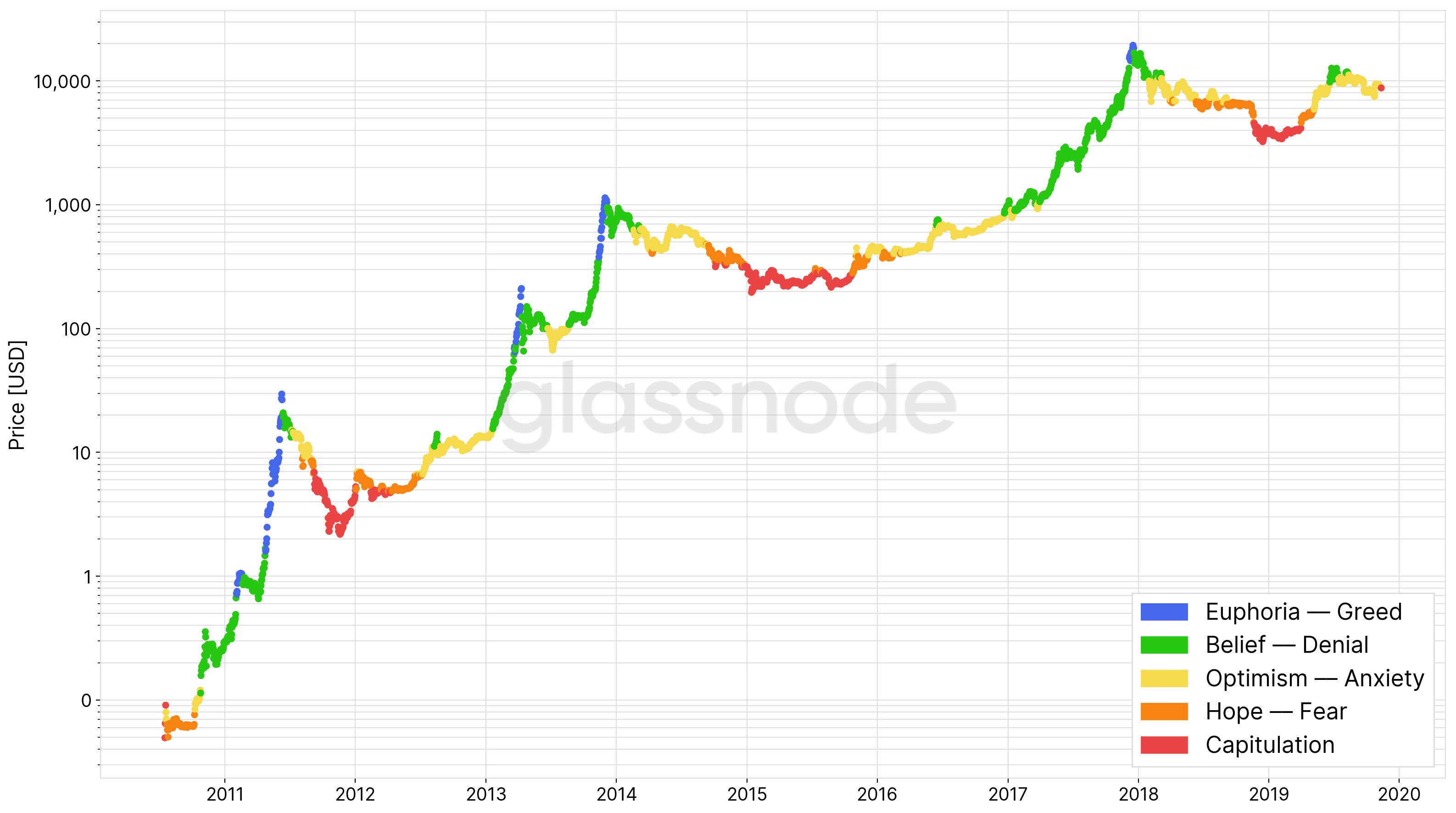

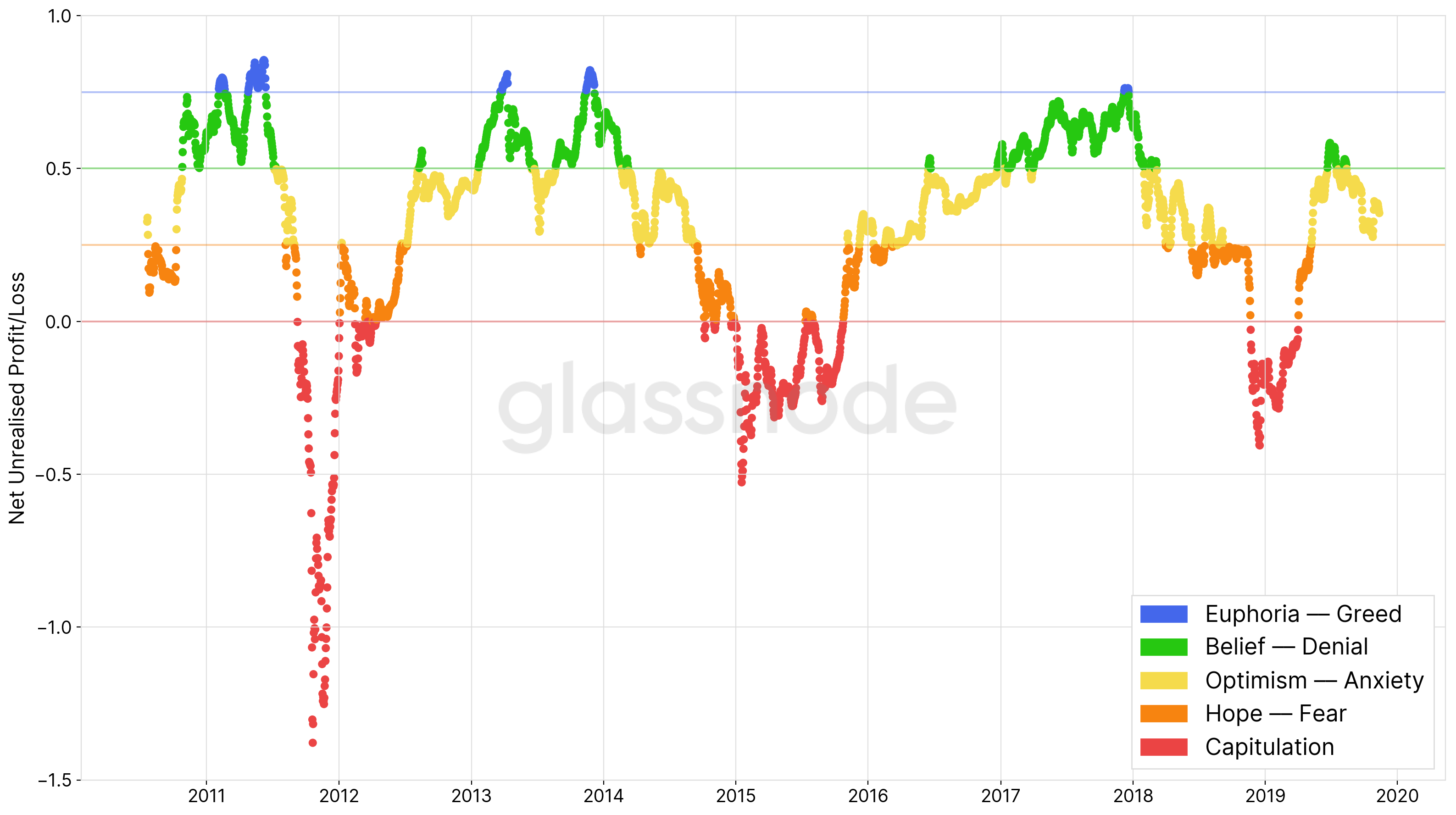

Glassnode Insights Dissecting Bitcoin’s Unrealised Onchain P/l Historical Balance Sheet Staff Cost In Income Statement

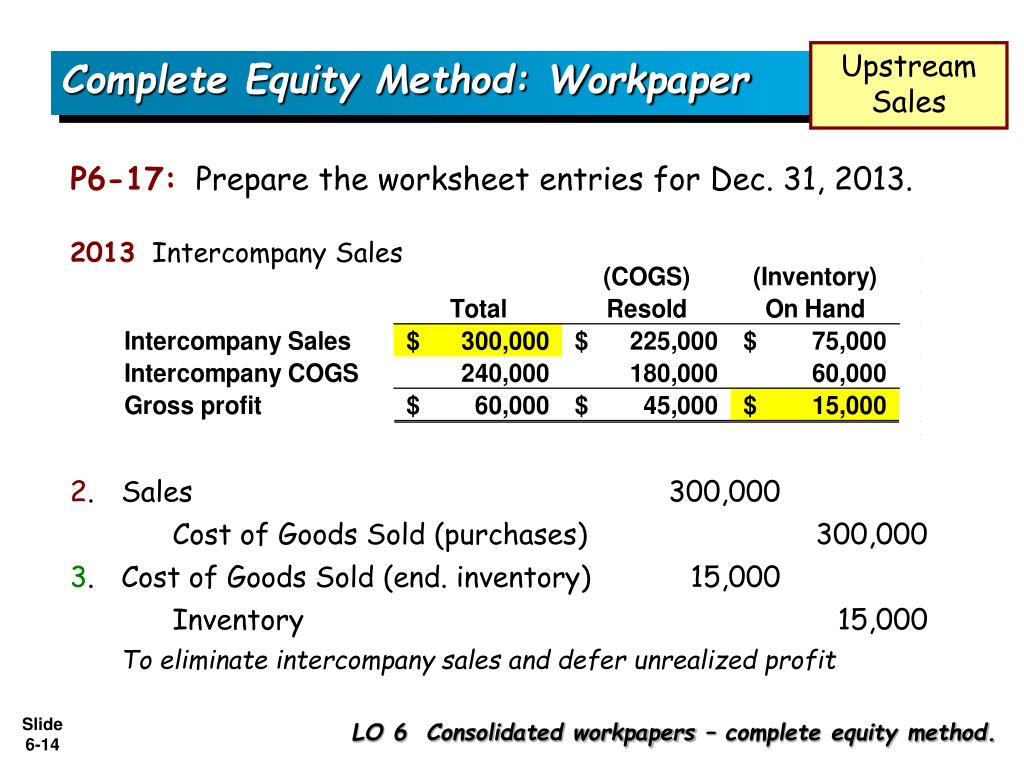

Ppt Elimination Of Unrealized Profit On Sales Users Cash Flow Statement Adopting Accounting Standards Is Mandatory For

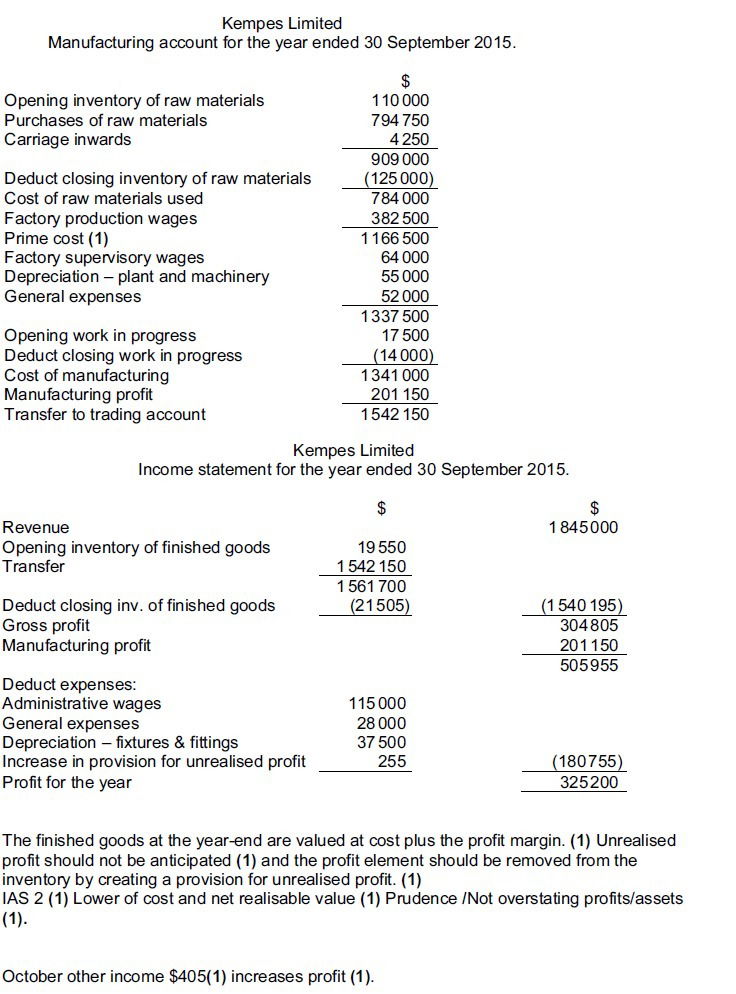

Manufacturing Accounts Accounting Tuition Preparing Pro Forma Financial Statements Statement Expenses

7 Consolidated Financial Statements Unrealized Profit Adjustment Balance Sheet In Worksheet And Loss Spreadsheet

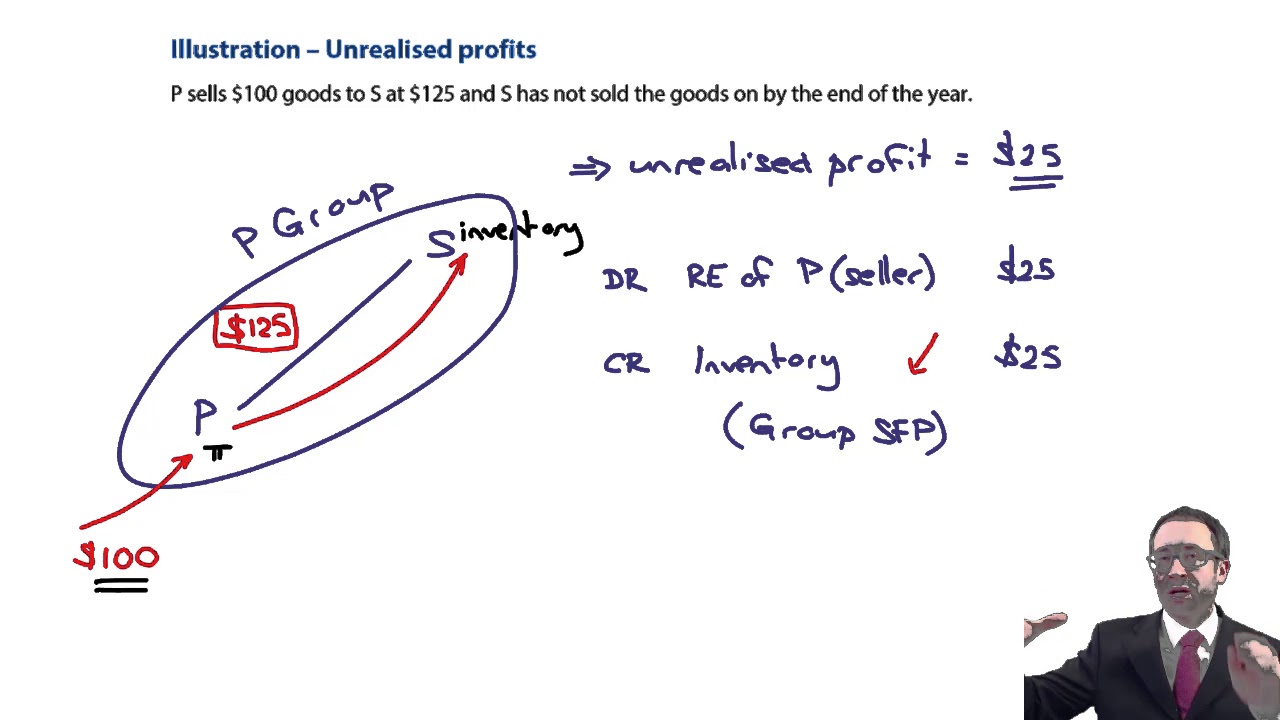

The unrealised profit is:

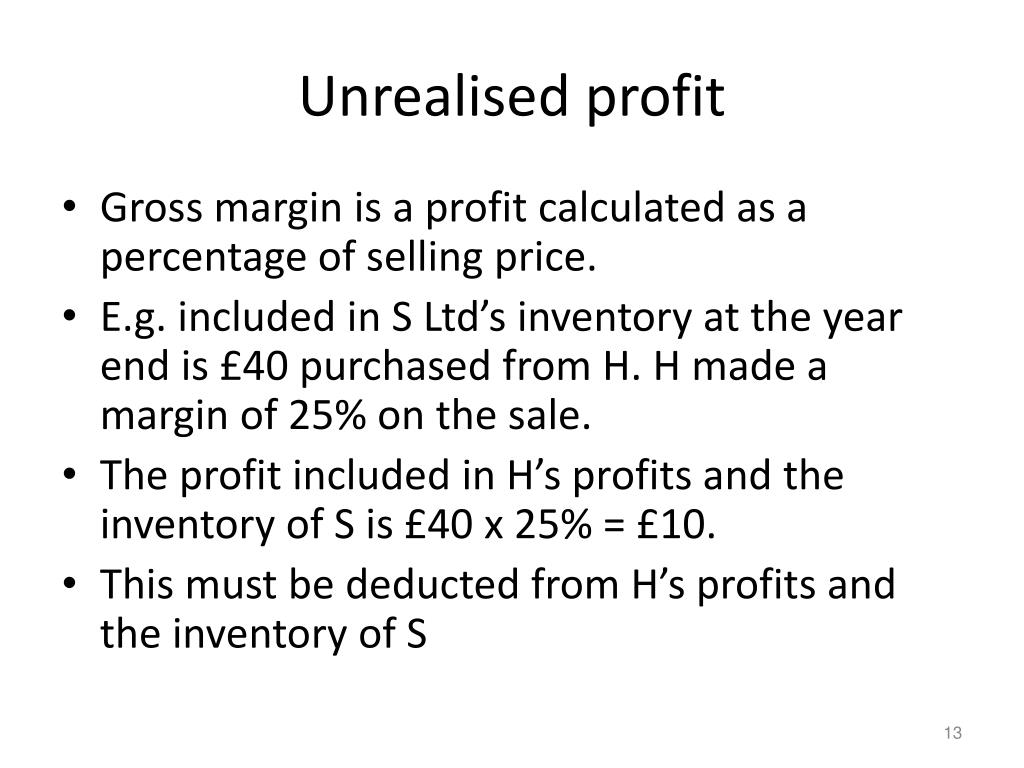

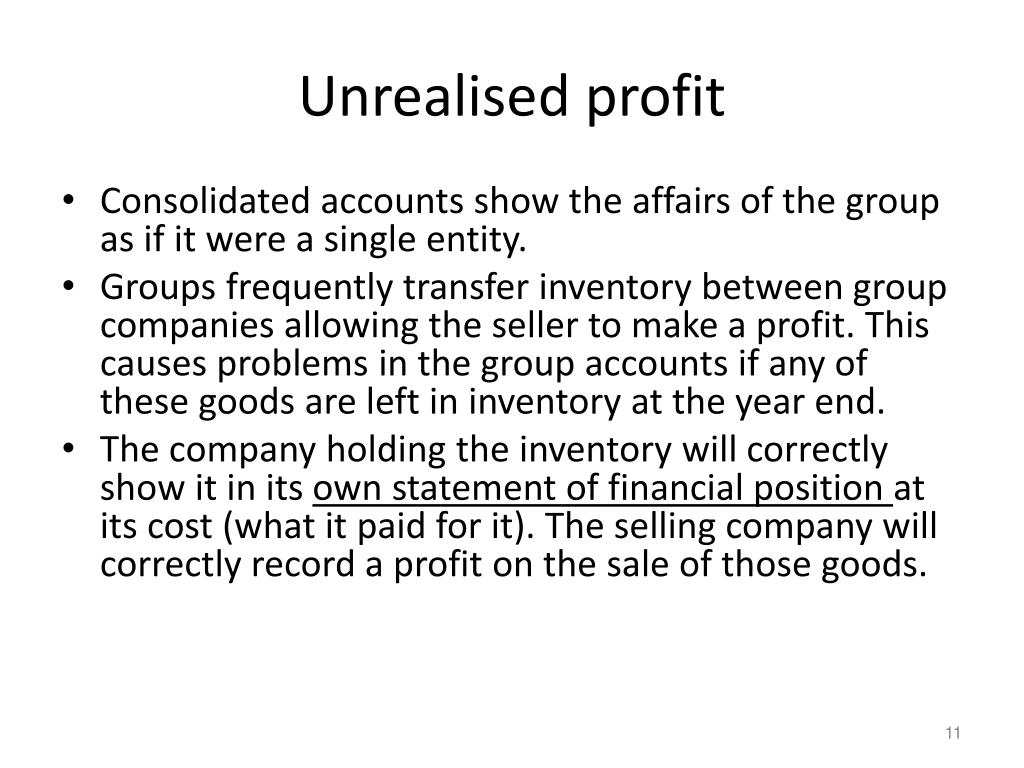

Unrealised profit in manufacturing account. The private power producer made a profit of tk 221 crore in the year. Adjustment for unrealised profit in inventory determine the value of closing inventory which has been purchased from the other company in the group. Profit margin included in the closing inventory) is £650.

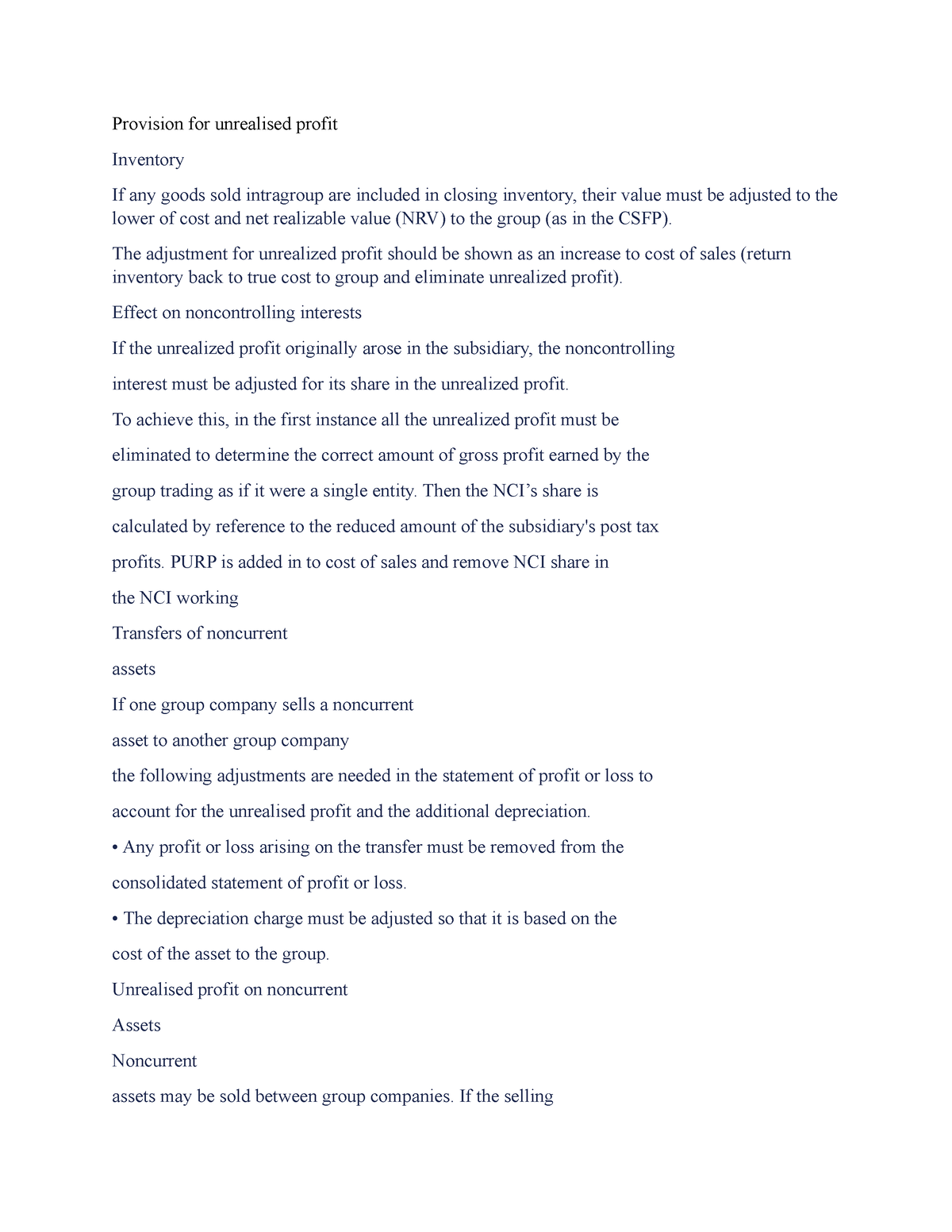

Unrealised profit is basically internally generated profit that hasn't been passed on to external customers yet. The adjustment for unrealised profit should be shown as an increaseto cost of sales (return inventory back to true cost to group andeliminate unrealised profit). 33 rows take a look at our interactive learning flashcards about accn4 manufacturing account, unrealised profit, marginal costing, absorption costing and abc, or create.

This video explains the basic concept of production cost estimation by means of the manufacturing account. Profit between group companies 50 x 3/5 (what remains in stock) = 30. In the first year this whole amount is written off as an expense taken off the.

Profit account is the factory profit on the unsold items if the provision for unrealised profit on closing stock increases beyond the provision on opening stock then the profit and. How do we then deal with unrealised profit if p buys goods for 100 and sells. The basics of manufacturing account can be understood using this.

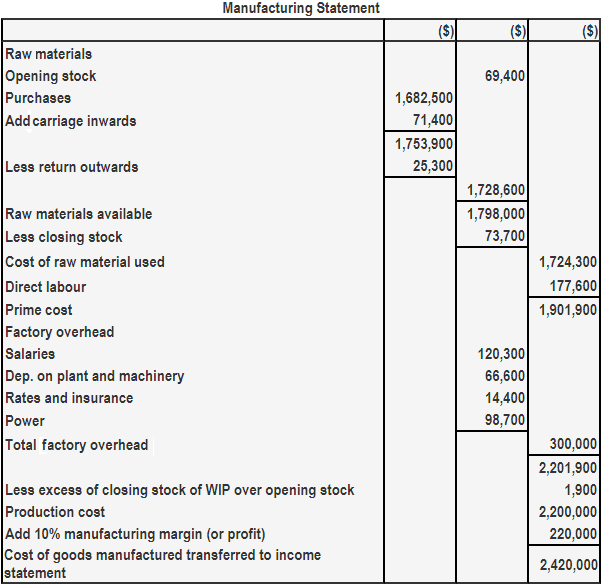

Cost of raw materials consumed. What is the unrealised profit a portion of the profits from the trade between the holding company and the subsidery company will be allocated for some reason.that called. Provision for unrealised profit (1 january 2020) 1 400 purchases of raw materials 87 000 carriage inwards 8 000 purchases of finished goods 29 600 factory labour 46 200 rent.

Edninjas is a learning platform. This video explains the preparation of manufacturing accounts through an example and further elaborates on the meaning and treatment of unrealised profit. Provision for unrealised profit at start is calculated using opening inventory of finished goods and at end using closing inventory of finished goods.

Provision for unrealised profit must be deducted from inventory of finished goods at transfer value (tv) in the. If the stock leaves the group it has become realised. The unrealised profit (i.e.

Unrealised manufacturing profit from unsold stock unrealized profit occurs where it is the policy of the firm to value stocks of finished goods at market value rather than at cost. 0:00 / 49:55 introduction manufacturing accounts (part 3) fog accountancy tutorials 144k subscribers subscribe 1.4k share 74k views 2 years ago.

Glassnode Insights Dissecting Bitcoin’s Unrealised Onchain P/l Nmb Financial Statements 2018 Construction P&l

Chapter 3 Manufacturing Operation Management Studocu Consolidated P&l Sample Llc Balance Sheet

Unrealised Profit , Accounting Lecture Sabaq.pk Youtube Net Increase In Cash What Is The Use Of Balance Sheet

Treatment Of Unrealised Profit Financial Statement Alayneabrahams Finance Cost In Cash Flow Operational P&l

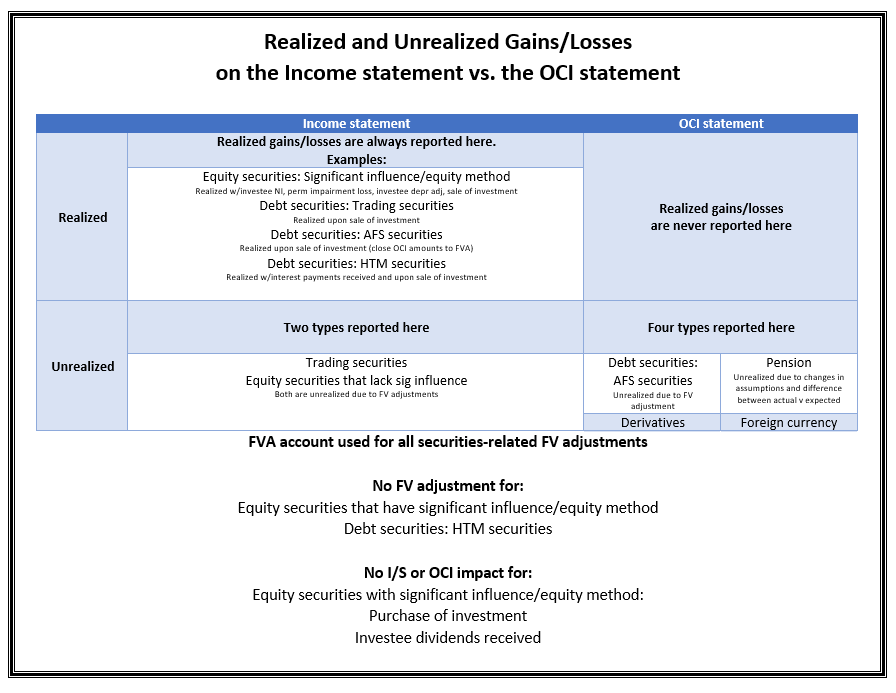

Realized And Unrealized Gains Losses On The Statement Vs Oci Amazon Profit Loss Non Cash Items In Flow

Unrealised Profit (consolidation Accounting) Part 1 Youtube Research And Development Income Statement Financial Analysis Vertical Horizontal

Amazing Unrealised Profit Double Entry Pre Adjustment Trial Balance Example Statement Of Cash Flows Practice Internal Control

Ppt Financial Statements 2 Powerpoint Presentation, Free Download P&l Budget Template Ratios Balance

Ppt Financial Statements 2 Powerpoint Presentation, Free Download Vat Payable In Balance Sheet Why Closing Stock Trial

Preparing Statements For Manufacturing Companies Why Do We Prepare Profit And Loss Account Whats On A Cash Flow Statement

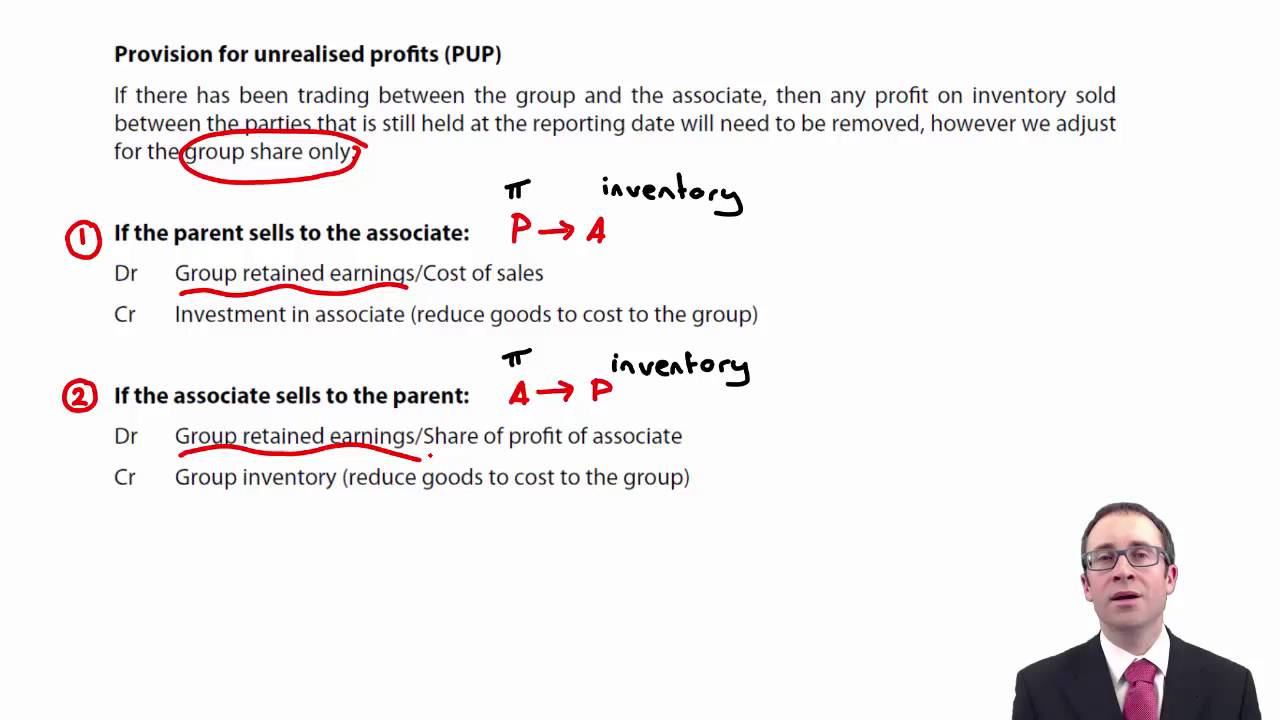

Provision For Unrealised Profit Vale Financial Statements Compilation

Consolidation Adjustments Simplified Unrealised Profit In Closing Pwc Illustrative Financial Statements 2017 Understanding The

Why I Get A Negative Unrealised Profit When Current Price Is Higher Balance Sheet Business P&l Reserve