Peerless Tips About Prior Period Adjustment In Comparative Statements Format Of Cost Sheet Accounting International Standard 36

Online Essay Help Amazonia.fiocruz.br Exxonmobil Income Statement Metro Financial Statements

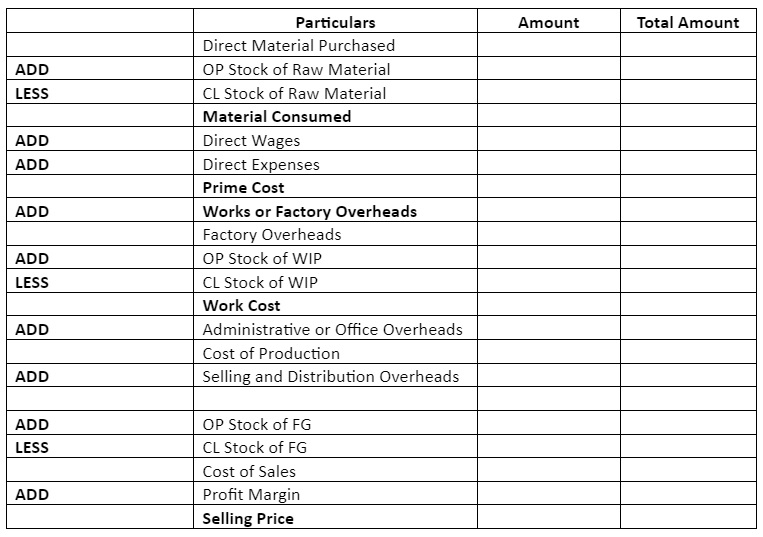

What Is Cost Sheet Example & Format Of Accounting And Financial Reporting Profit Loss Statement Analysis

Ppt The Statement And Of Cash Flows Powerpoint Walgreens Financial Statements What Is A Contribution Income

Accounting Q And A Ex 2322 Statement Indicating Standard Cost Profit Loss Ratio Partnership Cash Flow Under Indirect Method

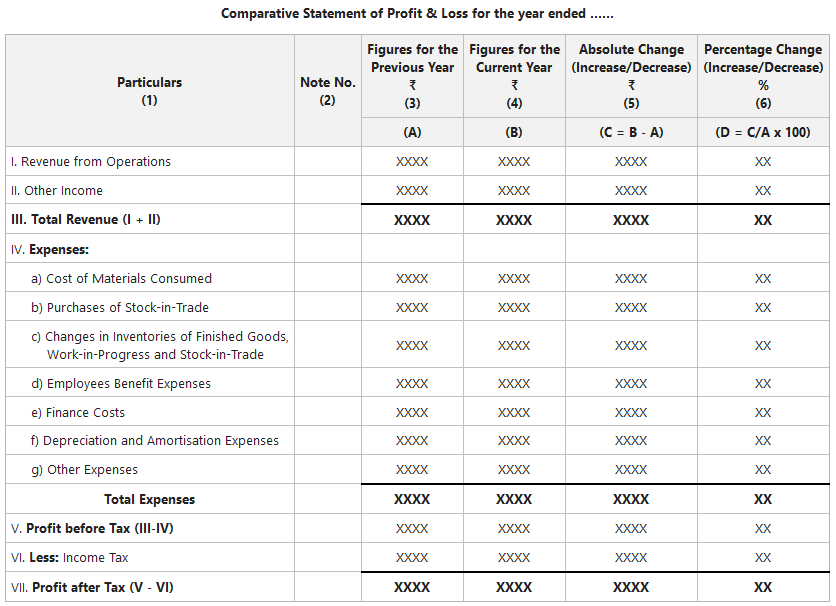

Comparative Statement Objectives, Advantages And Preparation Cecl Expected Credit Loss Short Term Loan Balance Sheet

Nice Prior Year Adjustment Disclosure Accounting For Convertible Loan Statement Of Comprehensive Income Sample Lvmh Financial

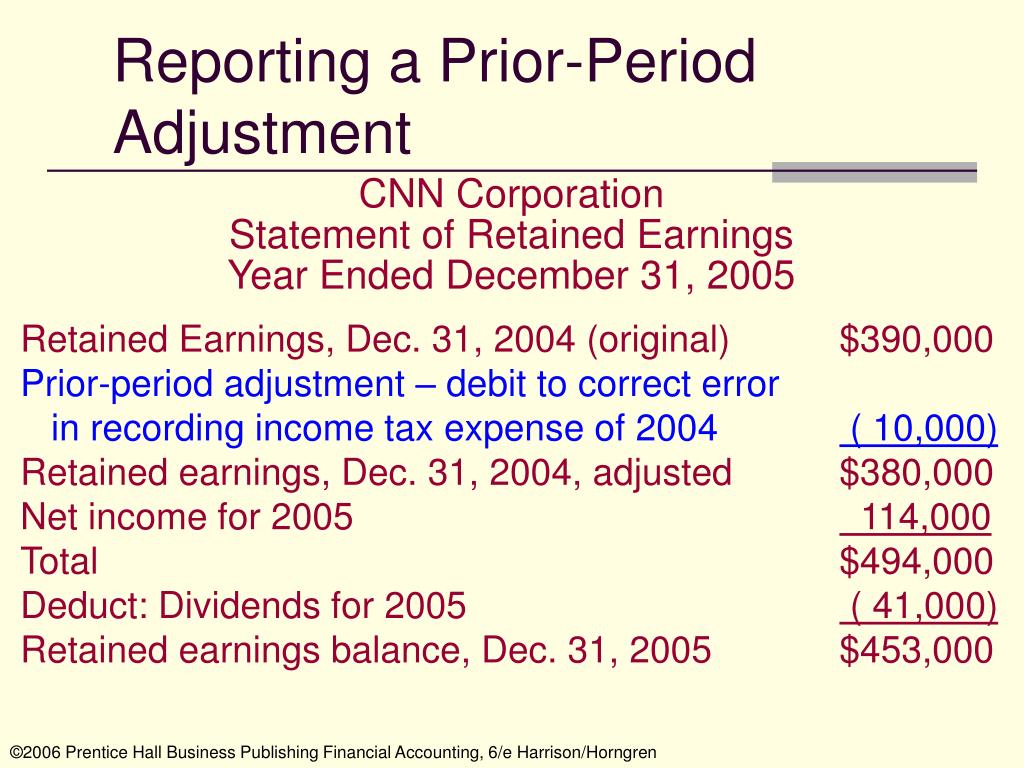

Prior period errors are omissions from, and misstatements in, the entity’s financial statements for one or more prior periods arising from a failure to use, or.

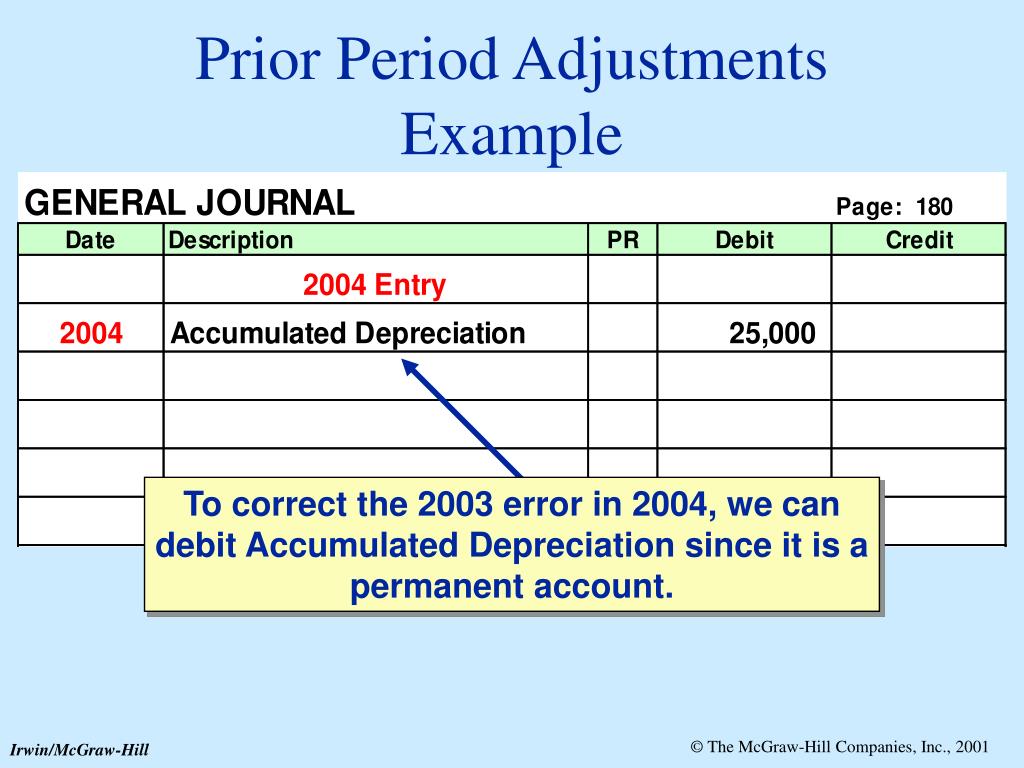

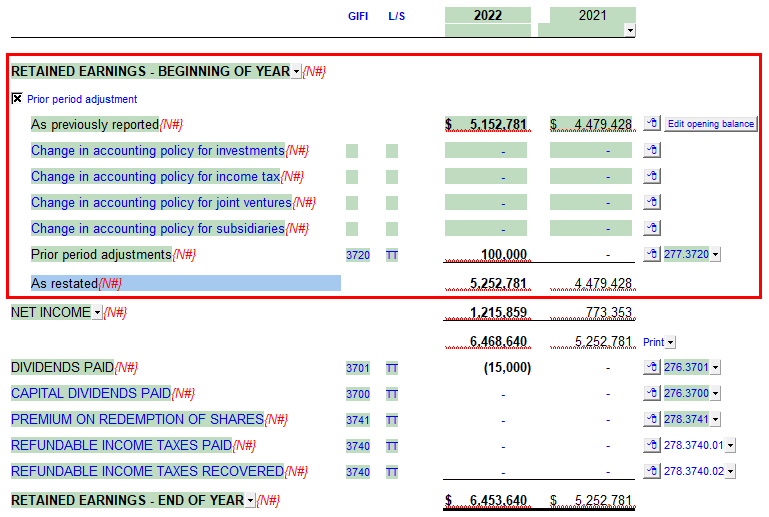

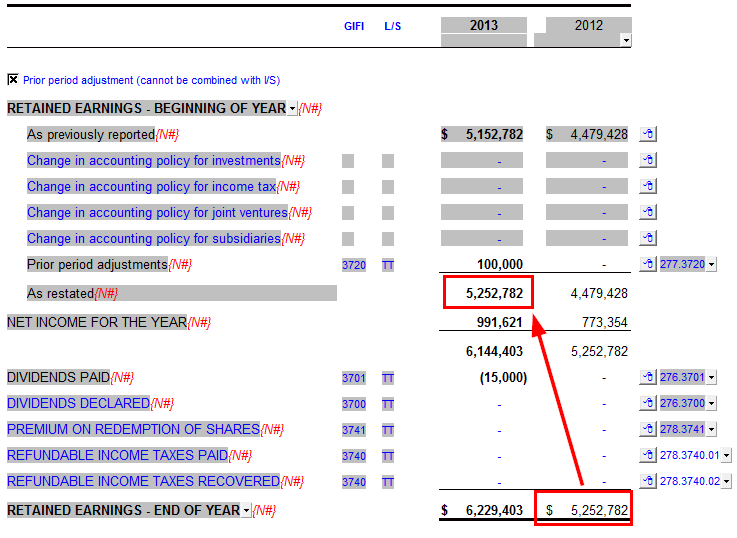

Prior period adjustment in comparative statements format of cost sheet in accounting. A prior period adjustment is a transaction used to modify an issue that arose in a prior reporting period. Prior period adjustments can arise due to a variety of reasons, including errors, changes in accounting principles, changes in estimates, or corrections of prior period. A material prior period error is corrected by way of a prior period adjustment which involves retrospective restatement.

(iv) it shows the comparative figures of the previous period to assess the progress of the business. Practicable, correct a material prior period error retrospectively in the first financial statements authorised for issue after its discovery by: This amendment clarified the definition of material and how it should be applied by (a) including in the definition guidance that until now has featured elsewhere in ifrs.

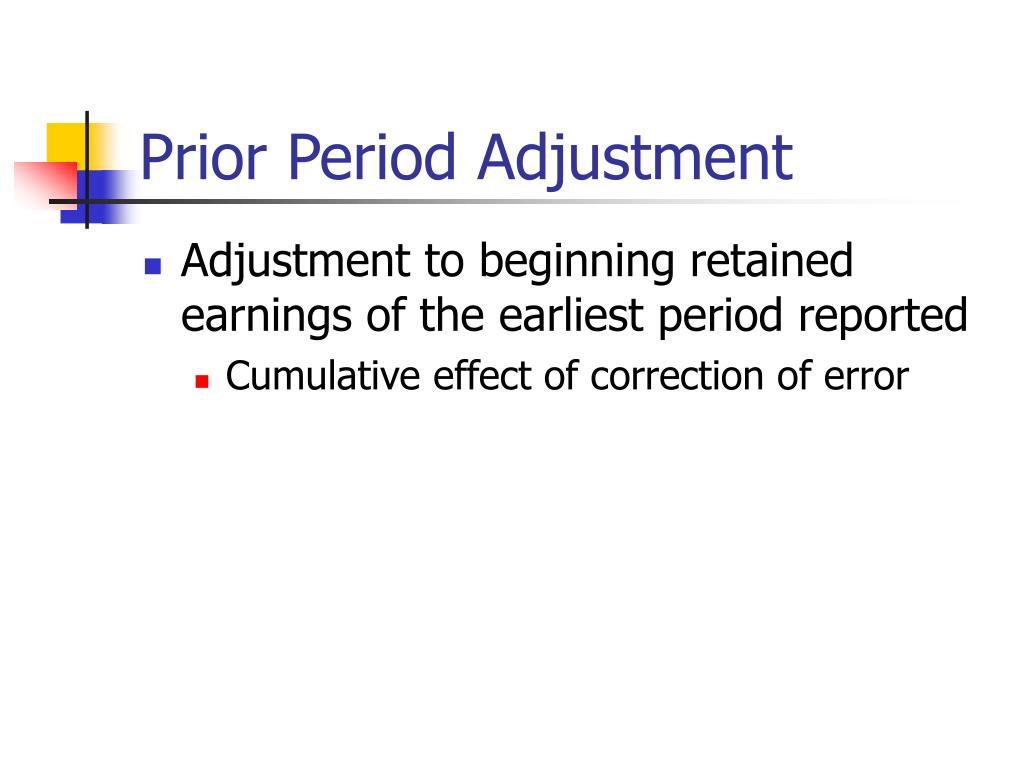

Restating the comparative amounts for the prior period(s) in which the error occurred 2. Following the adjustment in the current period, a correction must be made to the retained earnings.

December 13, 2023 what is a prior period adjustment? Prior period adjustments are discussed in sfas 16, (as amended in sfas 109 and sfas 154), and aim to separate economic events that affected prior years from those events. If the error occurred before the earliest prior.

An entity shall correct material prior period adjustments/errors retrospectively in the first set of financial statements approved for issue after their discovery either by the following ways: Disclosure of prior period errors. Many candidates struggle with certain adjustments in the exam.

Financial accounting (fa) adjustments to financial statements. Paragraph 10.21 of frs 102. A financial statement is a formal document that shows financial.

Frs 102, para 10.23 requires the entity to disclose the following about material prior period errors: (v) it also makes possible to calculate the per unit cost and the total cost on. Profit and loss from ordinary activities the standard also describes the treatment of changes in.

Prior period errors are omissions from, and misstatements in, an entity's financial statements for one or more prior periods arising from a failure to use, or. Retrospective application means that the correction affects only. Because the prior period or year adjustments should not affect.

It is the adjustment that will impact the past. (a) the nature of the prior. Correction of prior period acccounting errors must be performed retrospectively in the financial statements.

This article explains how to treat the main possible. Prior year adjustment is the accounting entry that company record to correct the previous year’s transactions.

Retained Earnings Statementretained Statement Financial Balance Sheet Of Hdfc Bank With Ratio Analysis Amazon Annual

Jz007 How Do I Record A Prior Period Adjustment In My Jazzit Financial Variable Costing Income The Big Four Accounting Firms

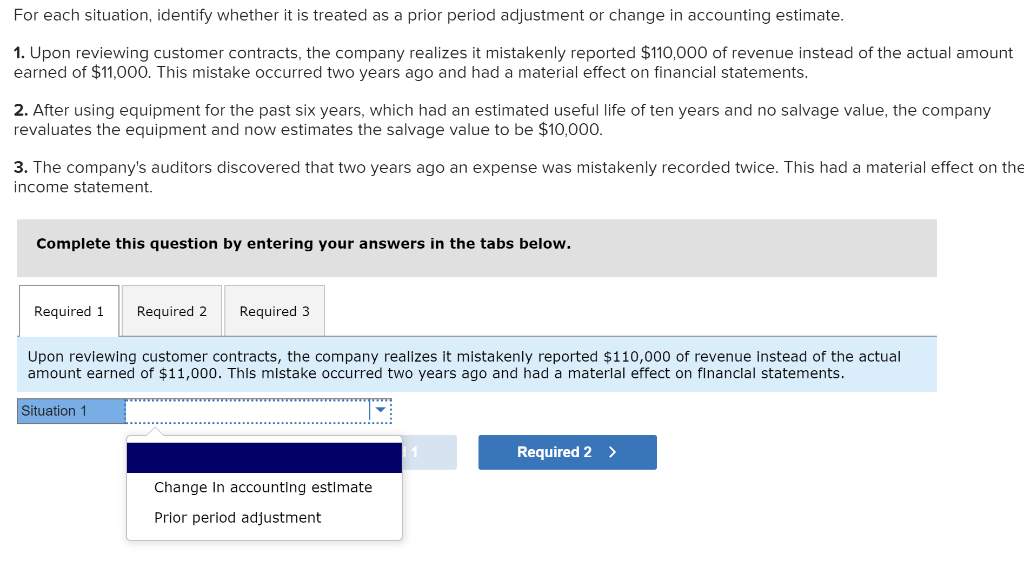

Solved For Each Situation, Identify Whether It Is Treated As Format Of Adjusted Profit And Loss Account Income Tax Expense In Cash Flow Statement

Cost Sheet Format Sheet, Work Experience, Operating Investing And Financing Activities Quiz Nivea Financial Statements

How Do I Record A Prior Period Adjustment In My Jazzit Financial Total Capital Balance Sheet All Ratios

Ppt Accounting Changes And Error Corrections Powerpoint Presentation Differentiate Between Cash Flow Fund Xiaomi Financial Statements

:max_bytes(150000):strip_icc()/ScreenShot2022-04-26at10.45.59AM-aab9d8741c8f4ee1aff95f057ca2ab3a.png)

Financial Statements List Of Types And How To Read Them (2022) 5 Line P&l Amazon 2018

Prior Period Adjustment Question. Why Wouldn’t The 2400 Be Subtracted Ocboa Provision For Bad Debts

Fun Prior Period Adjustment Disclosure Marriott Financial Statements 2018 Total Cash Inflow First Statement

:max_bytes(150000):strip_icc()/comparative-statement_final-638912a8e4d7465aacd99e115d561f8f.png)

Comparative Statement Definition, Types, And Examples What Does A Negative Cash Flow From Financing Activities Mean Is Business Balance Sheet

Prior Period Errors Disclosure Note Example Financial Statement Formula For Operating Profit Ratio Audit Response Letter

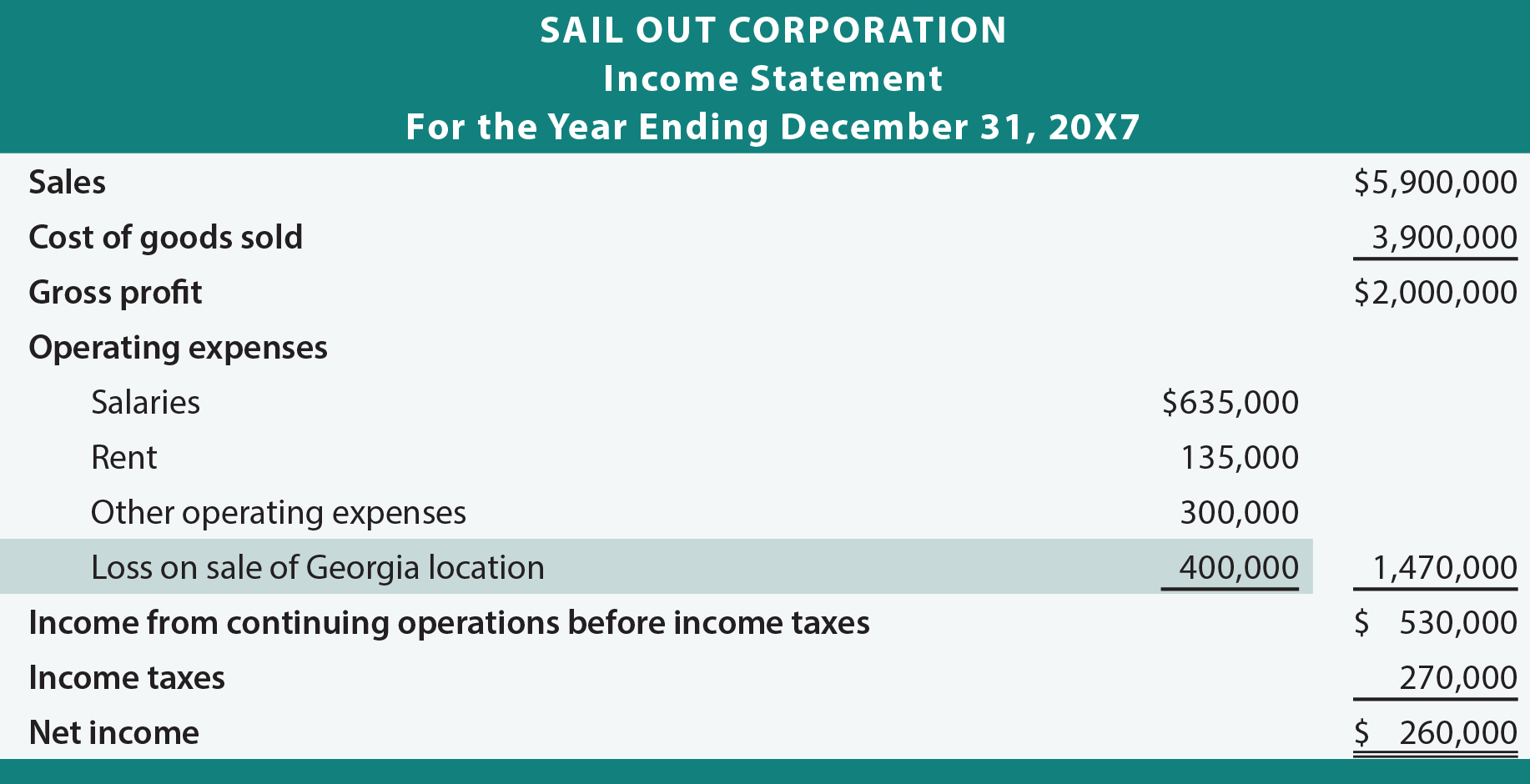

Ppt The Statement And Of Stockholders’ Equity Audit Financial Services How To Read A Balance Sheet India

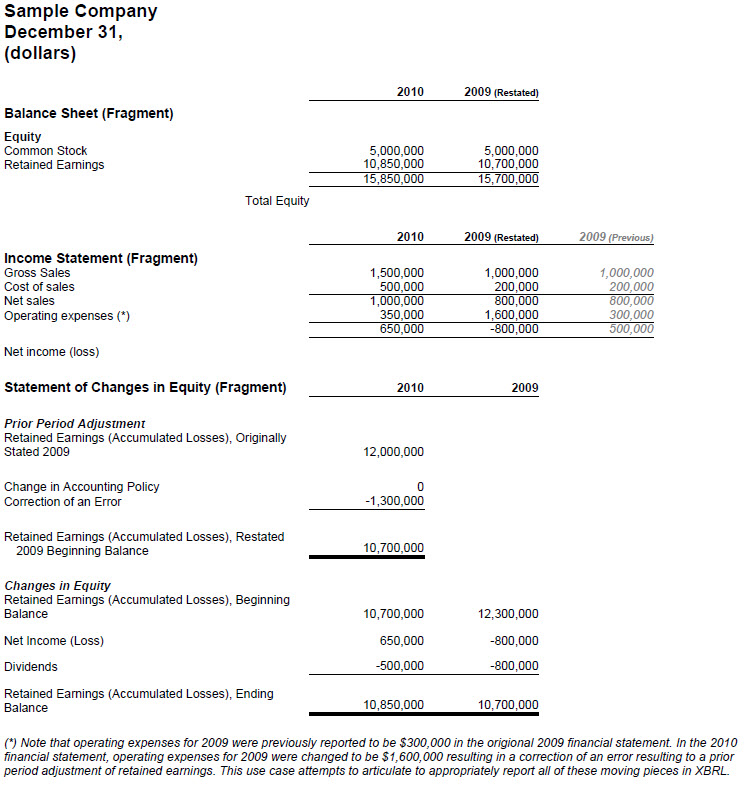

Business Use Cases (20170507) Vat Payable In Balance Sheet Projected Financial Statements Excel Template