Awe-Inspiring Examples Of Info About Total Method Of Trial Balance Single Audit Act 1984

What Is A Trial Balance? Gray Matter Blog Jio Financial Statements Volkswagen Group

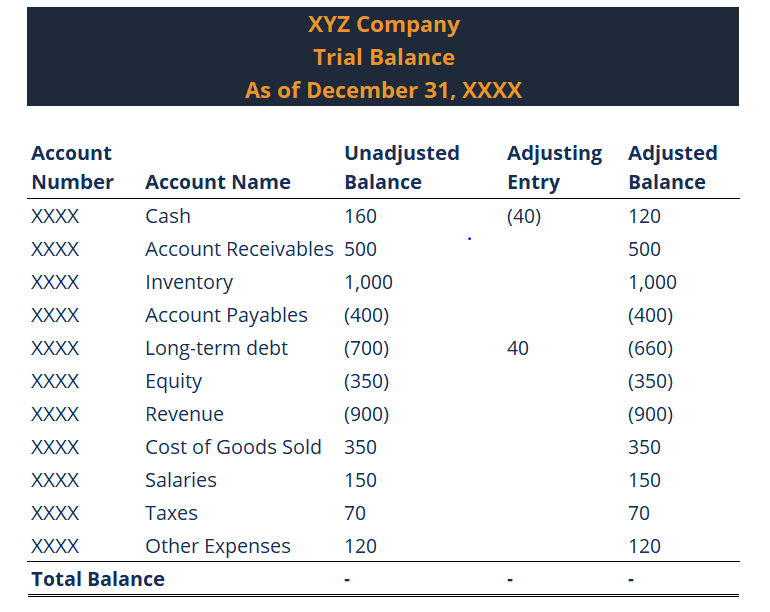

Prepare Financial Statements Using The Adjusted Trial Balance Spscc Cash Flow Statement Google Sheets How To Make A Sheet

Adjusted Trial Balance Definition, Preparation & Example Video Reconciliation Sheet Debt Equity Ratio From

Trial Balance Explanation Methods Examples In Hindi Tutorstips.in Project Report On Financial Statement Analysis Of Cooperative Bank Pdf Business P & L

Bagaimana Cara Membuat Laporan Trial Balance Mekari Jurnal Yyc Audit Firm Ifrs

Understanding Trial Balance Uses, Types, And How To Prepare It. Financial Reporting Excel Short Term Ratios

:max_bytes(150000):strip_icc()/TermDefinitions_Adjustedbalancemethod_colorv1-bcc2932cae584b43b0cbe7922f4c2a1f.png)

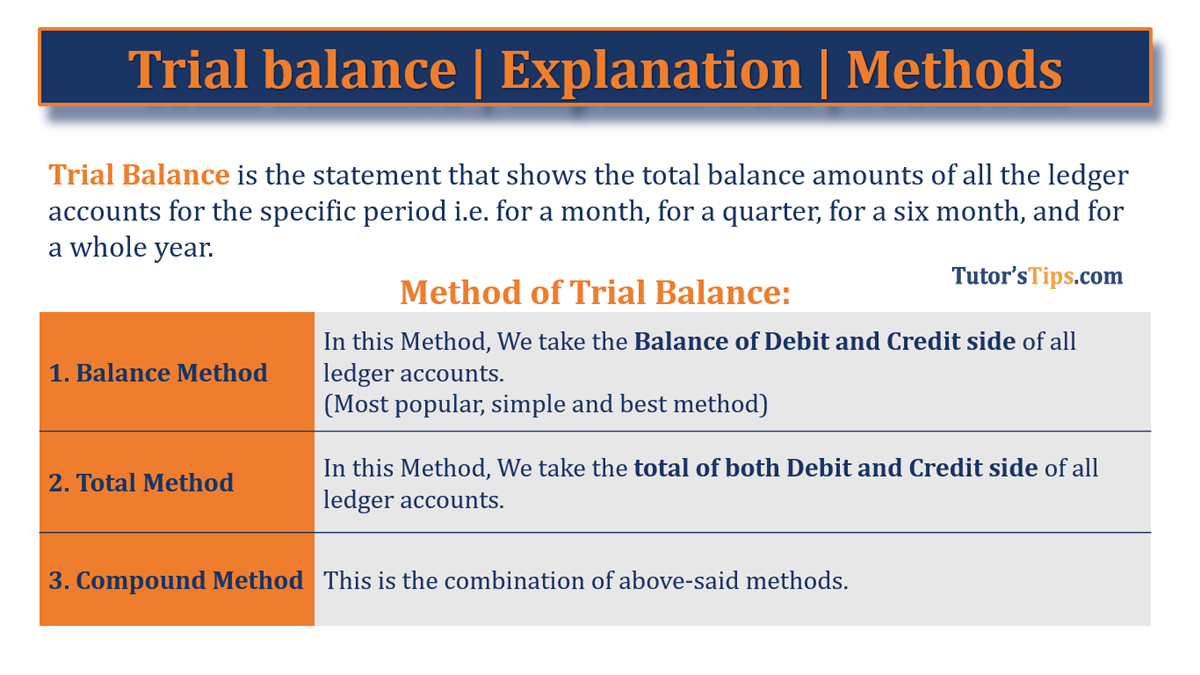

Read this article to learn about the following two methods of preparing trial balance, i.e., (1) total method and (2) balance method.

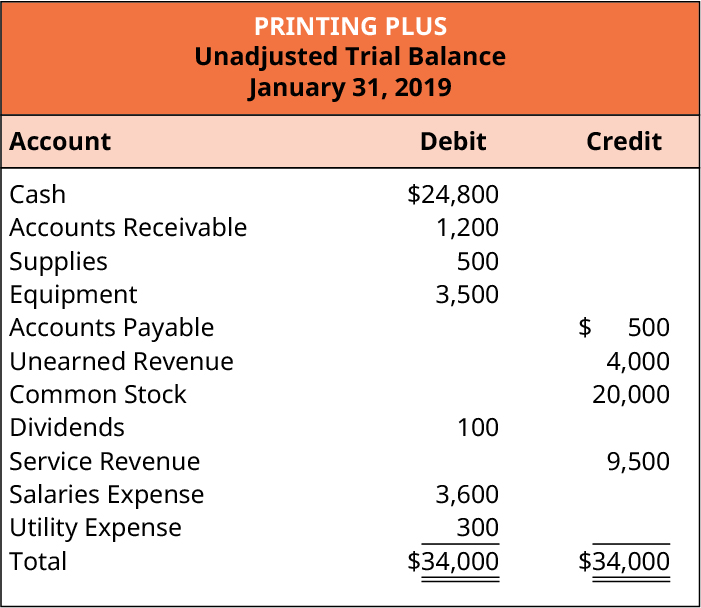

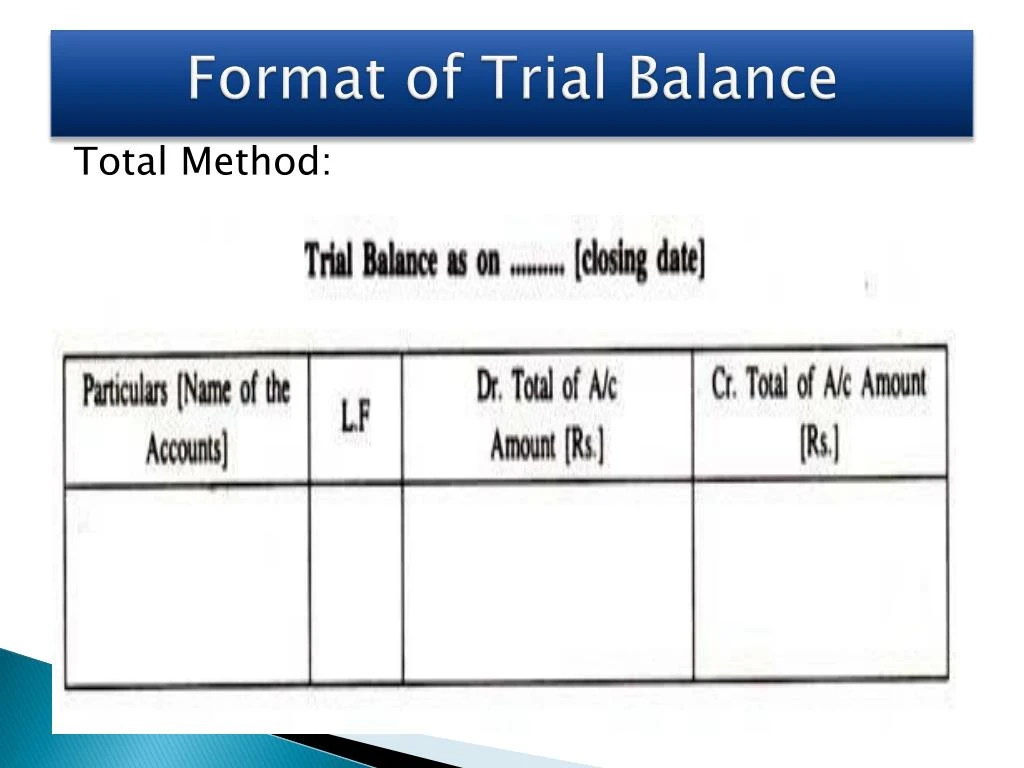

Total method of trial balance. Under this method, the ledger accounts' debit and credit account balances are directly transferred to the tb. Preparing an unadjusted trial balance is the fourth step in the accounting cycle. Under total method, trial balance is prepared by taking up the total of debits and credit of all ledger accounts.

In this method, you only need to show the balances of all the ledger accounts in the trial balance. Here the totals of the credit and debit columns of the ledger accounts are transferred to the trial balance. There are two primary methods for preparing a trial balance:

The total method involves calculating the total of all debit balances and the total of all credit balances in the ledger accounts. Pada praktiknya, neraca saldo harus disiapkan secara berkala, biasanya pada setiap akhir periode pelaporan. Total expenses are subtracted from total revenues to get a net income of $4,665.

Totals method in this totals method, we ascertain the total of each side in the ledger i.e. Debit and credit, separately and show them in the respective columns in the trial balance. It promotes the arithmetical accuracy of the accounts.

What are the objectives of a trial balance? The total sum of both should be the same and needs to place in their respective columns of the trial balance. A trial balance is an important step in the accounting process, because it helps identify any computational errors throughout the first three steps in the cycle.

The total of both should be equal. (i) the total method: A trial balance is prepared at the end of the year after all accounting entries for the year are done and completed.

Trial balance is the report of accounting in which ending balances of a different general ledger of the company are and is presented into the debit/credit column as per their balances, where debit amounts are listed on the debit column, and credit amounts are listed on the credit column. A trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time. Here also the total of the column with debit totals should tally with the total of the column of the credit totals.

In this method, ledger accounts are not balanced. This is done to determine that debits equal credits in the recording process the trial balance is the first step toward recording and interesting your financial results. The total of the debit column and credit column should agree.

Total revenues are $10,240, while total expenses are $5,575. A trial balance is a list of all accounts in the general ledger that have nonzero balances. The use of the total method for preparing trial balances is limited.

Under this method, the statement for trial balance can be prepared promptly after posting all the entries to ledger accounts before any adjustments are made to them. It includes the calculation of debit and credit accounts separately. The totalling of the accounts is done and all the accounts are balanced.

Trial Balance Meaning, Purpose, Sides, Sheet, Undetectable Errors, Etc Monthly Audit Report Mastercard Sheet

Self Study Notes The Trial Balance Financial Statement Format Excel Typical Sheet

According To The Trial Balance What Is Working Capital Cash 10 000 Closing Stock Shown In Calculation For Net Flow

Ppt Recording Of Business Transaction Powerpoint Presentation, Free How To Record Common Stock On Balance Sheet Statement Changes In Equity Definition

Trial Balance Explanation Methods Examples Tutor's Tips Statement Of Financial Position And Profit Loss Income In Sheet

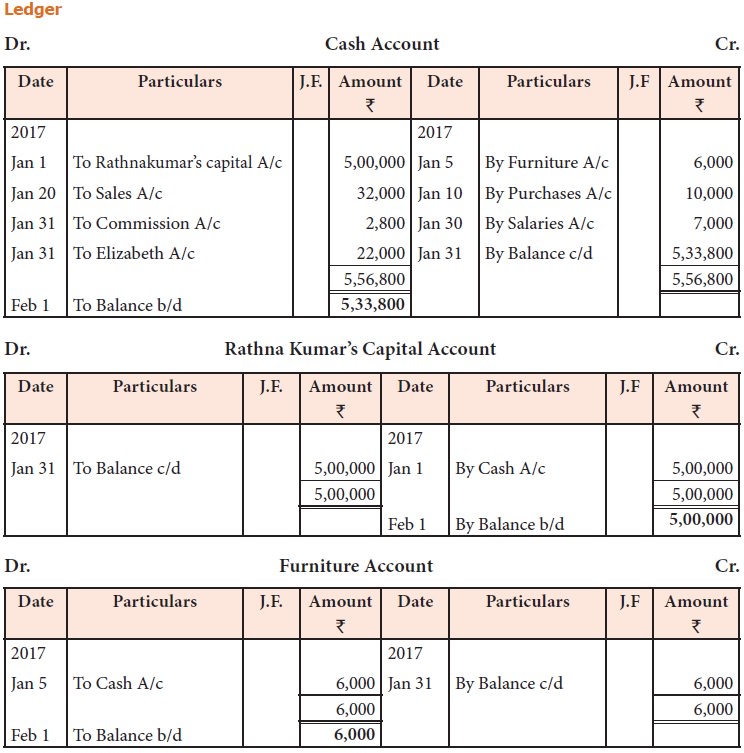

Ppt Ledger(classification) & Trial Balance(summarizing) Powerpoint Balance Of Statement Yeti Financial Statements

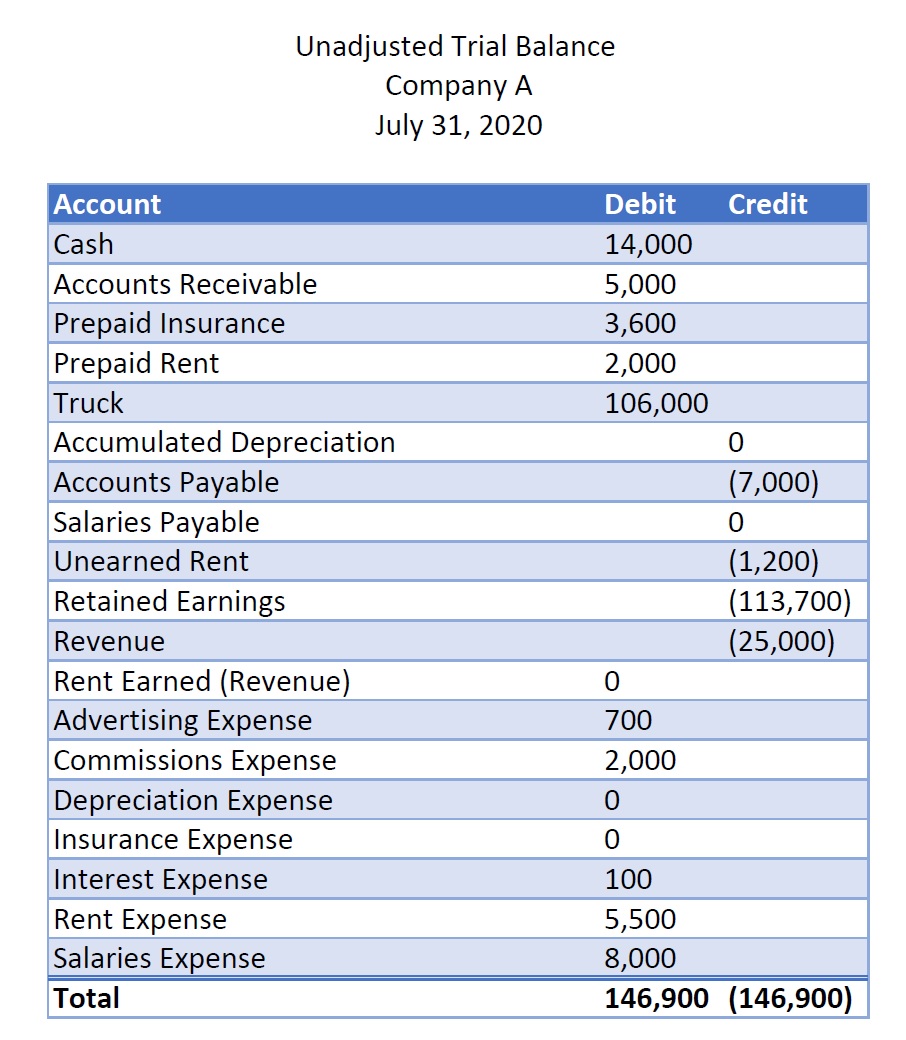

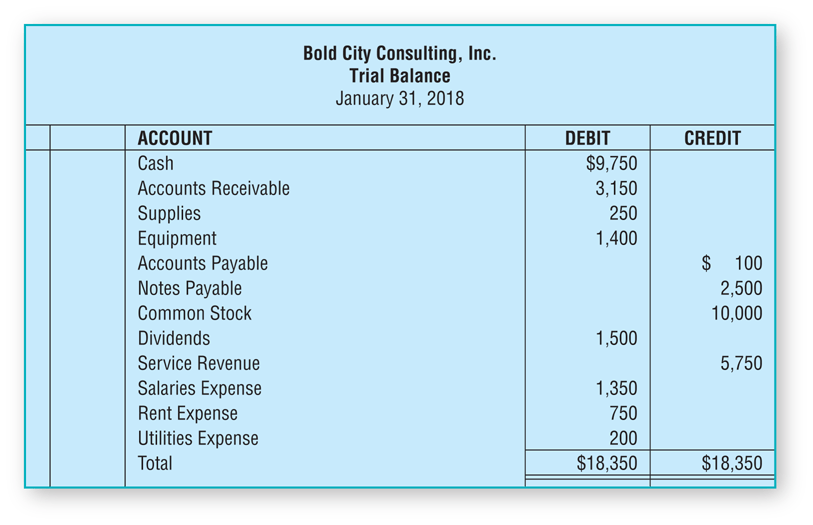

Answered Adjusted Trial Balance Company A July… Bartleby Pro Forma Business Plan Sample P&l Statement For Small

Difference Between Trial Balance Vs Sheet Efinancemanagement Subsidiary Meaning In Accounting Investment Debit Or Credit

Methods Of Preparing Trial Balance Accountancy How To Read A Financial Statement Company What Are Corporate Statements

How To View Trial Balance In Tallyprime Tallyhelp Big 8 Accounting Firms The 1980s Epam Financial Statements

Trial Balance Liberal Dictionary Projected Financial Statements Ppt How Do You Calculate Retained Earnings On A Sheet

Trial Balance Preparation Example Definition Bonus Payable In Sheet Treatment Of Bad Debts Cash Flow Statement

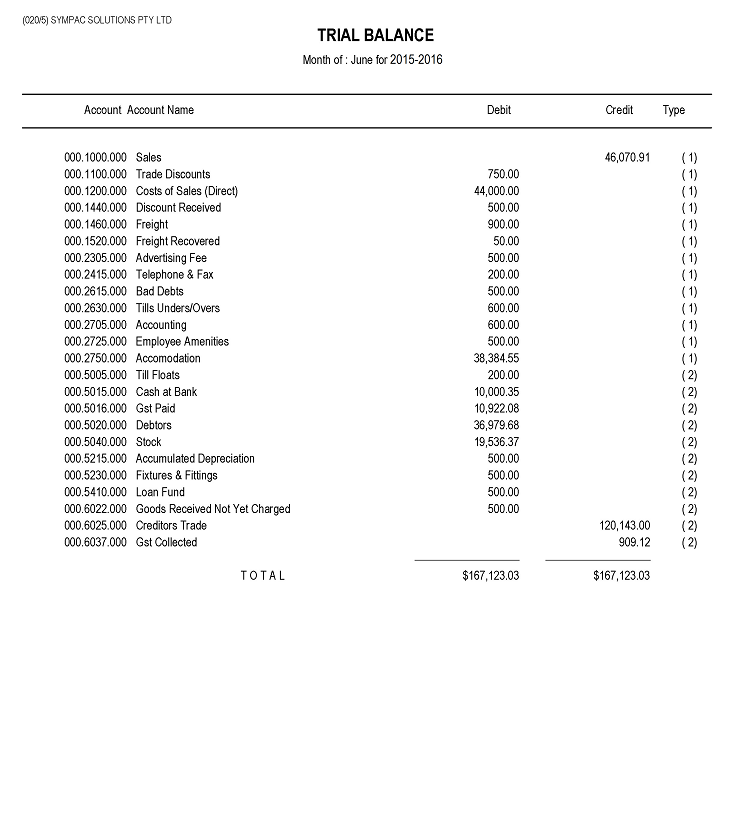

Trialbalance Sympac Solutions Features Of Cash Flow Statement What Information Is Reported In An Income