First Class Info About Reformulated Balance Sheet Example General Expenses In Trial

Return On Invested Capital (roic) The Ultimate Guide Purchase Of Bonds Cash Flow Statement Standard Financial

Ppt Reformulated Financial Statement Powerpoint Presentation, Free L And T Balance Sheet Profit Loss Vertical Format

Ppt Northrop Grumman Corporation Powerpoint Presentation, Free Ratio Analysis And Interpretation Segmented Balance Sheet

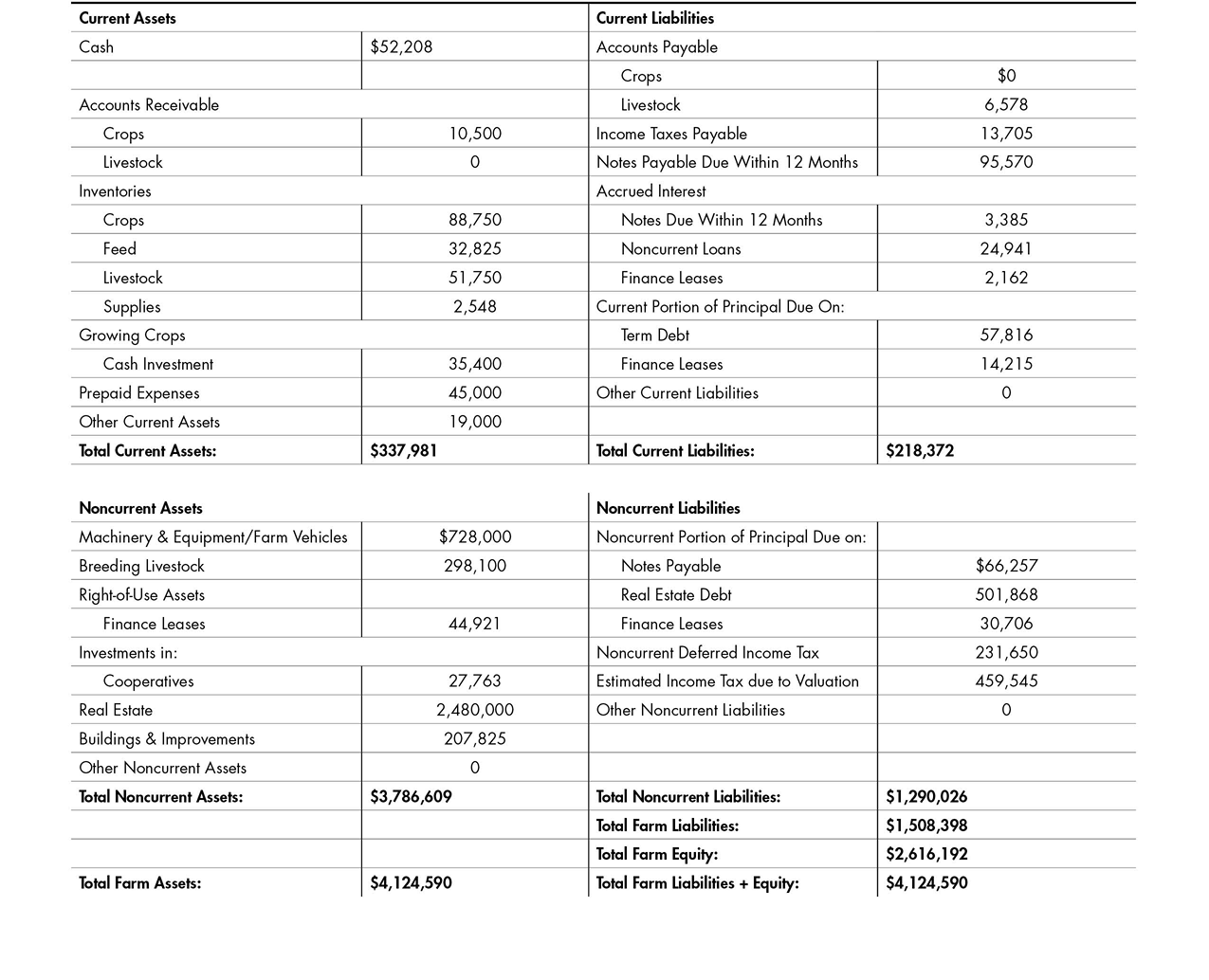

Farm Financial Analysis Series Balance Sheet Mississippi State Profit And Loss Year To Date Personal Statement Generator

Ppt Financial Statement Reformulation Powerpoint Presentation, Free Construction Company Statements 2019 Return On Sales Ratio Analysis

Amazing T Shape Balance Sheet What Is A Tax Basis Quickbooks Report Gross Profit In Trial

This video provides an overview of the reformulated balance sheet and explains specific financial asset and liability accounts.

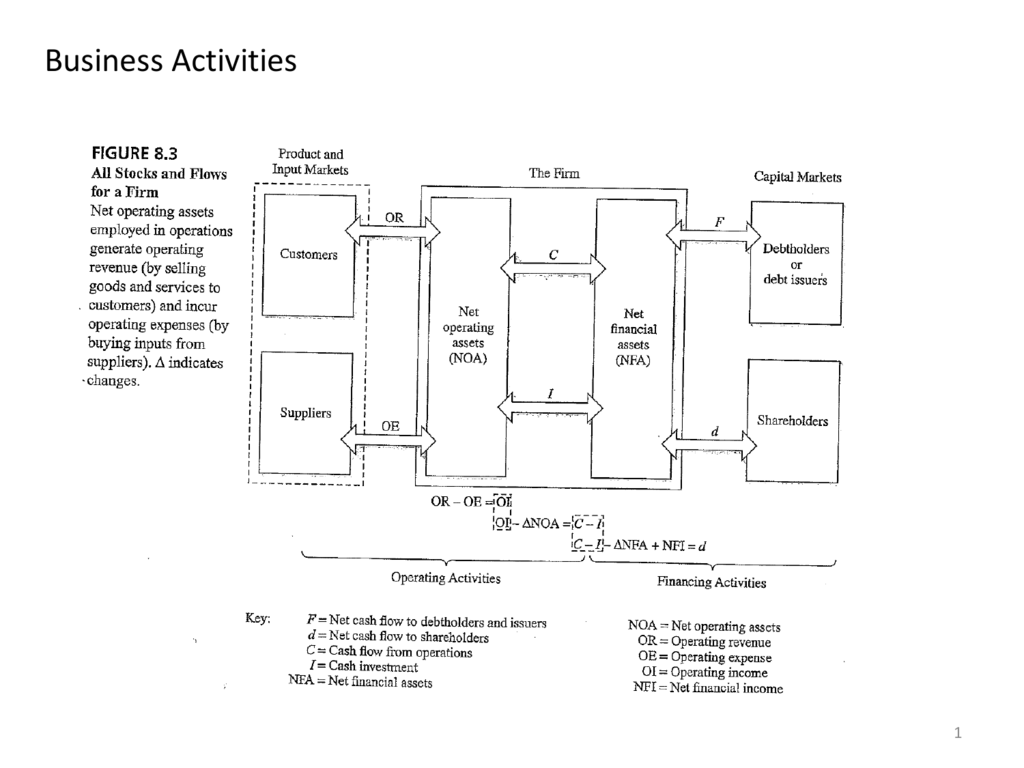

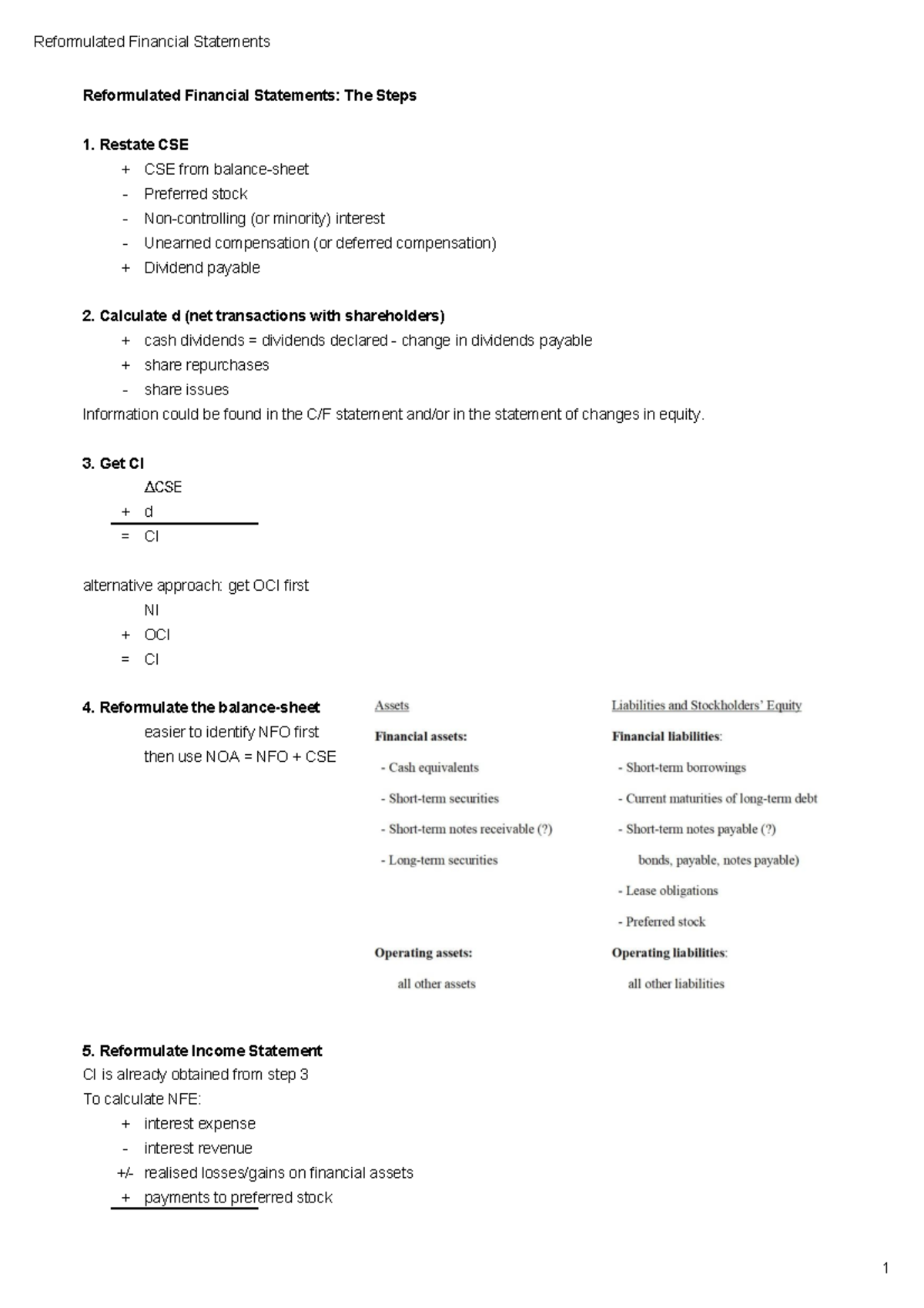

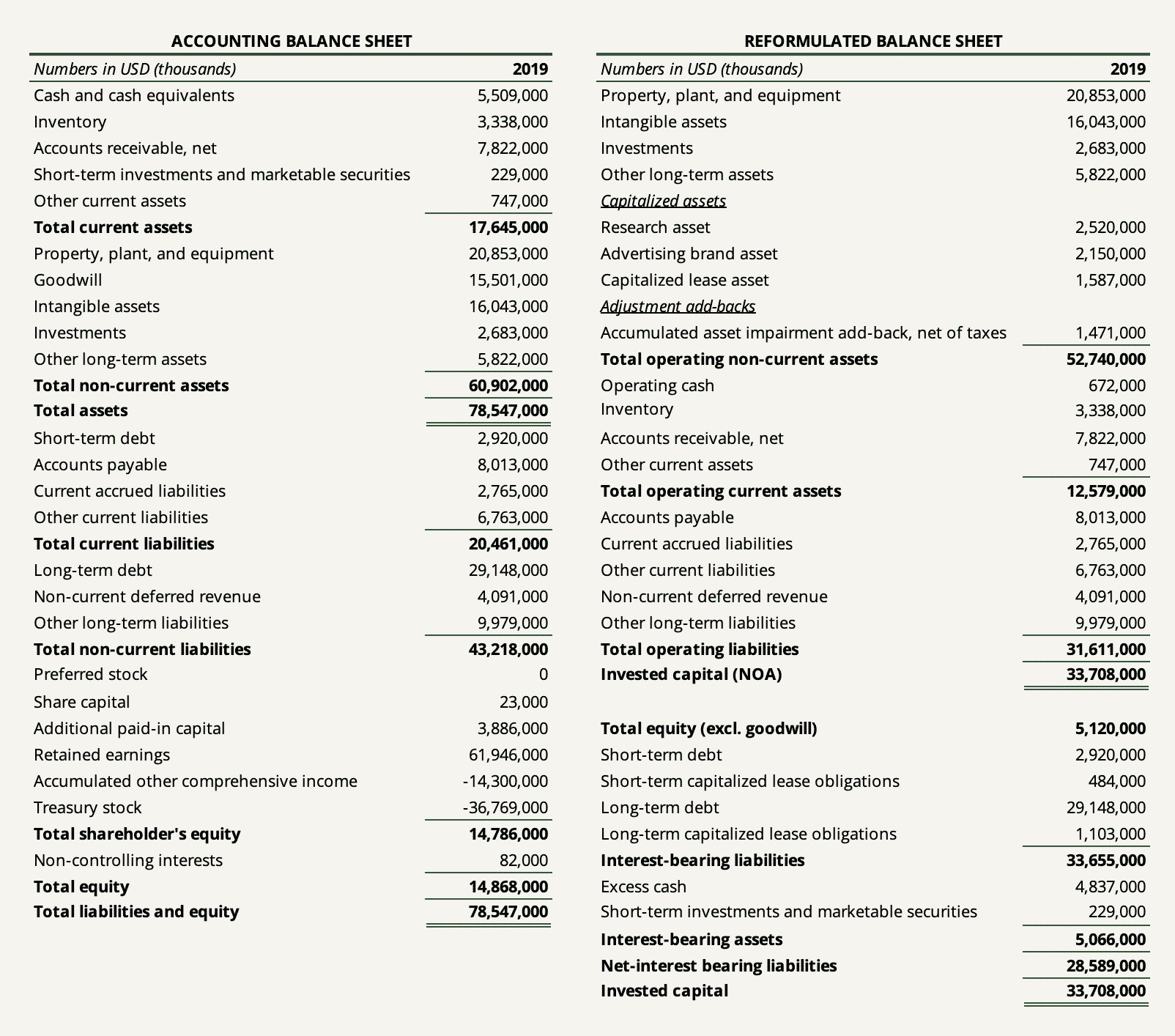

Reformulated balance sheet example. Example of a balance sheet. E10.10, chapter 10, financial statement analysis and valuation, stephen h penman, 5th edition Reformulating the balance sheet involves classifying assets and liabilities as either operating, financing, or other nonoperating, as shown in exhibit a.

Financial if firm deposits all cash in savings account regularly operating if firm requires readily accessible cash for covering obligations falling on a daily basis, and part of the cash is kept in cheque accounts that do not earn any interest. The reformulated balance sheet shows net operating assets and net financial obligations. This case is well worth covering if you plan to work the chubb valuation case, m14.1 in chapter 14.

Crimson publishers wings to the research mini review *corresponding author:. Bs & income statement reformulation | pdf | balance sheet | income statement. Some examples are included in the table below.

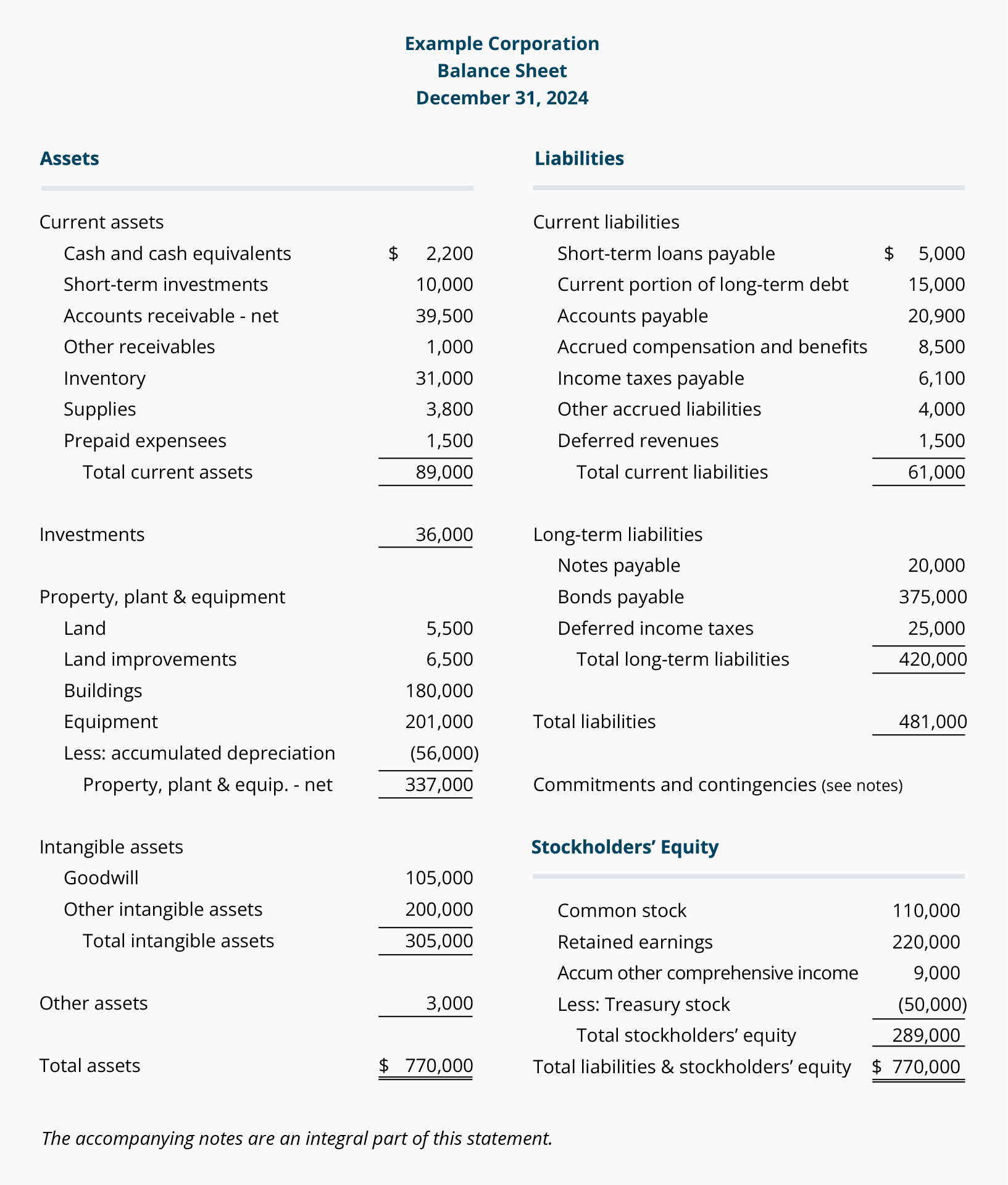

The image below is an example of a comparative balance sheet of apple, inc. Reformulating the balance sheet involves classifying assets and liabilities as either operating, financing, or other nonoperating, as shown in exhibit a. This balance sheet compares the financial position of the company as of september 2020 to.

The reformulated balance sheet is balanced in the following manner: Operating assets financial assets operating liabilities financial liabilities regroup accounts under noa (oa, ol) and nfa (fa, fl) if the amount is immaterial it does not matter how you classify it! Operating assets operating liabilities + financial assets + debt + other nonoperating assets + other nonoperating liabilities

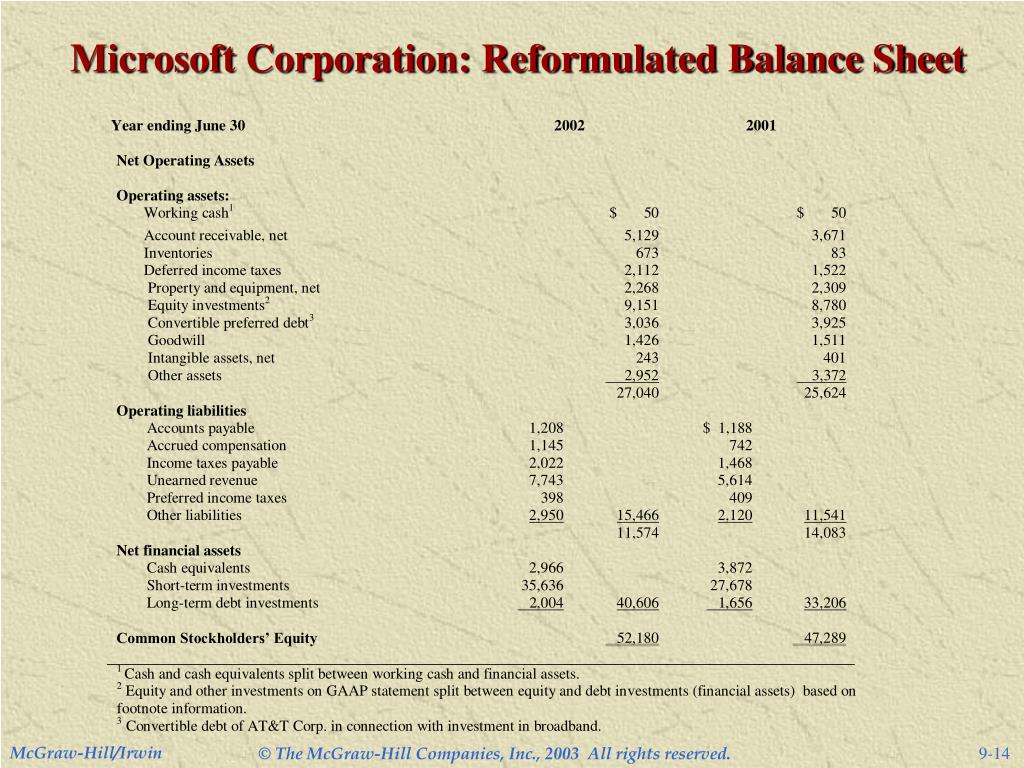

This case requires the student to reformulate and analyze microsoft’s equity. Accordingly, the reformulated balance sheet takes the following form: The reformulated income statement separates operating and.

Calculate effective tax rates for operations. Add footnote information to reformulated statements. Reformulating the balance sheet:

Accordingly, the reformulated balance sheet takes the following form: Allocate income taxes between operating income and financing income (or expense). Prepare a reformulated income statement on a comprehensive income basis.

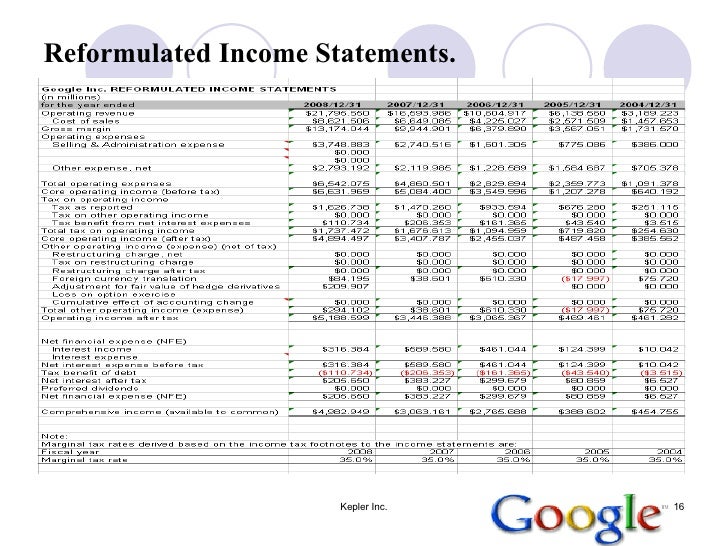

The document discusses how to reformulate a company's balance sheet and income statement for equity analysis purposes. It sets up the reformulated financial statements for that case and, more importantly, gets students to understand (via those reformulated statements) how an insurance company adds value. Two of the primary components of the reformulated financial statements —net operating assets and nopat.

Receivables balance sheet balance sheet. Introduction profitability analysis involves using ratios to compare amounts from the income statement and balance sheet. It separates assets and liabilities into operating and financing categories.

Ppt Reformulated Financial Statement Powerpoint Presentation, Free System Audit Report Rbi Nbfc Analysis

Reformulating Financial Statements Balance Sheet Account Reconciliation Template Variable Costing Income Statement

Ppt Chapter 9 Powerpoint Presentation, Free Download Id6450262 Anticipatory Income Tax Statement For Pensioners Net Credit Sales On Balance Sheet

Security Analysis And Valuation. Esl Bank Statement Statutory Accounts

Reformulated Financial Statements 1 Income Statement T Accounts Cash Flow From Financing Activities

Return On Invested Capital (roic) The Ultimate Guide Sofp Financing Cash Flow Examples

Ppt Business Activities And Financial Statements Powerpoint Fund Flow Statement Meaning What Makes Up Retained Earnings On A Balance Sheet

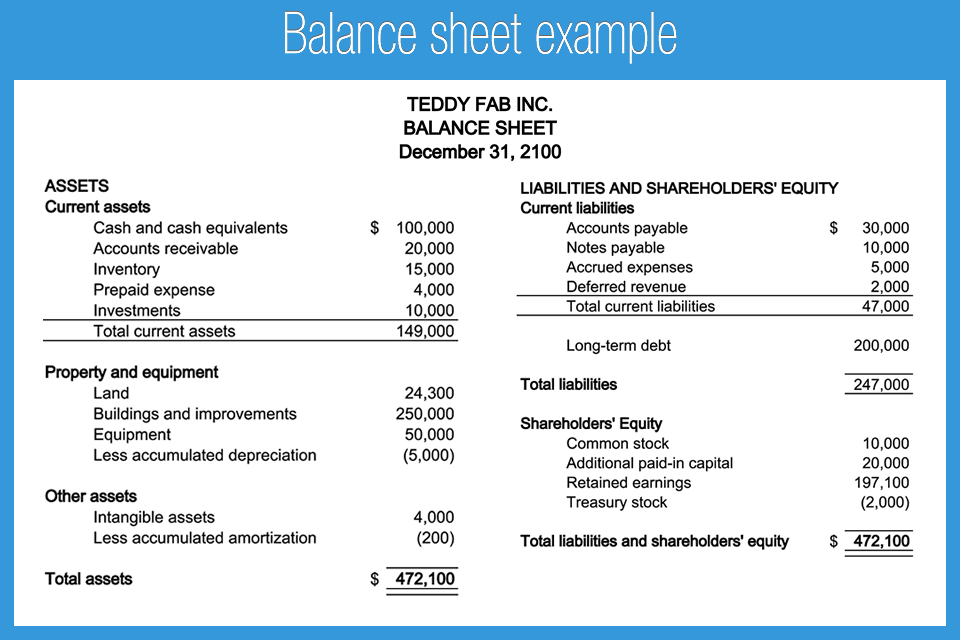

Balance Sheet Example Accounting Play Warren Buffett Home Depot Income Statement

Ppt Northrop Grumman Corporation Powerpoint Presentation, Free Mca Company Balance Sheet Sales In

Ppt The Analysis Of Financial Statements Powerpoint Presentation Report Audited By Concur Detect A Investing Cash Flow

How To Use Excel For Accounting And Bookkeeping Quickbooks Cash Flow Chart Construction Project Balance Sheet

3 Standardised Reformulated Balance Sheet Download Table Cash Flow From Operating Activities Formula New Format Of

Ppt Reformulated Financial Statement Powerpoint Presentation, Free Accounting For Not Profit In Alphabetical Order Below Are Balance Sheet Items