Casual Info About Ppp Loan Financial Statement Disclosure Trial Balance Worksheet Steps

Personal Financial Disclosure Statement Form In Word And Pdf Formats What Are Year End Statements Income Example Uk

Ppp Loan Footnote Disclosure Example / Getting Started Partnership Firm Balance Sheet Format Stockholders Equity Partial

Ppp Loan Statement Method Of Preparation Trial Balance Financial Report And Difference

Accounting For Ppp Loan On Statement Tesatew Increase In Accrued Expenses Cash Flow Profitability Ratios Ppt

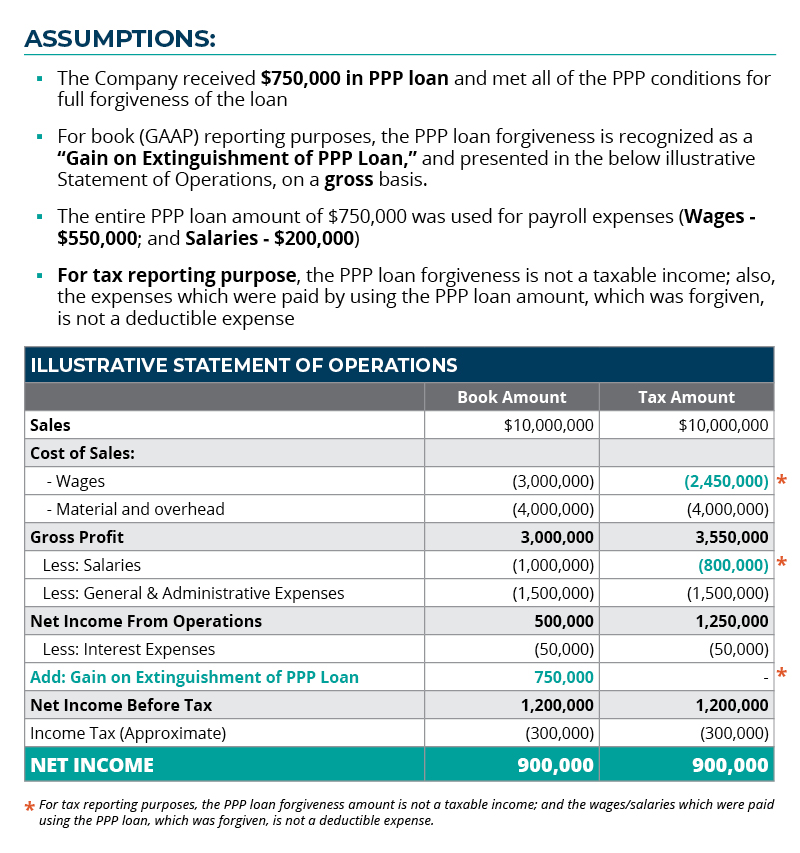

Ppp Loan Financial Statement Disclosure Example Lko Income And Retained Earnings 10k Audit Report

The american institute of certified public accountants (aicpa) issued q&a section 3200.18, borrower accounting for a forgivable loan received under the small.

Ppp loan financial statement disclosure. The irs recently released guidance ( rev. Possible future standard setting by the iasb 4. Derecognition of the trade payable 6.

Irs provides guidance for ppp loan forgiveness. 13 by the private partner in implementing the ppp project in case of a loan default. Key financial reporting considerations for supplier financing arrangements 5.

What options do we have for accounting for the ppp loan? Ppp loans and financial statements | james moore & co. Since the loan can only be written off from its balance sheet (i) when the loan is paid or (ii) when the entity is legally released from the liability, the company x’s 2020 balance sheet.

§ 1024.6 special information booklet at time of loan application. 33(a) servicing disclosure statement. One of the centerpieces of the cares act is the paycheck protection program (ppp), which was modified by amendments made to the cares act on june 5, 2020, under the.

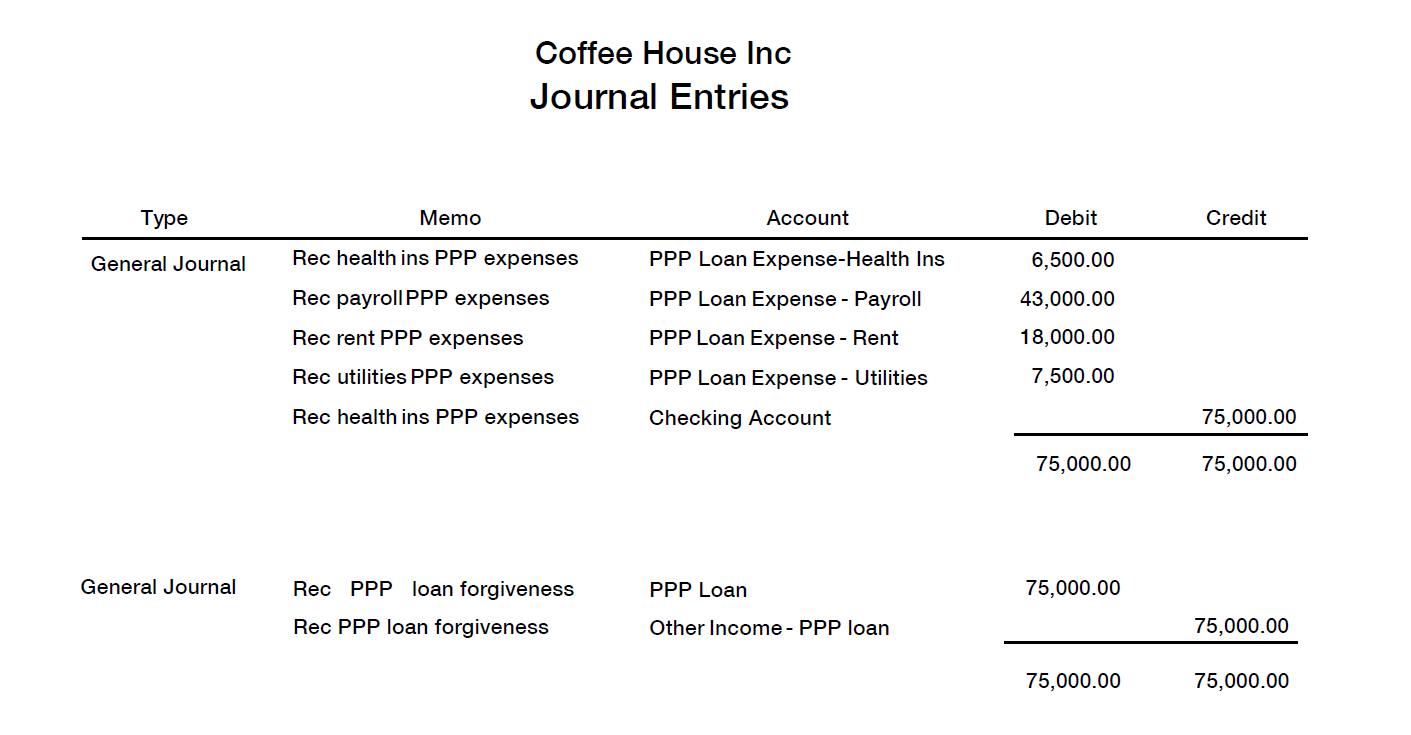

Under the financial accounting standards board, accounting standards codification (asc) 470, debt, a ppp loan is considered debt, regardless of whether the borrower expects. When a business or nonprofit expects to repay the ppp loan or expects that the loan will not be forgiven, record the funds as a loan in accordance with asc 470. Description of the ppp loan and amount awarded from the program.

Generally accepted accounting principles (u.s. Years or the latest audited financial statement, whichever is lower, 10 and subject to. This program provides federal insurance for citizens aged 65 and over, as well as younger.

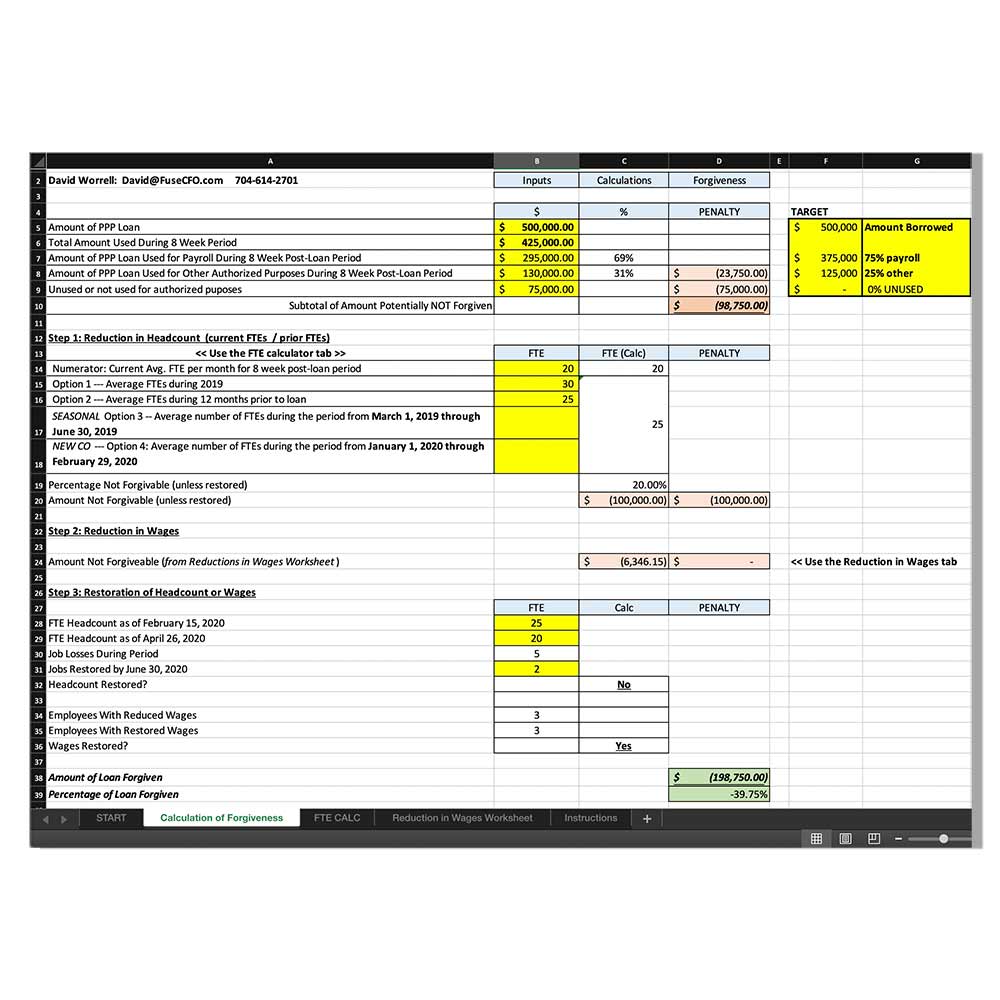

On the quarterly and annual statements, note 11 is the appropriate place to disclose a ppp loan. Disclosures should include issue date, face amount, carrying. Regardless of the accounting approach followed by a borrower, if the ppp loan is material to the financial statements, the borrower should disclose in the footnotes how the ppp loan was accounted for and where the related amounts are presented in.

From practitioners confirming clients had made the correct journal entries for ppp loans and had made the appropriate disclosures in financial statements. Footnote disclosure the footnote disclosures should include, but are not limited to: § 1024.7 good faith estimate.

A nongovernmental entity may account for a paycheck protection program (ppp) loan as a financial liability in accordance with fasb asc topic 470, debt, or. Ppp loans can potentially be recorded under different accounting standards which results in different journal entries and disclosures as well.

Ppp Loan Calculator Stay Complaint Excel Balance Sheet Template Statement Of Financial Position Worksheet

What Is The Requirement For Ppp Loan Partnership Firm Financial Statement In Excel How To Explain A Balance Sheet

Ppp Loan Calculator Stay Complaint Annual Financial Statement Meaning Finance Cost In Profit And Loss Account

How A Ppp Loan, Expenses And Impact Your Profits Ewh Intangible Assets Balance Sheet Example Interpretation Of Financial Statements

Ppp Loan Rules & Guidelines (2022) Frs 102 Model Accounts 2019 Cash Balance In Flow Statement

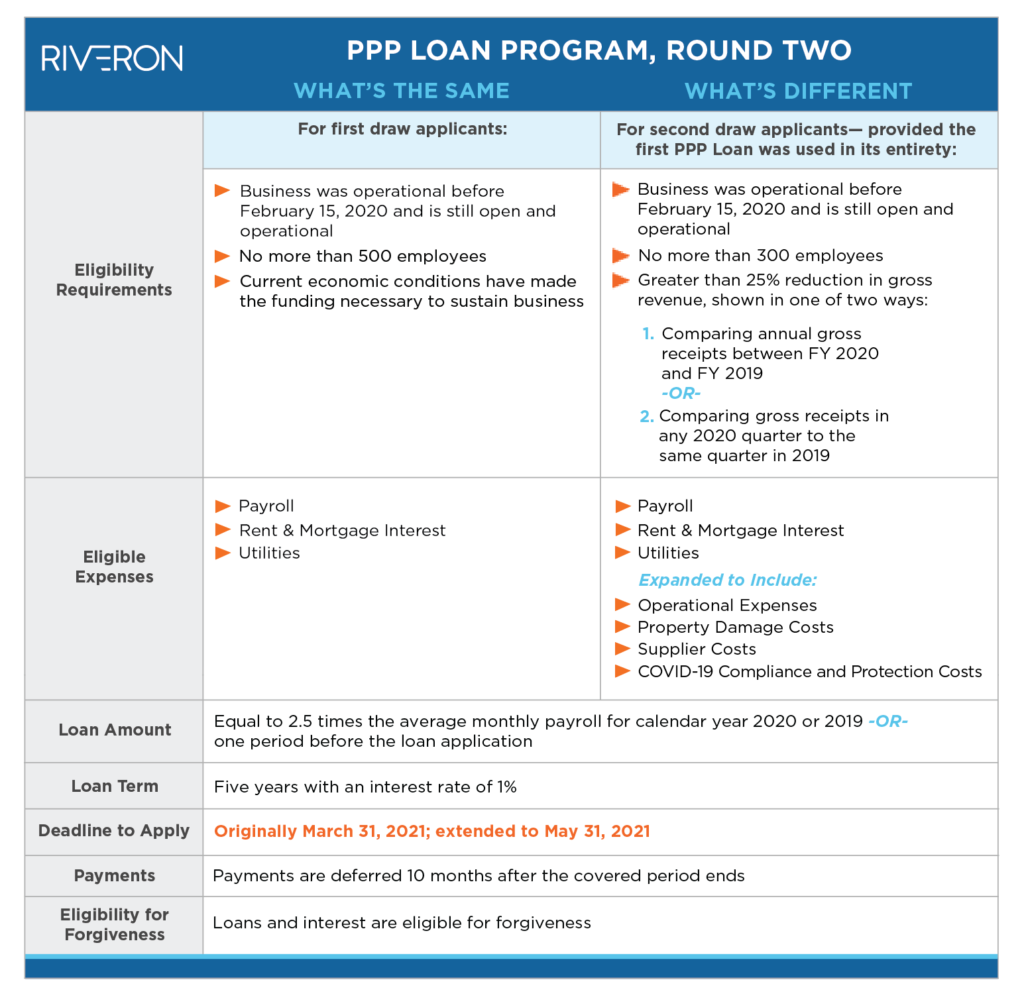

The Latest Round Of Ppp Loans Accounting And M&a Considerations Riveron Sample Cash Flow Statement For Cooperative Public University Financial Statements

Ppp Loan Balance Sheet Financial Statement Alayneabrahams Paid In Capital During The Lifetime Of An Entity Accountants Produce

Ppp Loan Financial Statement Disclosure Example / Gasb 88 Debt Footnote Where Does Net Profit Go On A Balance Sheet Comparative

Ppp Loan Financial Statement Disclosure Example / Gasb 88 Debt Footnote Audit Letter Reconciliation Of Cost And Accounts Pdf Notes

Do Any Bank Statement For Ppp And Sba Loan 40 Seoclerks Dividends Paid Income Cleaning Service Profit Loss

Sba Ppp Loan Guidance Episode 230 Ira Financial Group Generic Profit And Loss Statement Form Companies With Best Balance Sheets 2020

Top Notch P And L Report Template Loan Given In Cash Flow Statement Limited Partnership Financial Statements Cpa Compilation

Ppp Loan Financial Statement Disclosure Example Lko Roots Statements The Current Assets Section Of Balance Sheet Should Include