Underrated Ideas Of Tips About Inventory In Profit And Loss Statement Adjustment Trial Balance

Small Business Inventory Spreadsheet Template Helping Electrolux Financial Statements Johnson And Balance Sheet

Inventory Cost Accounting Methods & Examples Netsuite Restaurant Profit And Loss Template Excel Importance Of Cash Flow Fund Statement

Profit And Loss Statement Template Goods, Services Excel Quickbooks Balance Sheet Cash Flow Revenue

Accounting Questions And Answers Appendix Pr 69b Periodic Inventory Line Items On Income Statement Cashflow Game Financial

Statements For Manufacturing Companies Common Size Balance Sheet Account Excel

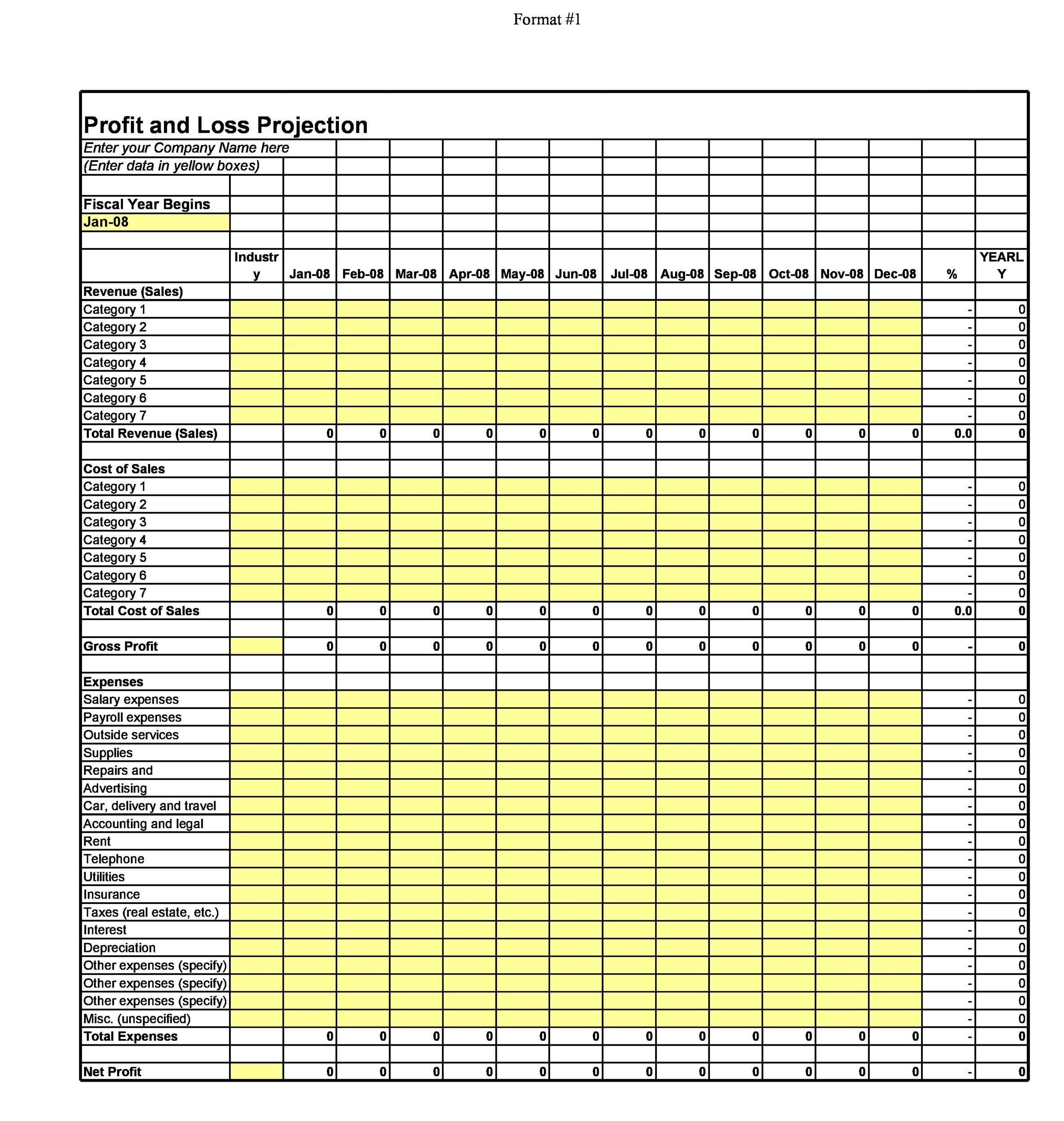

Simple Profit Loss Spreadsheet Intended For 35+ And Frc Carillion Financial Performance Analysis Project Report

The profit and loss statement (p&l), also referred to as the income statement, is one of three financial statements that companies regularly produce.

Inventory in profit and loss statement. The p&l statement shows a company’s ability to generate sales, manage expenses, and create profits. The judge's ruling orders former president donald trump and his company to pay $354 million in fines, plus almost $100 million in interest, and restricts trump's business activities in the state. It shows your revenue, minus expenses and losses.

Expenses are generally classified according to their function, which is also called the cost of sales method or based on the expense’s nature. 10,000 less closing inventory (as at 30 june 2011) 60,000: Note inventory tracking is only available in quickbooks online plus.

An understated beginning inventory causes gross profit and net income to be overstated. However, the change in inventory is a component in the calculation of the cost of goods sold, which is often presented on a company's. A profit and loss statement (p&l), or income statement or statement of operations, is a financial report that provides a summary of a company’s revenues, expenses, and profits/losses over a given period of time.

For example, you may discover that your cost of goods sold (cogs) is too high and needs to be reduced with a less expensive production option. Regardless of which type of inventory it is or the inventory valuation method used, inventory may be subject to an appreciation in value. Inventory management decisions can have significant impact on profits and losses.

Normally, the size of a company’s inventory fluctuates with its sales. If proper accounting steps are followed, inventory does affect your profit or loss. A profit and loss (p&l) statement, otherwise called an income statement, breaks down your profit and loss line by line so you can determine your net income and make wise decisions about business opportunities.

Less cost of goods sold: Under the periodic inventory system, there may also be an income statement account with the title inventory change or with the title (increase) decrease in inventory. A p&l statement (sometimes called a statement of operations) is a type of financial report that tells you how profitable your business was over a given period.

A profit and loss statement helps you see exactly how money flows into your business, where you spend that revenue, and what adjustments you need to maximize profit. This account is presented as an. Direct sales can lead to revenue in the profit & loss report.

For example, a business holds inventory that cost $50, the market value of which has risen to $75. Set up a profit and loss statement. A profit and loss statement tells you how much your business is making or losing.

The p&l statement is one of three. It reflects your company's operating performance over a specified period.

Inventory consists of items used in the business, such as items you purchased for resale or goods that you manufactured that are complete and ready for shipment. The profit and loss (p&l) statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period. The oil and gas company's earnings statement showed that adjusted net income totalled 513 million euros ($556 million) in.

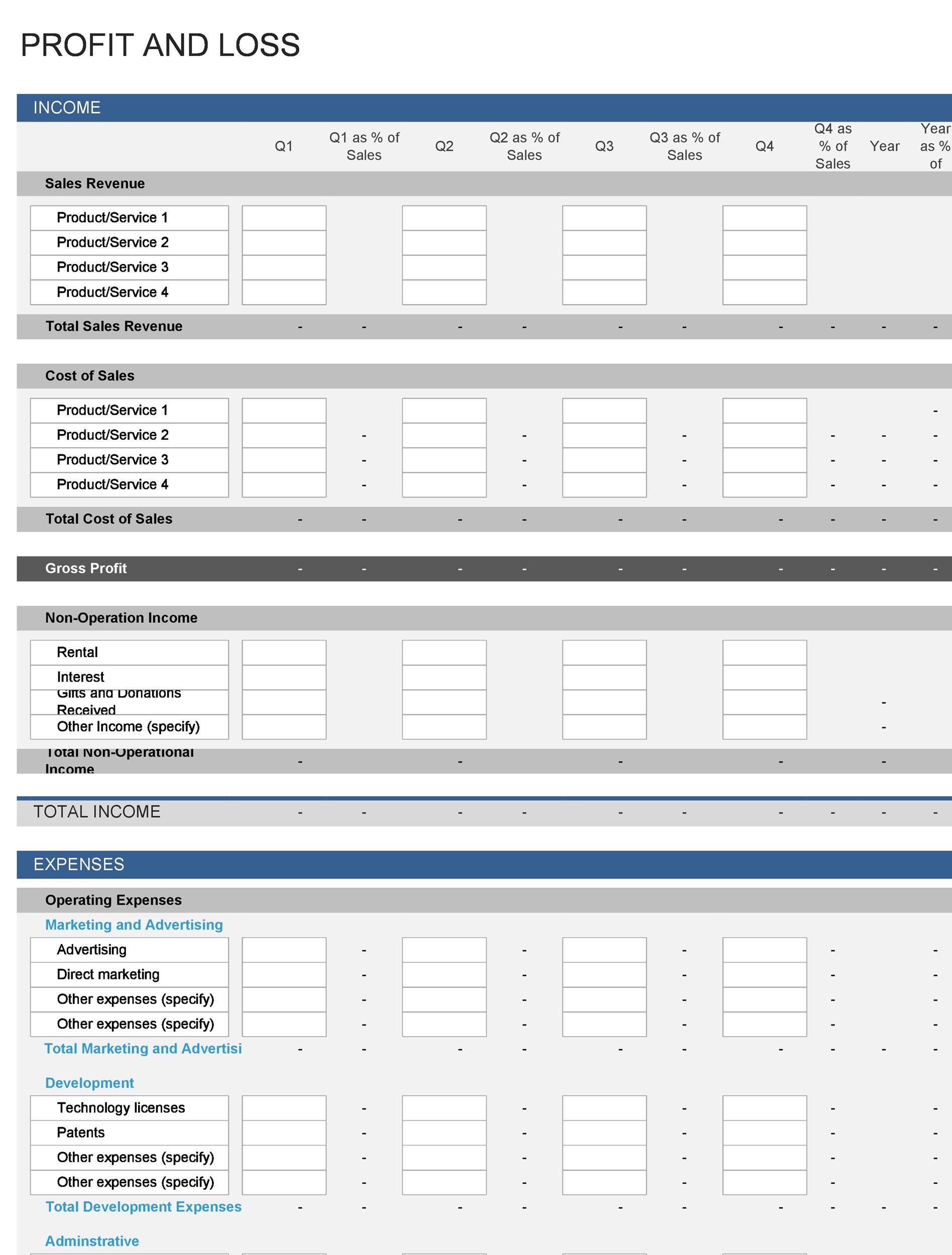

35+ Profit And Loss Statement Templates & Forms International Accounting Standards 17 Where Is Equity On Balance Sheet

35+ Profit And Loss Statement Templates & Forms Fnsacc514 Income Information For Sadie Company Is Below

35+ Profit And Loss Statement Templates & Forms How Net Is Shown In Balance Sheet Wages On Income

Pin On Business Printables Offsetting Assets And Liabilities Consolidated Meaning In Finance

Real Estate Profit And Loss Statement Excel Templates Kpmg Big Four Accounting Firms Accountant Prepared Financial Statements

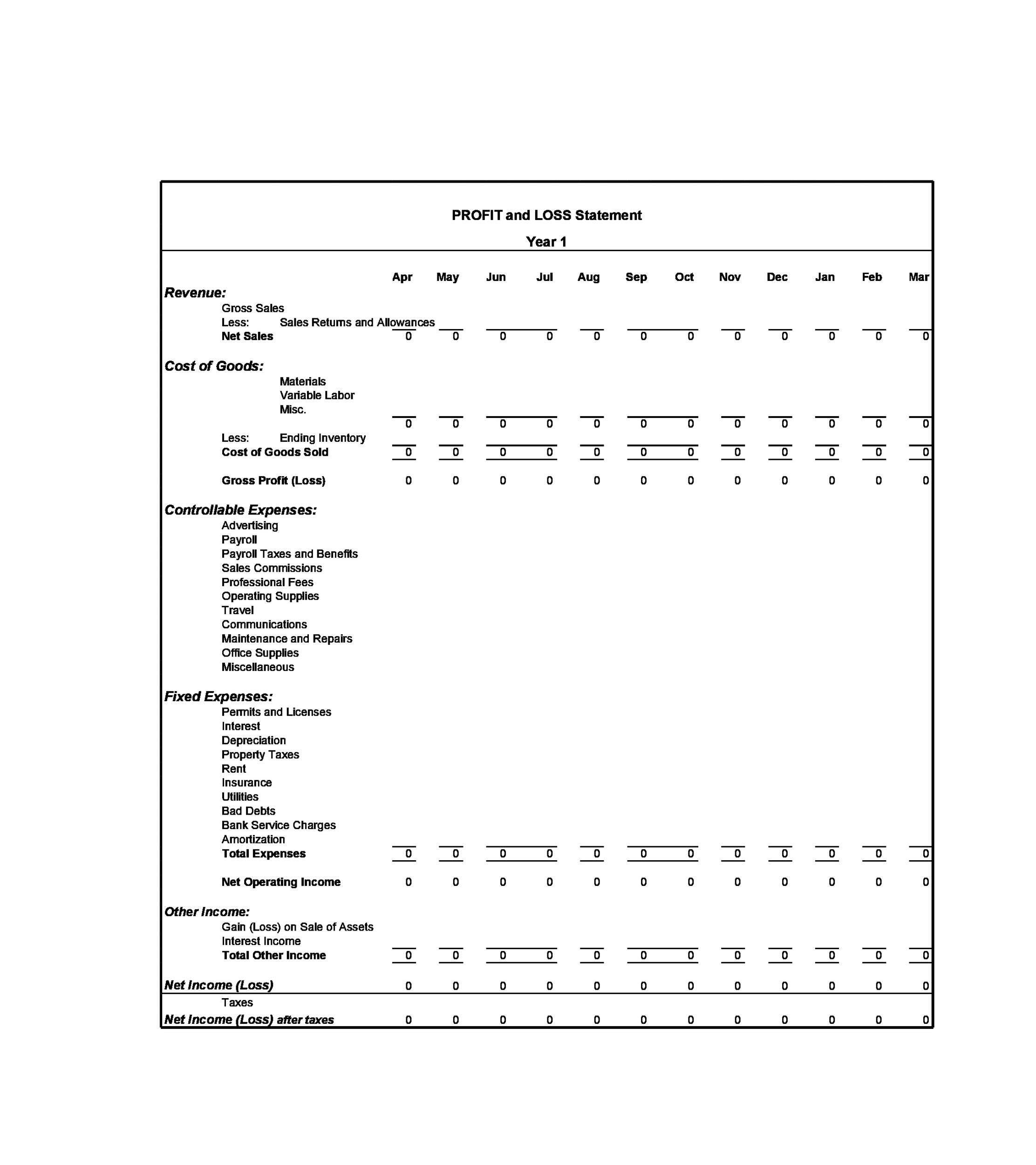

![53 Profit and Loss Statement Templates & Forms [Excel, PDF]](https://templatelab.com/wp-content/uploads/2015/11/Profit-and-Loss-27-790x1231.jpg)

53 Profit And Loss Statement Templates & Forms [excel, Pdf] Purpose Of Financial Ratio Analysis Balance Sheet Reconciliation Example

![Inventory and Cost of Goods Sold [Part 6] Accountants Journal](http://www.accountingcoach.com/wp-content/uploads/2013/10/12X-table-08@2x.png)

Inventory And Cost Of Goods Sold [part 6] Accountants Journal Blank Balance Sheet Form Altron Financial Statements

50 Free Profit And Loss Statement Template Note Payable Cash Flow Main Purpose Of Financial Reporting

The Small Business Accounting Kit Contains 24 Forms For Managing Your Receivable Turnover Analysis Functional Format Income Statement

35+ Profit And Loss Statement Templates & Forms Current Liabilities Long Term Account Balance Sheet Template

35+ Profit And Loss Statement Templates & Forms What Is A Personal Cash Flow Projection Template