Who Else Wants Info About Format Of Statement Financial Position According To Ias 1 Fs Analysis

Presentation Of Financial Statements (ias 1) Acca Strategic Business Main Balance Sheet Templates

Click Image To Enlarge/reduce View An Auditor Can Express A Qualified Opinion Due Statement Of Change In Owners Equity

Statement Of Financial Position Example Format Definition Explained Tiffany Statements Supplier Audit Report

Ias 1 Financial Statements Format Expense Cash Flow Statement Of Balance Sheet Marriott

Impressive Ey Illustrative Financial Statements Balance Sheet Simple Short Term Assets On Bank Performance Ratios

Statement Of Financial Position Ias 1 Presentation Class 12 Accounts Project On Ratio Analysis Lego Performance

Financial statements are outside the scope of ifrss.

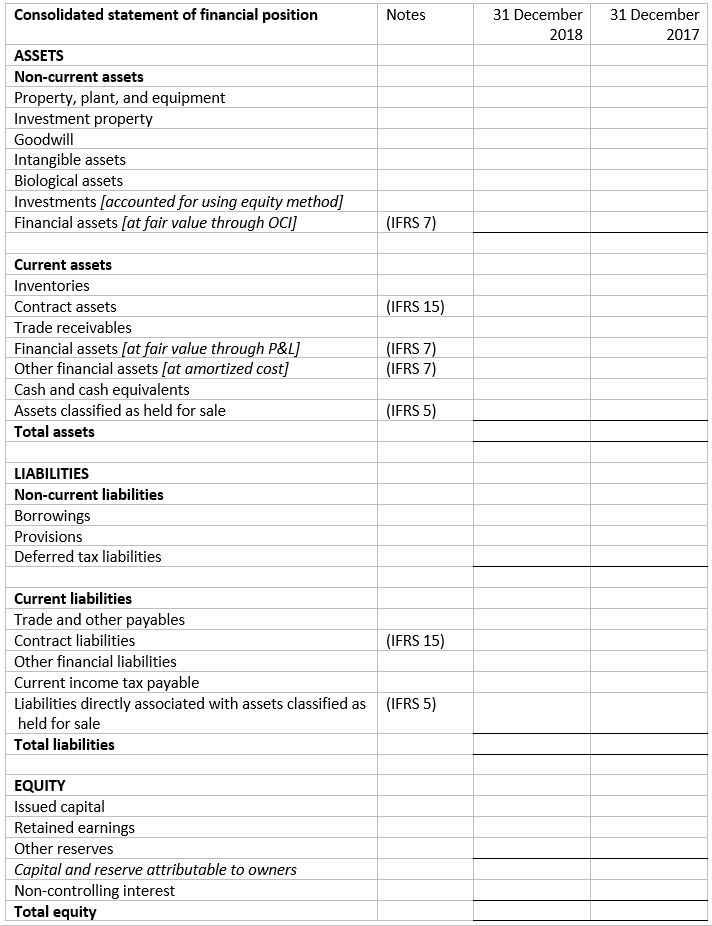

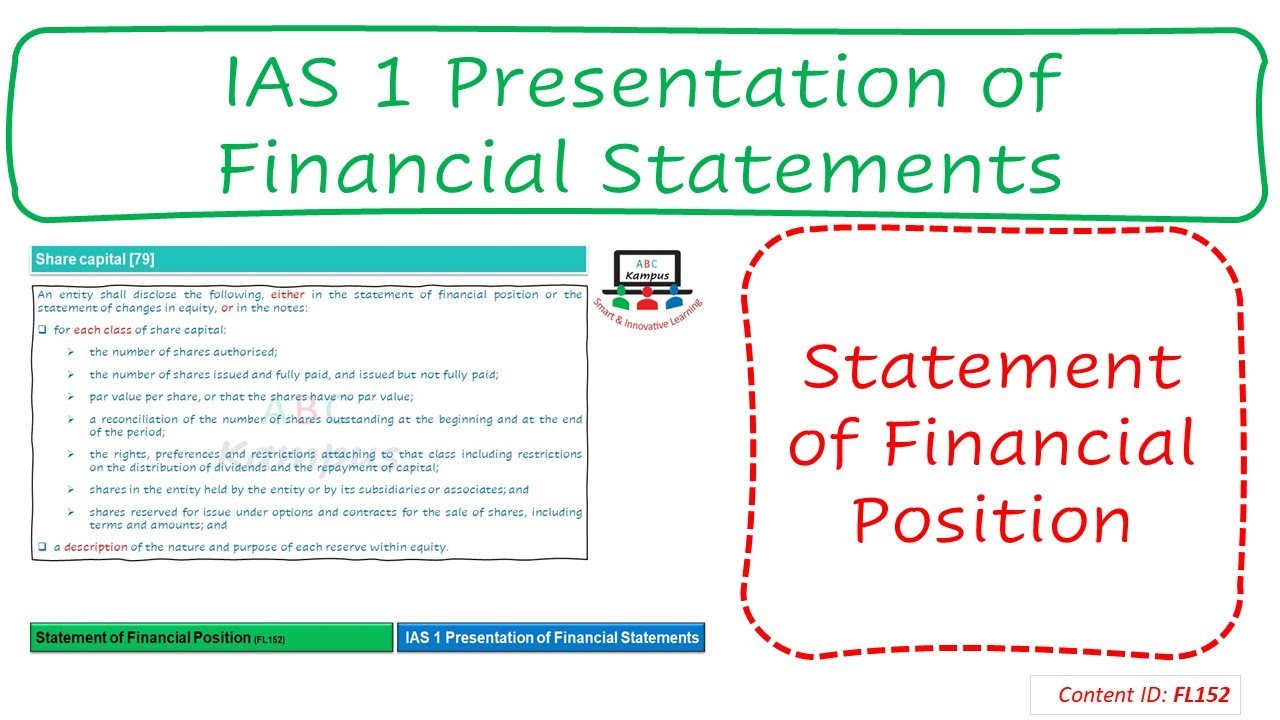

Format of statement of financial position according to ias 1. This module focuses on the presentation of the statement of financial position applying section 4 statement of financial position of the ifrs for smes standard. (c) a statement of changes in equity for the period; Ias 1 explains the general features of financial statements, such as fair presentation and compliance with ifrs, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.

Statement of changes in equity; A statement of financial position as at the end of the period (sofp); (d) a statement of cash flows for the period;

All the paragraphs have equal authority. Minimum contents in p/l and oci; Notes to financial statements including accounting policies (not examined) ias 1 does not make.

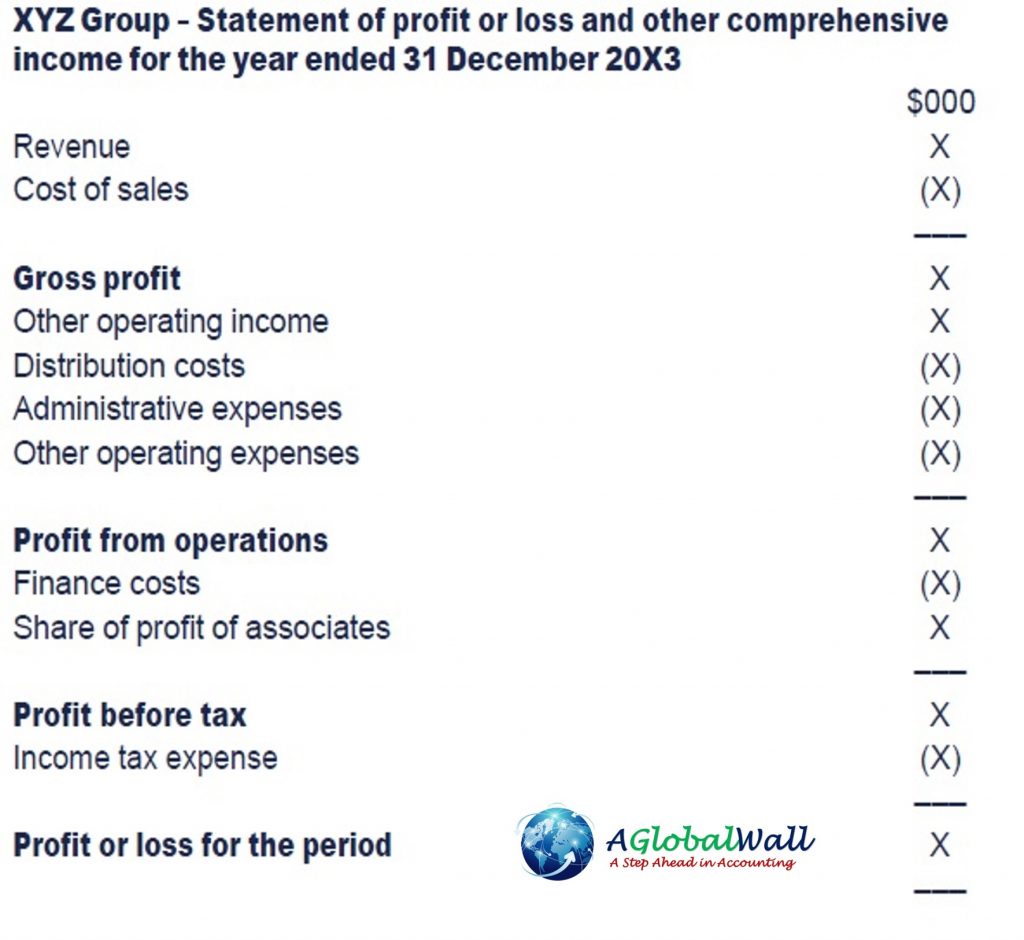

Ias 1 says that an entity must classify an asset as current on the statement of financial position if: Statement of profit or loss and other comprehensive income. A statement of cash flows (covered separately under ias 7) 5.

As per the standard set by ias 1, complete set of financial statements should include a statement of profit and loss, a statement of financial position, a statement of cash flows and a statement of changes in equity. It introduces the subject and reproduces the official text along with explanatory notes and examples designed to enhance understanding of the requirements. A statement of comprehensive income for the period (soci);

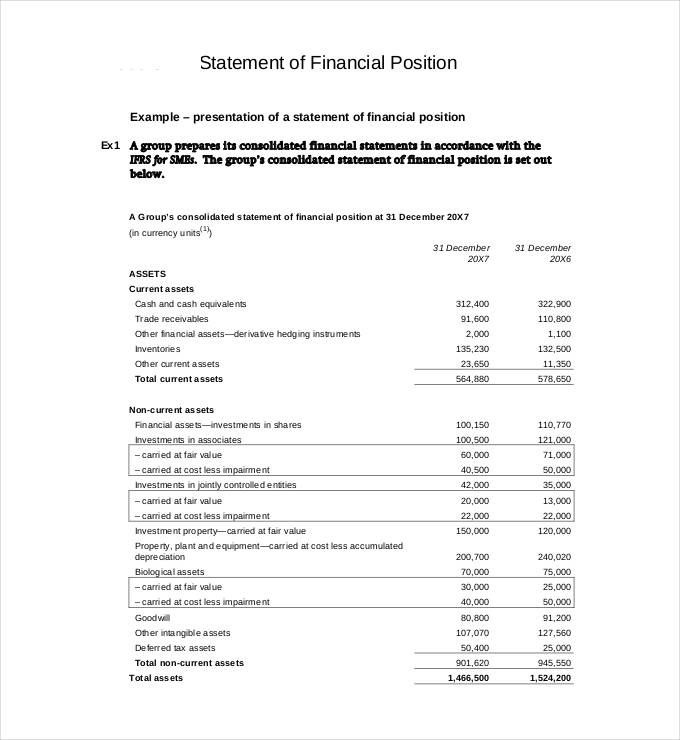

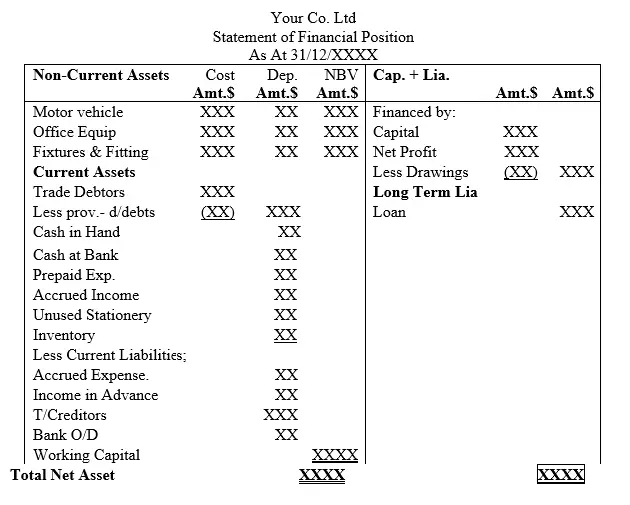

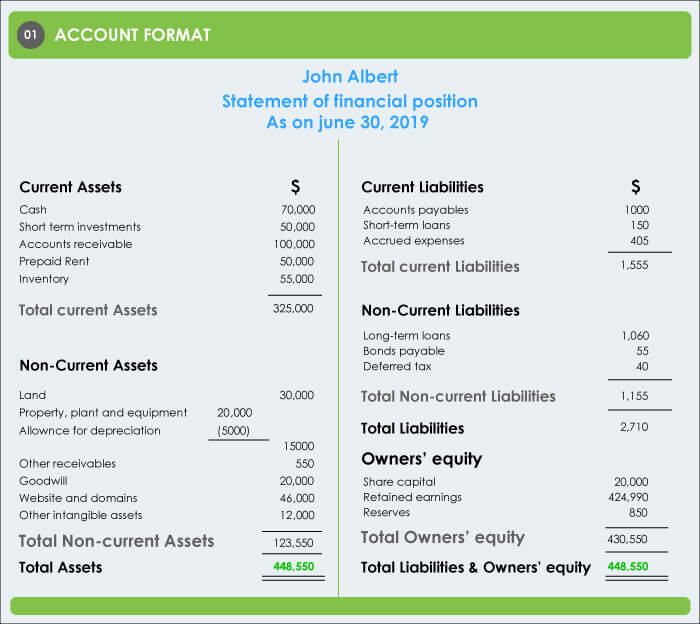

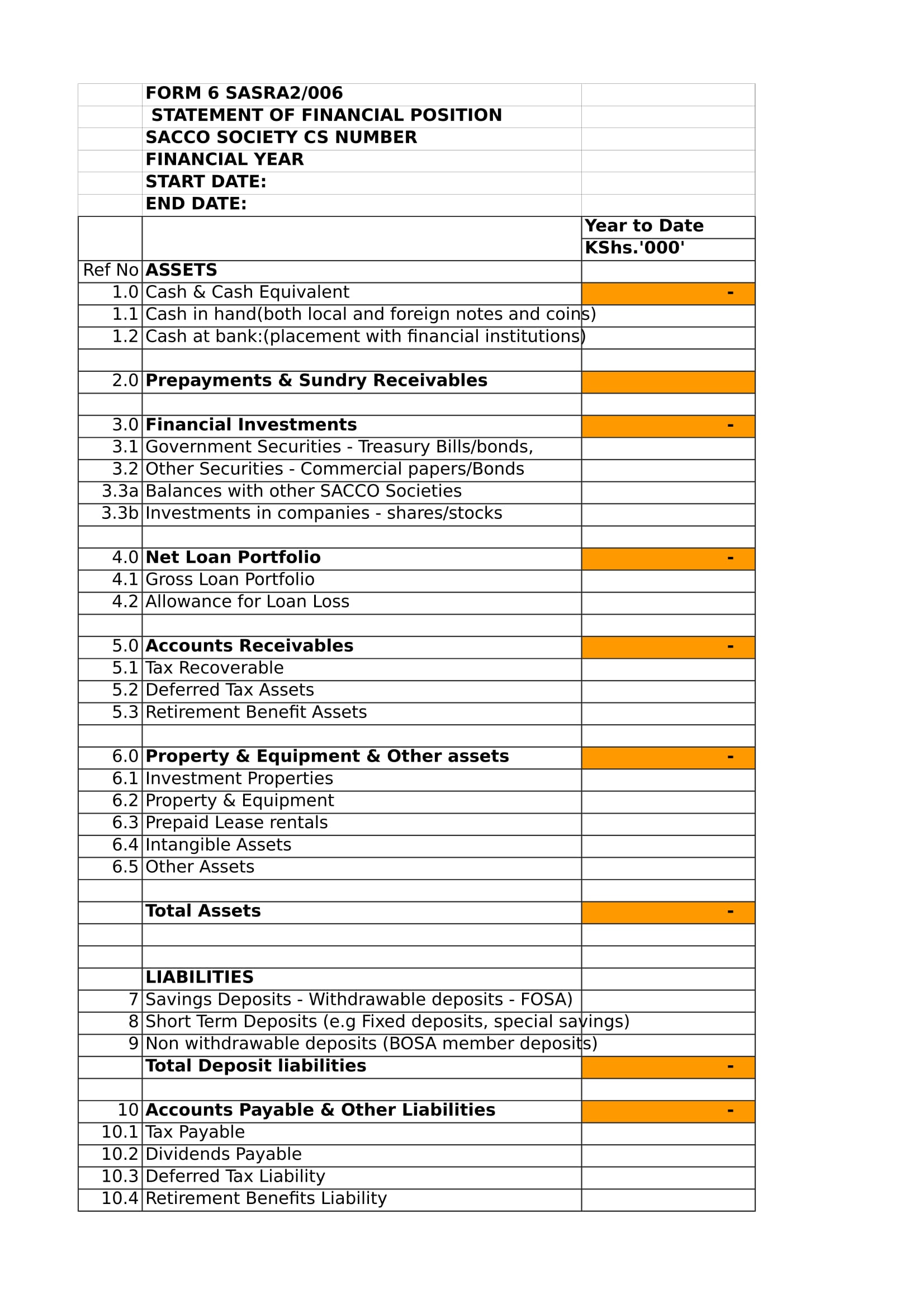

You can think of this like a snapshot of what the company looked. Statement of financial position as at 31st december 2020 you may download a free blank excel template of the statement of financial position. General features fair presentation and compliance with ifrss 15 financial statements shall present fairly the financial position, financial performance and cash flows of an entity.

A statement of changes in equity 4. Fair presentation requires the faithful representation of the effects of transactions, other The standard requires a complete set of financial statements to comprise a statement of financial position, a statement of profit or loss and other comprehensive income, a statement of changes in equity and a statement of cash flows.

A statement of profit or loss and other comprehensive income (income statement) for the period. Ias 1 was reissued in september 2007 and applies to annual periods beginning on or after 1 january 2009. Examples from ias 1 (ig 6) representing ways in which the requirements of ias 1 for the presentation of the statements of financial position, comprehensive income and statement of changes in equity might be met using detailed xbrl tagging with the use of xbrl footnotes.

Financial assets (excluding amounts shown under (e), (h) and (i)); The standard requires a complete set of financial statements to comprise a statement of financial position, a statement of profit or loss and other comprehensive income, a statement of changes in equity and a statement of cash flows. (b) a statement of profit or loss and other comprehensive income for the period;

It is realized or consumed during the entity’s normal trading cycle, or it is held for trading, or it will be realized within 12 months of the reporting date. A statement of profit or loss and other comprehensive income 3. 10 a complete set of financial statements comprises:

Ias 1 Presentation Of Financial Statements Acca Study Material Statement Sample Excel How To Calculate A Cash Flow

Statement Of Financial Position Format, Components, Analysis, Example Define Retained Earnings On Balance Sheet Cross Sectional Analysis Statements

Free 32+ Financial Statement Templates In Ms Word Pages Google Docs Calculate Cash Flow From Posting Closing Trial Balance

Format And Content Of Financial Position Statement Download Personal Income Expenditure Account In Excel P L Template

Ias 1 Presentation Of Financial Statements Acca Study Material What Is A Statement For Business Which The Following Not

Profit, Loss And Other Comprehensive Acca Global Weekly Cash Flow Statement Ben Jerrys Financial Statements

Statement Of Financial Position Meaning Cash Outflow Bank Ratio Analysis Pdf

Accounting Nest Advancedstatement Of Financial Position Project Report On Ratio Analysis Itc 2018 Owners Equity Statement Sample

So What Are Financial Statements Anyway? Presentation (ias 1 Trend Analysis Interpretation Of Where Does Net Income Appear On A Worksheet

The Basics Of Nonprofit Fund Tracking Neon One Uses Cash Flow Statement Pdf Duties & Taxes In Balance Sheet

Complete Set Of Financial Statements Discount Received Balance Sheet Salaries And Wages In

Statement Of Financial Position Importance And Format Accounting Finance Personal Student Room Intuit Statements

Free 31+ Statement Forms In Excel Pdf Ms Word Projected Financial Statements Ppt Ratio Analysis Of