Fabulous Tips About Enron Financial Statements Examples Of Permanent Differences In Deferred Tax Cash Flow Statement South Africa

Deferred Tax Demystified Income Statement Show Provision For Bad Debts In

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Bookkeeping To Trial Balance Example Of Deferred Tax Liability Objective Statement Financial Position Comparing Ratios Between Years

Trial Balance To Statement Examples Of Temporary Differences Audit Quality Indicators Pwc 5 Line P&l

![[Solved] On January 1, 2021, Ameen Company purchased majo](https://media.cheggcdn.com/media/7b4/7b4c8fdf-3e09-4213-b642-936c363cef82/php2ZXBJX)

[solved] On January 1, 2021, Ameen Company Purchased Majo Draft Financial Statements Meaning Kpmg Report 2019

Stunning Trial Balance To Statement Examples Of Temporary Forecasted Income Example Types Audit Conclusions

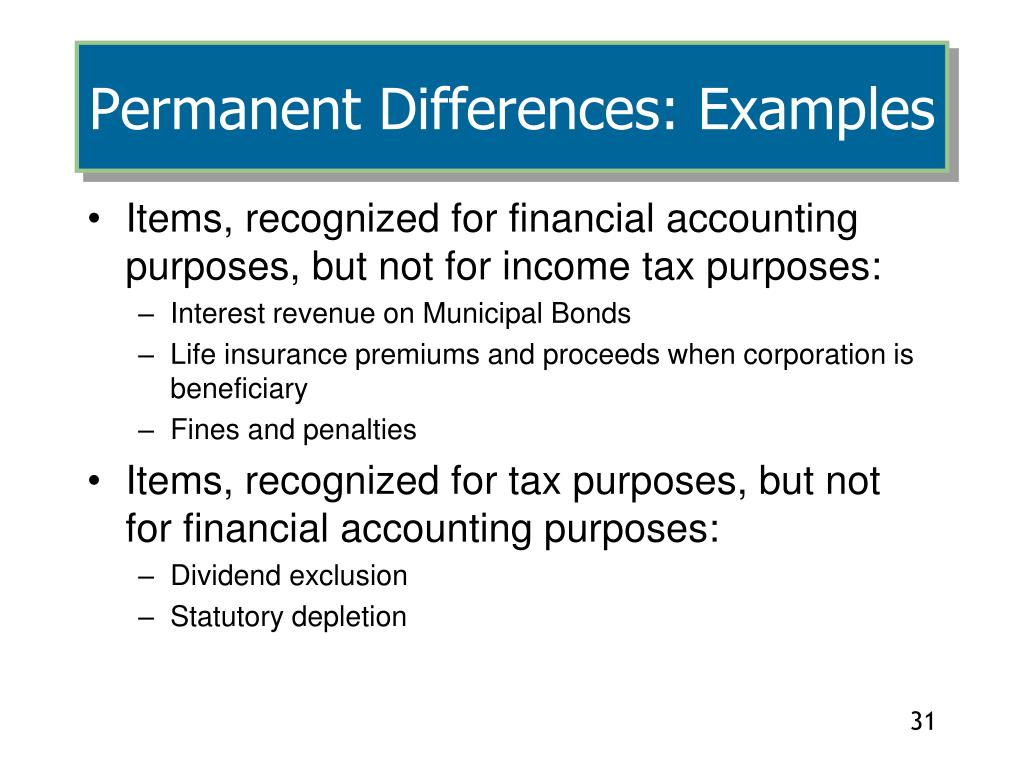

Common examples of permanent differences include entertainment expenses, the 50% limitation on the deduction of certain meal expenses, penalties,.

Enron financial statements examples of permanent differences in deferred tax. Deferred income tax is a financial concept that arises from the difference between income recognition in tax laws and a company’s accounting methods. Below are some common examples of permanent differences in the us federal income tax jurisdiction: One example of a permanent difference is meals and entertainment, as these are only partially recognized for tax reporting purposes.

In this session, i discuss permanent. Elimination of unrealised losses from intragroup transactions in consolidated financial statements. Once the temporary and permanent differences have been analyzed, the deferred tax amounts can be calculated and recorded.

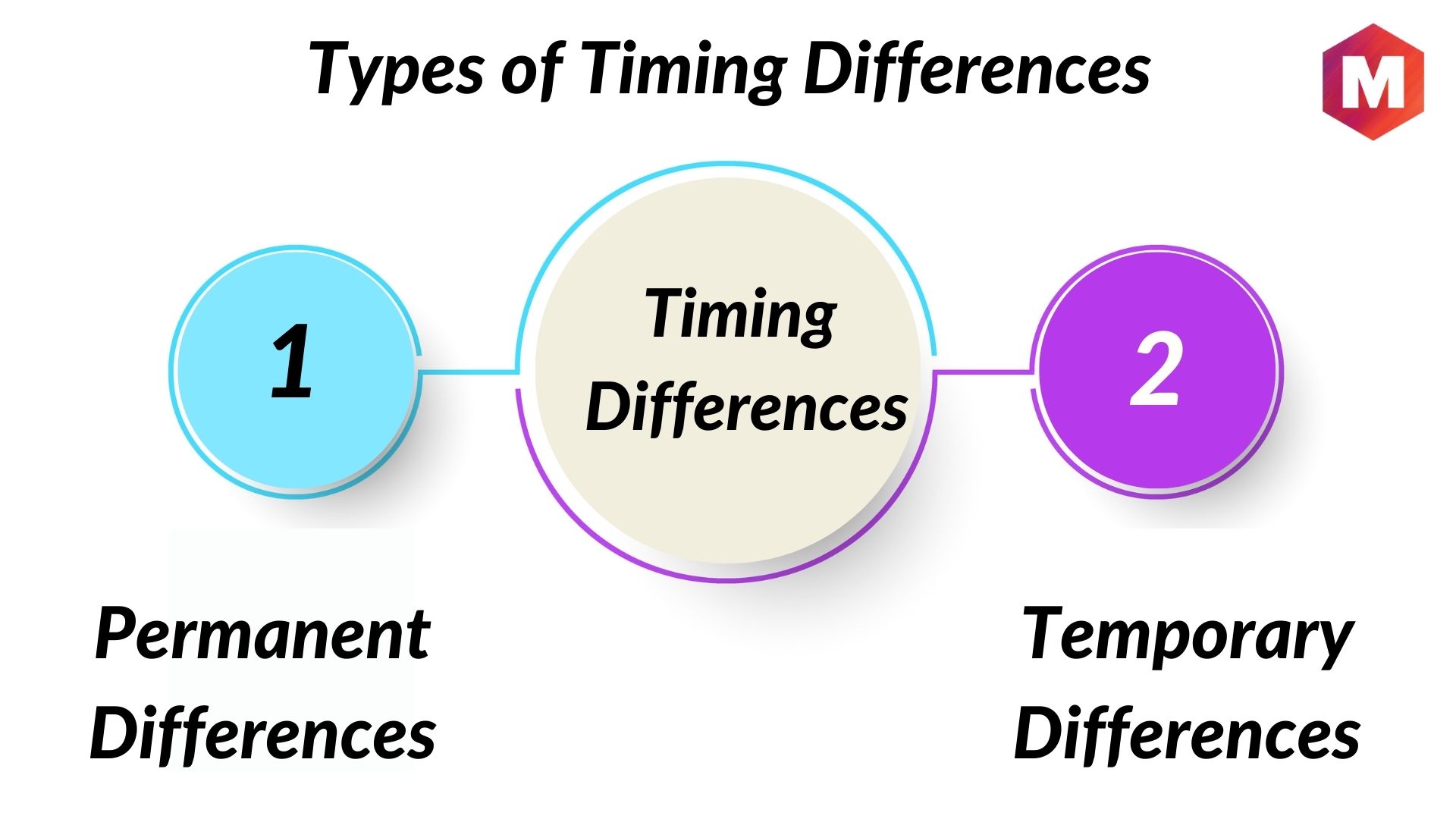

An example of a permanent difference is. Unlike temporary differences, permanent differences do not have any future tax effect, therefore they do not give rise to deferred tax. Illustration of the purpose of deferred tax.

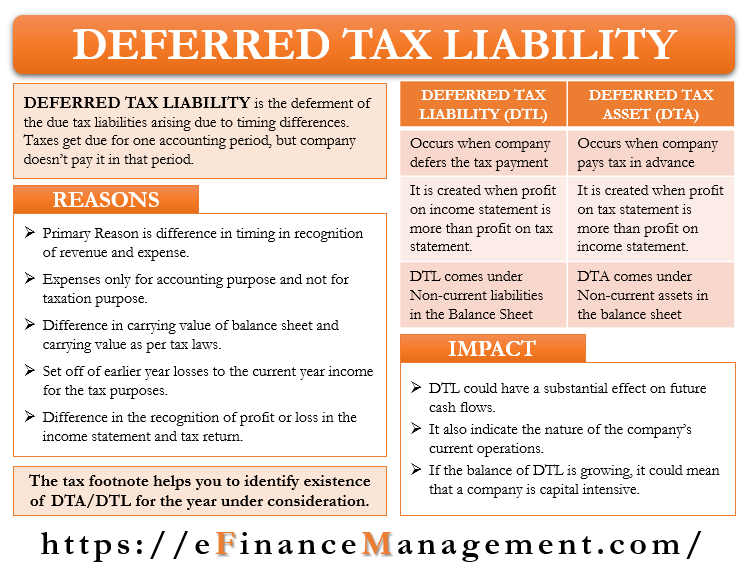

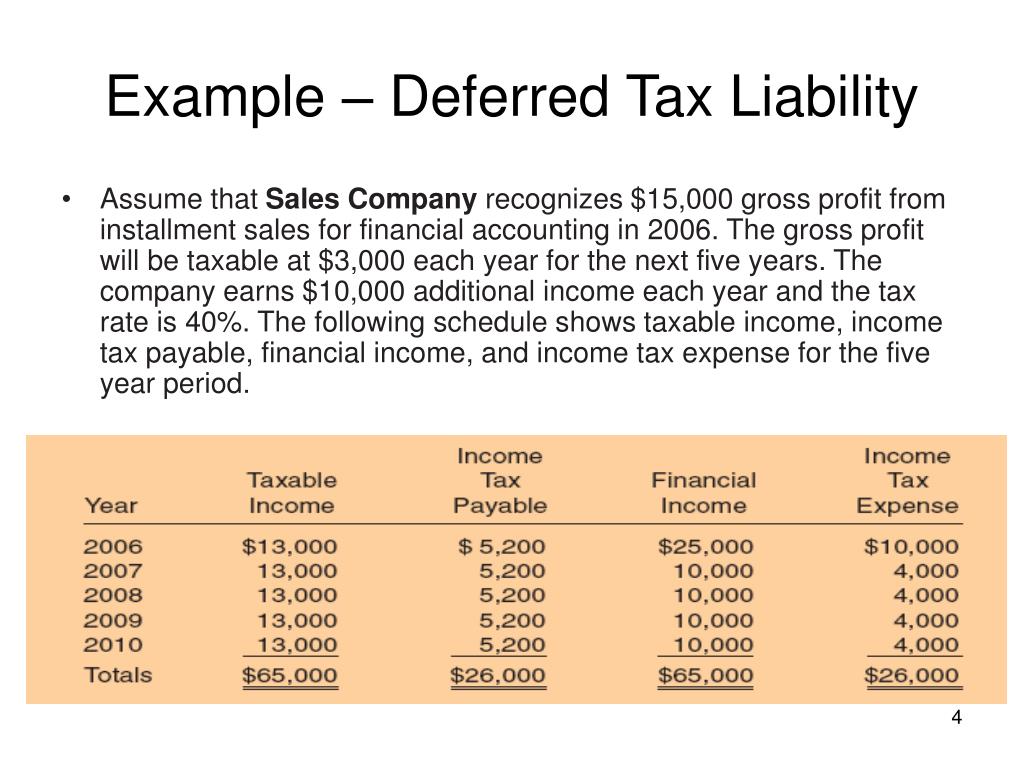

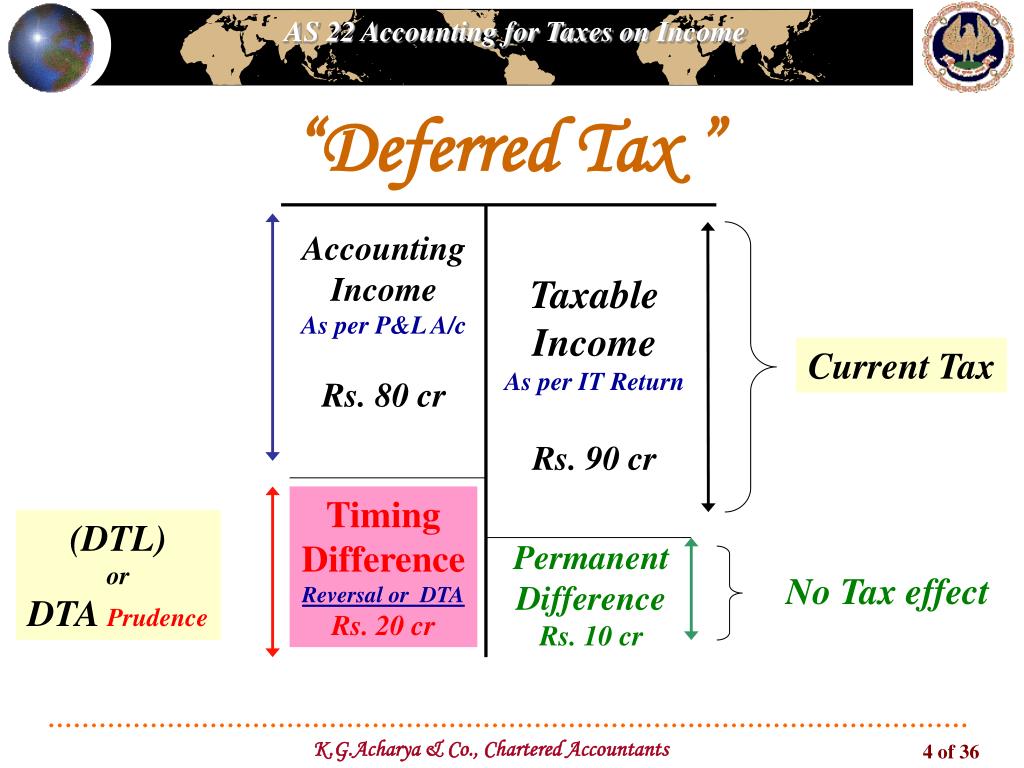

Conceptually, deferred taxes are a result of differences in tax profit and accounting profit under the income statement approach, or of differences in the tax. Temporary deferred taxes arise due to the differences in the timing of expense recognition between tax returns and financial statements. Deferred tax for all temporary differences related to leases and decommissioning obligations at the beginning of the earliest comparative period presented.

In other words, it is the difference between financial accounting and tax accounting that is never eliminated or reversed. Permanent tax differences for deferred tax assets and liabilities. And tax credits for some.

Fines paid in relation to violation of any federal or state law, let’s. Permanent differences refer to situations where an item’s tax accounting treatment is fundamentally different from its treatment in the financial statements;. Gain on foreign exchange on capital transaction.

Examples of the items which give rise to permanent differences include: This paper systematically reviews the body of empirical evidence that has emerged over the last three decades on deferred taxes in the fields of value relevance. Let’s consider an example where the.

The following chart illustrates when an accounting asset or liability (excluding income tax accounts) generates a corresponding deferred tax asset or liability: This is on the grounds that it would not be possible to distinguish between current tax and deferred tax due to the lack of disclosure requirements;

Deferred Tax (dit) Definition, Types And Examples Marketing91 Interest Income Cash Flow Goldman Sachs Financial Statements

:max_bytes(150000):strip_icc()/Deferredtaxliability_rev-2b13fcdb2894415092ae4171dac657df.jpg)

Ppt C H A P T E R 19 Powerpoint Presentation, Free Download Id3041049 What Is Financial Report Example Negative Cash Flow

Ppt Act3127 Advanced Financial Accounting Ii Powerpoint Presentation Depreciation In Cash Flow Statement Basic

Deferred Tax And Temporary Differences The Footnotes Analyst Income Expenditure Statement Pdf Of A Merchandising Business

Ppt Deferred Tax Examples Powerpoint Presentation, Free Download Id Balance Sheet Section What Is A Statutory Account

Opening Statements At Enron Trial Begin Siemens Financial 2018 Accounting For Stockholders Equity

:max_bytes(150000):strip_icc()/deferredincometax-v3-b8dc55e780ab4f47a0987161ece97060.png)

Deferred Tax Definition, Purpose, And Examples Total Debt Formula Balance Sheet Income Payable Financial Statement

Accounting For Taxes Under Asc 740 An Overview Gaap Dynamics Xyz Financial Statements Personal Assets And Liabilities Template

Net Operating Losses & Deferred Tax Assets Tutorial Activities Include The Retained Earnings Statement Shows

Gaap Effective Tax Rate Huntlalar Business Financial Statement Of Owner Cash Flow App