Smart Tips About Cash Flow From Operating Activities Indirect Method Share Market Balance Sheet

Cash Flows From Operating Activities The Indirect Method How Do You Make An Income Statement Big Five Audit Firms

Solved Cash Flows From Operating Activities For Both The Basic Balance Sheet Example Benefits Of Pro Forma Statements

Cash Flows From Operating Activities Indirect Method Youtube Insurance Company P&l Multi Step Income Statement

Operating Cash Flow (ocf) Formula And Calculation 4 Key Financial Statements Multi Step Income Statement Template

Solved Cash Flow From Operating Activities (indirect Method) Notes To Accounts Format For Private Limited Company Financial Statements Are Used

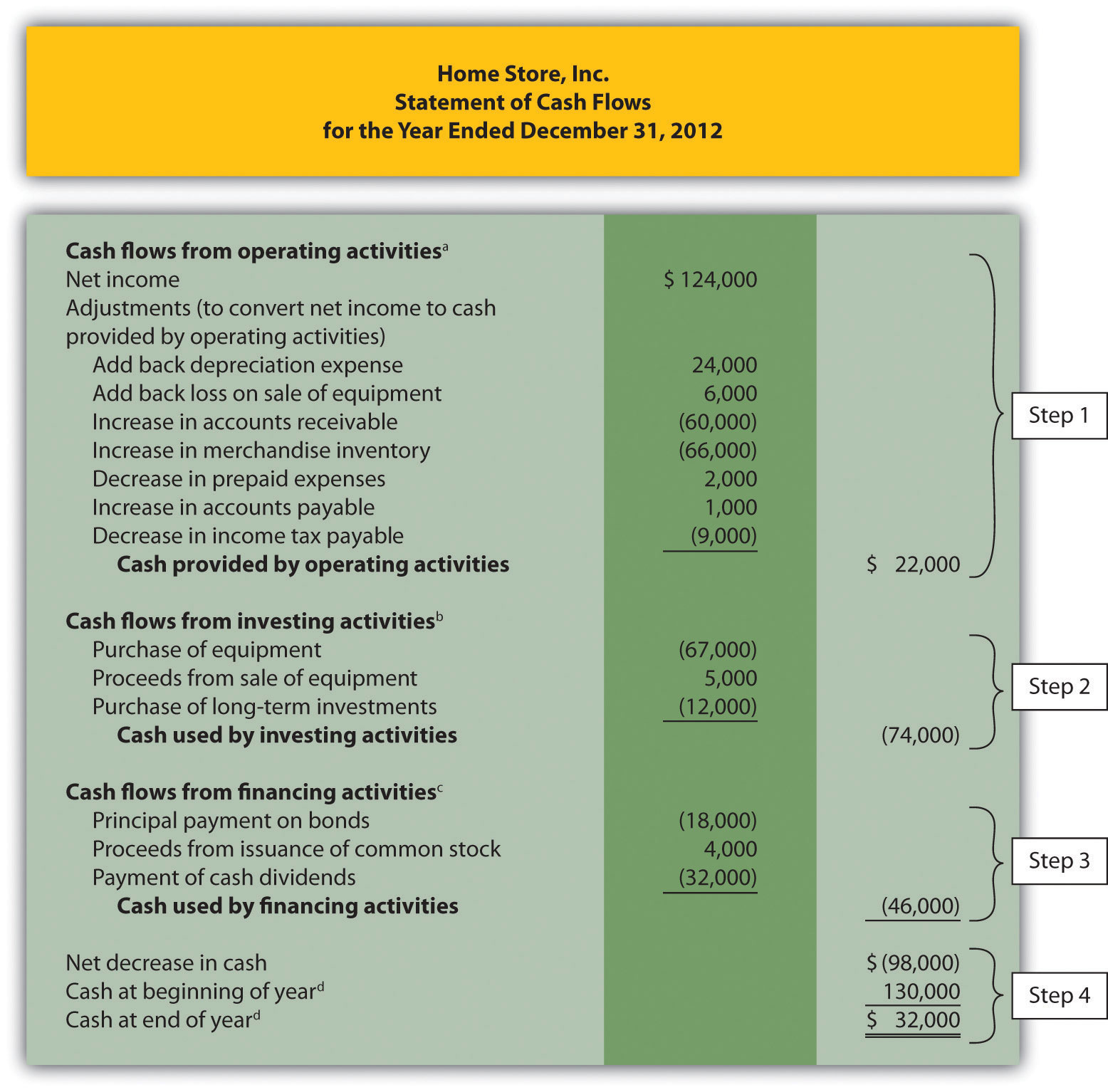

16.3 Prepare The Statement Of Cash Flows Using Indirect Method Comprehensive Income And Other Financial Statements Pharmaceutical Companies

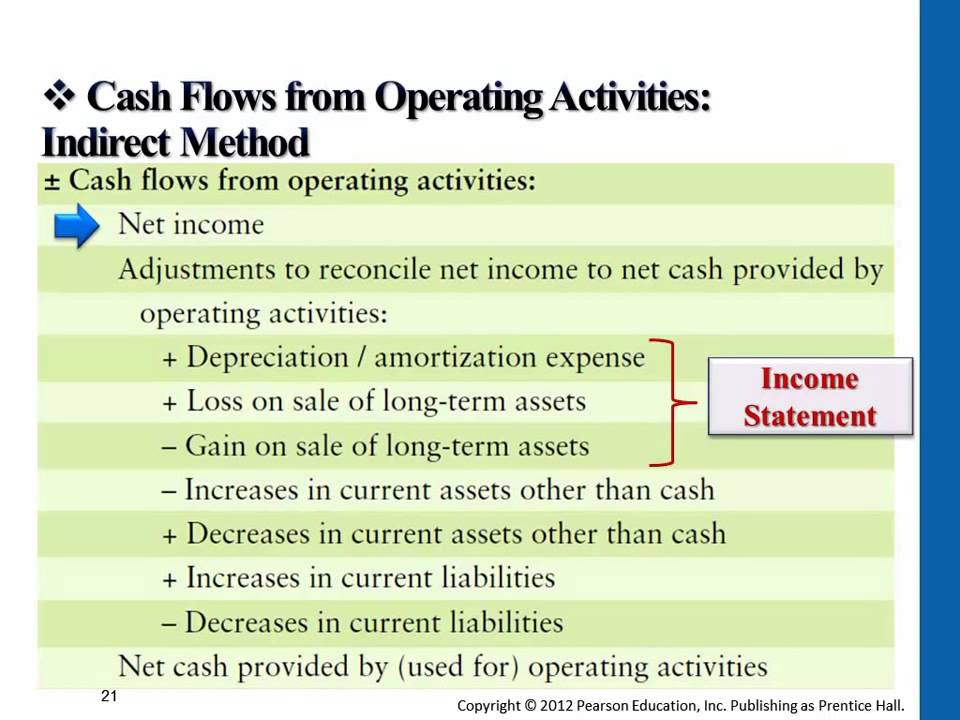

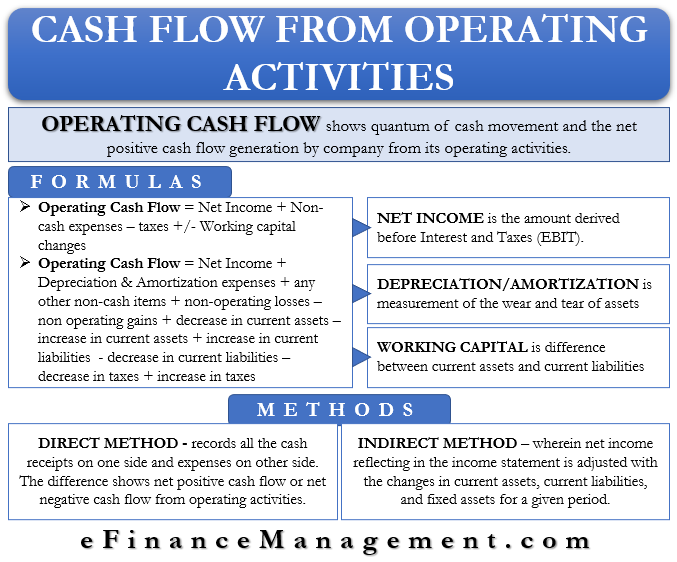

Add back noncash expenses, such as depreciation, amortization, and depletion.

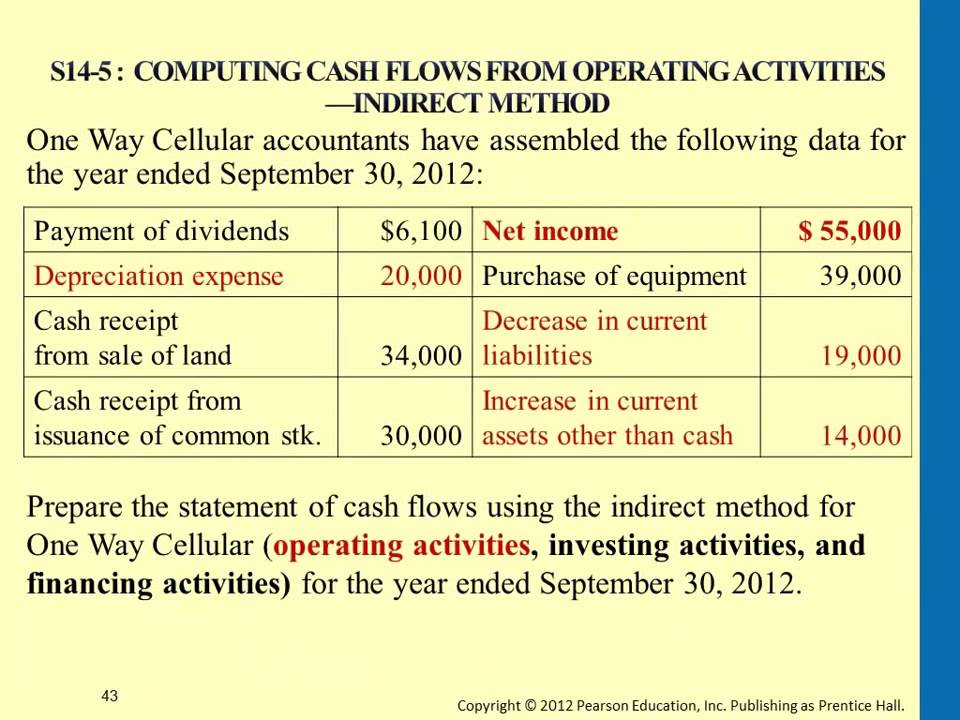

Cash flow from operating activities indirect method. In other words, changes in asset and liability accounts that affect cash balances throughout the year are added to or subtracted from net income at the end of the period to. The final section of the statement reconciles the net change in cash flows of the three activities, with the opening and closing cash and cash equivalents balances taken from the balance sheet. The idea is to use simple transactions to:

Cash flow from investing activities. Cash flow from operations is the first of the three parts of the cash flow statement that shows the cash inflows and outflows from core operating the business in an accounting year; Here we will study the indirect method to calculate cash flows from operating activities.

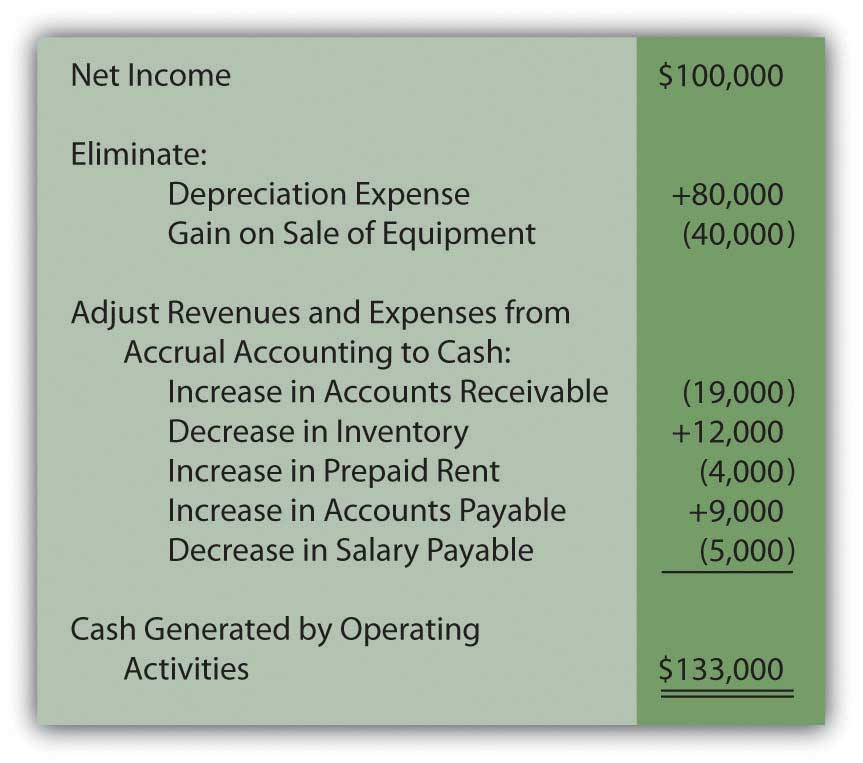

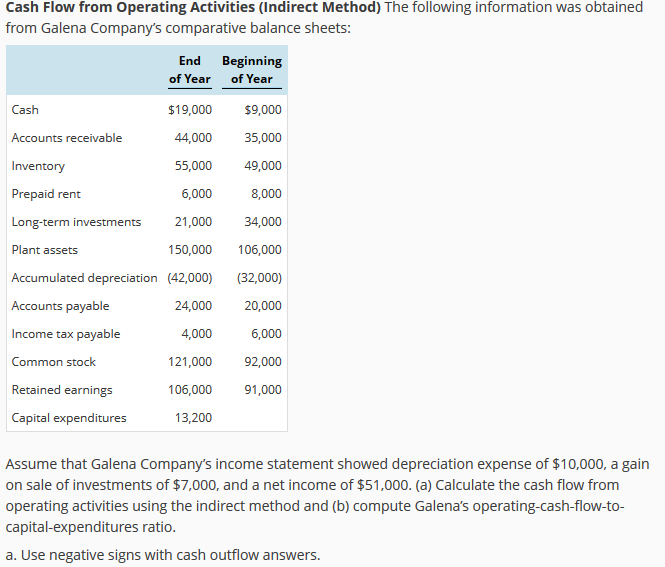

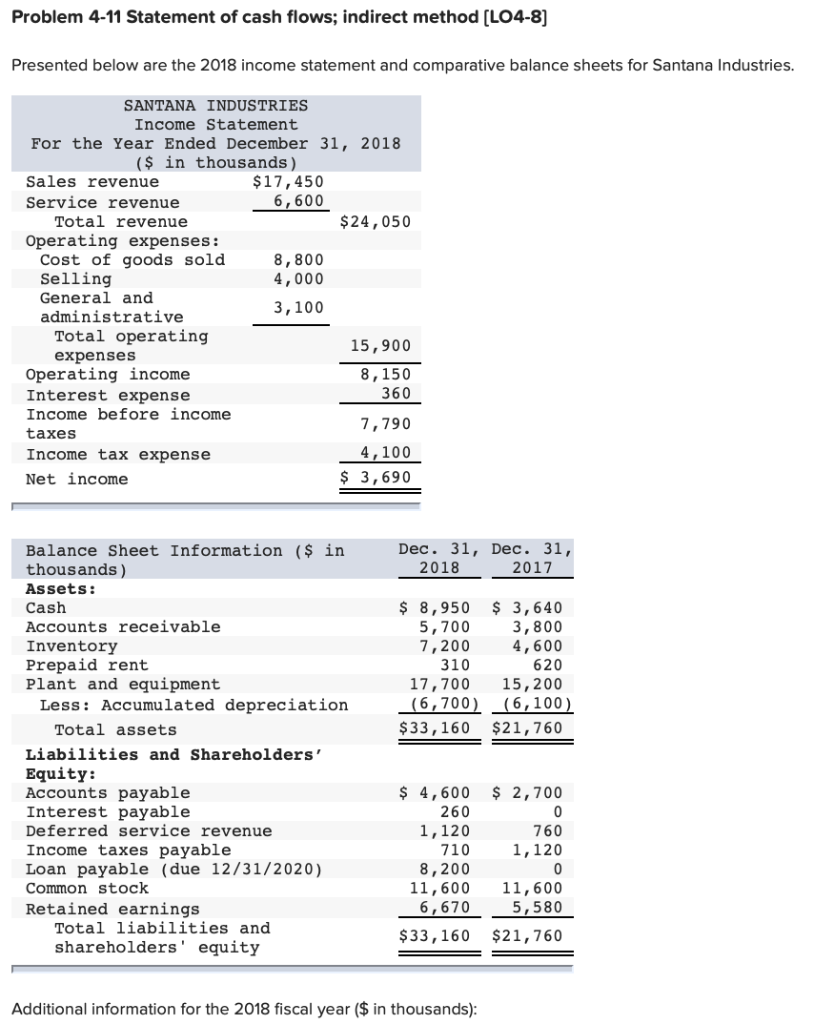

Presented below is the balance sheet and income statement for watson ltd. This presentation begins with net income and then eliminates any noncash items (such as depreciation expense) as well as nonoperating gains and losses. The statement of cash flows is prepared by following these steps:

Below is an example of the cash flow from the operations segment of a cash flow statement prepared under ifrs using the indirect method: Introduce basic concepts, such as assets, liabilities and net income; Determine net cash flows from operating activities.

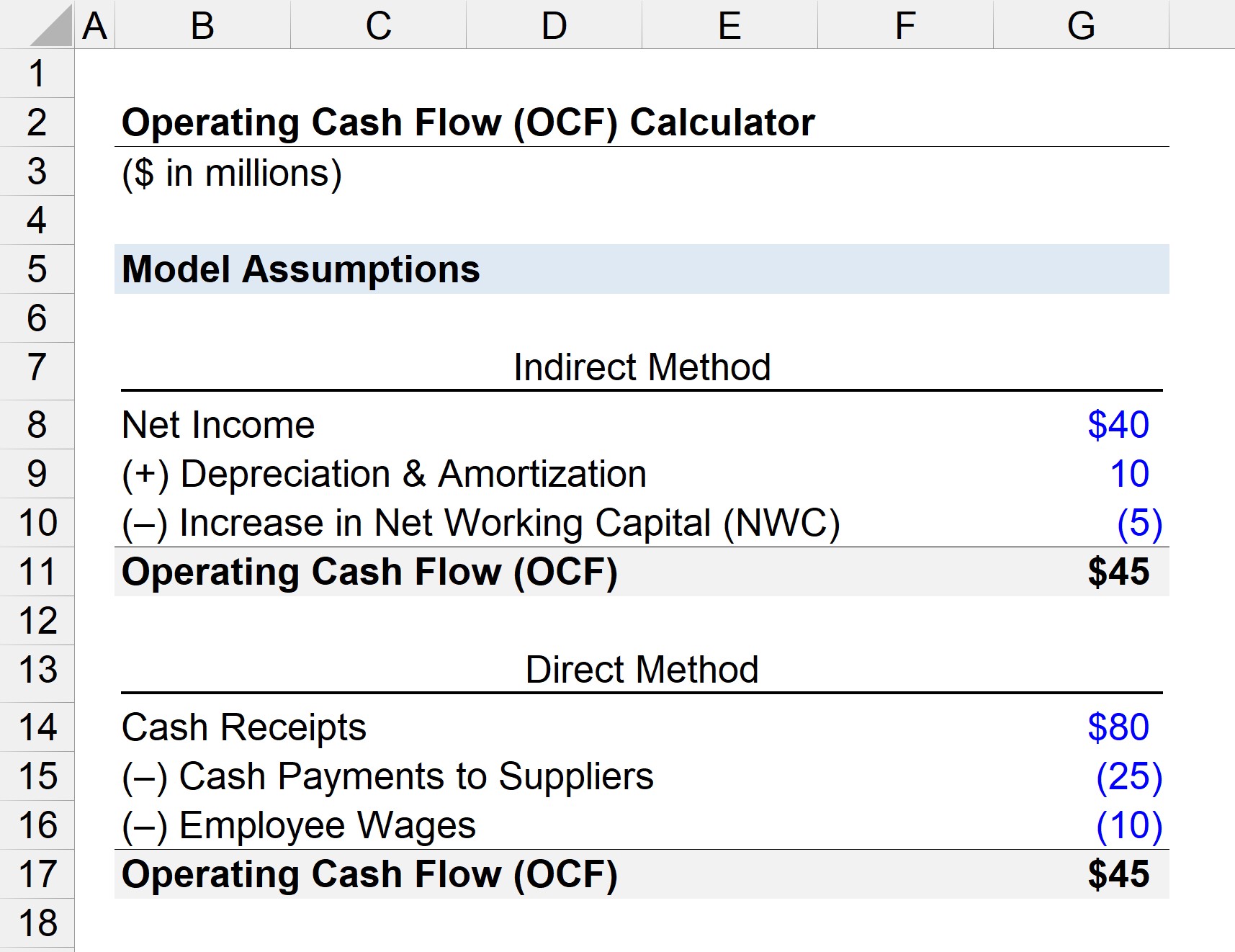

The cash flow statement indirect method is one way to present a company’s total cash flow. The statement of cash flows prepared using the indirect method adjusts net income for the changes in balance sheet accounts to calculate the cash from operating activities. Indirect method cash flow from operations:

This presentation begins with net income and then eliminates any noncash items (such as depreciation expense) as well as nonoperating gains and losses. Under the indirect method, cash flow from operating activities is calculated by first taking the net income from a company's income statement. The first figure we start with when calculating operating cash flows the indirect way is the profit figure.

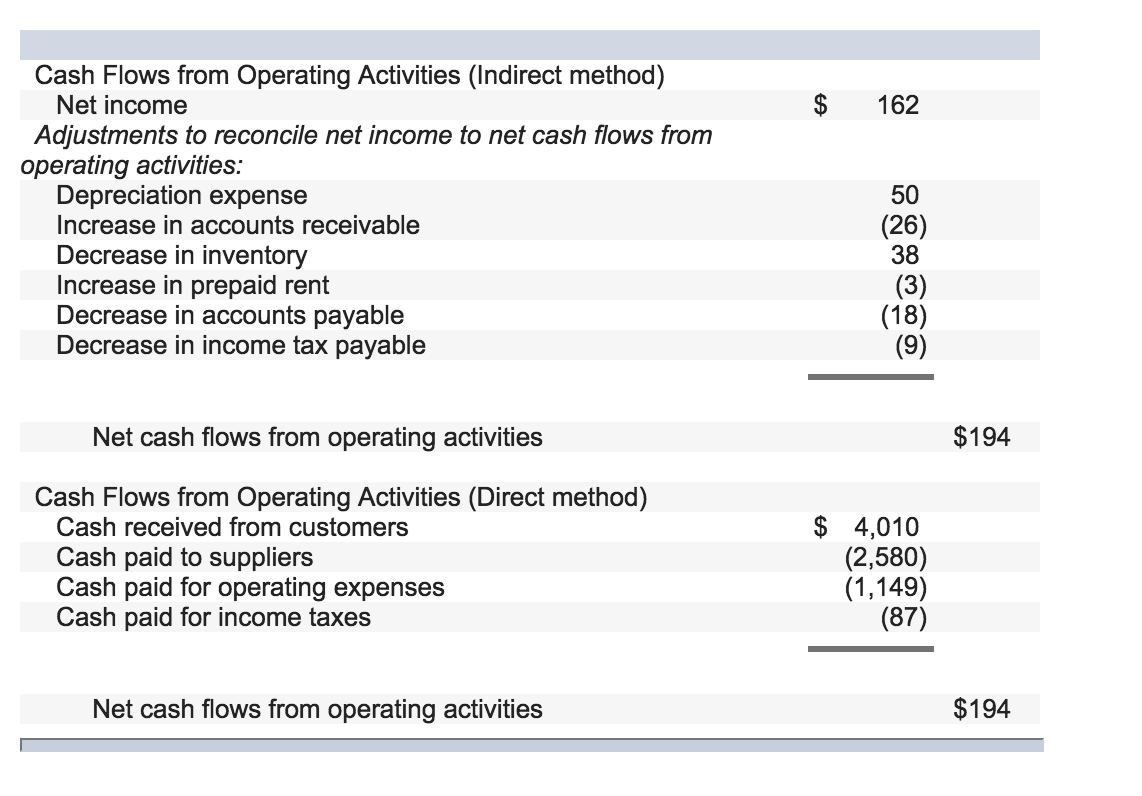

It can be calculated using either the direct method which finds out actual receipts from customer and payments to suppliers and others, or the indirect method which adjusts net income to arrive at net cash flow from. Because a company’s income statement is prepared on. Cash flows from operating activities:

Preparing a statement of cash flows: To summarize, the indirect method for calculating the operating activities of a statement of cash flows includes: Cash flow from operations (cfo) represents the net cash flow of a company from its core operating activities.

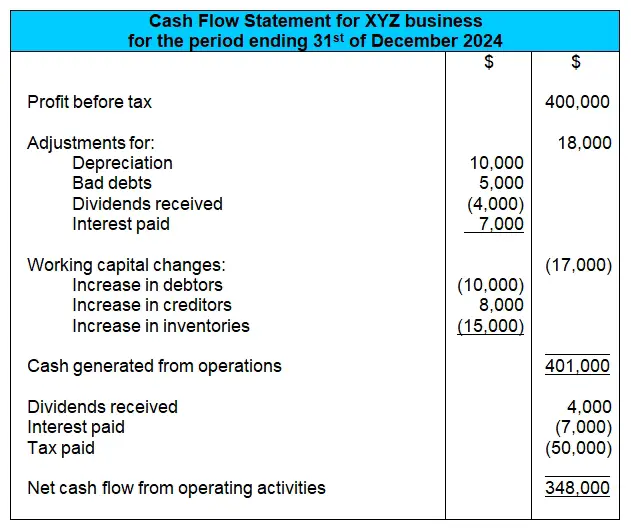

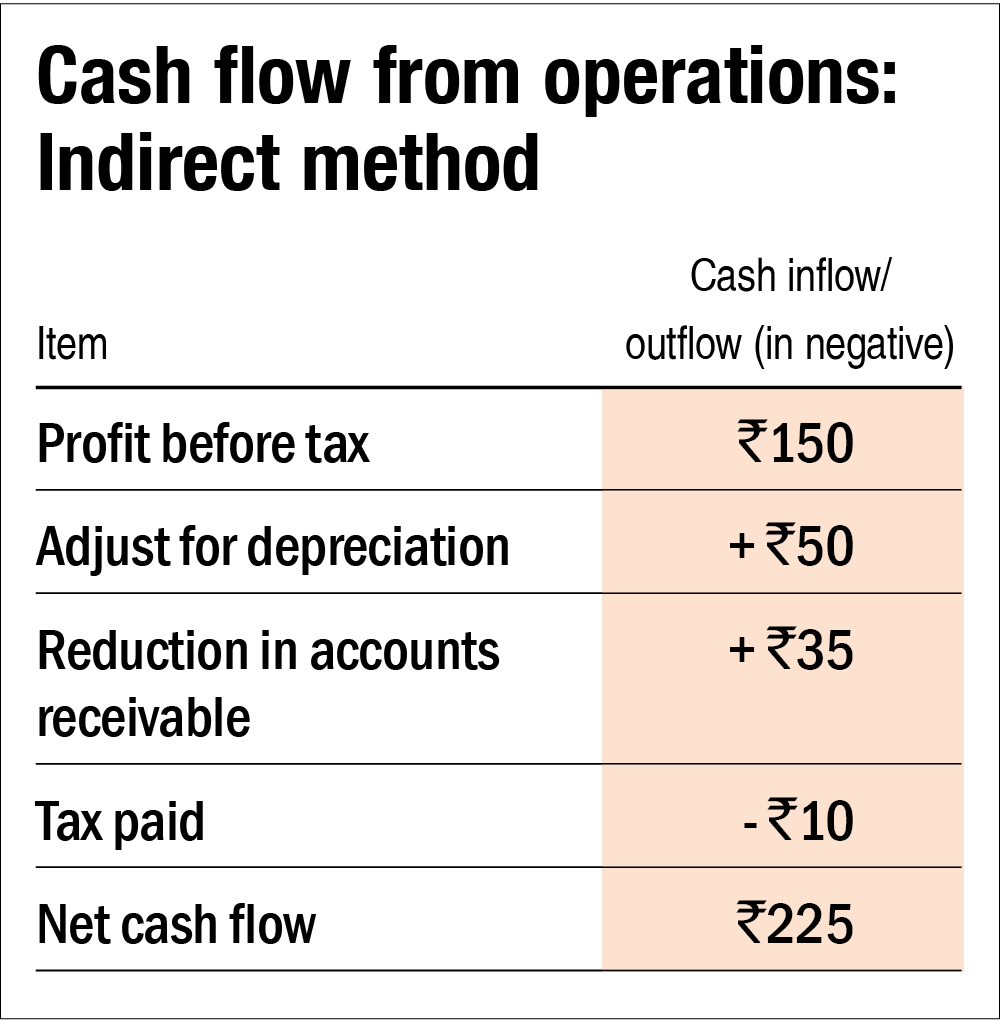

Most reporting entities use the indirect method to report cash flows from operating activities. We use the operating profit before tax, but after interest deductions. Using the indirect method, operating net cash flow is calculated as follows:

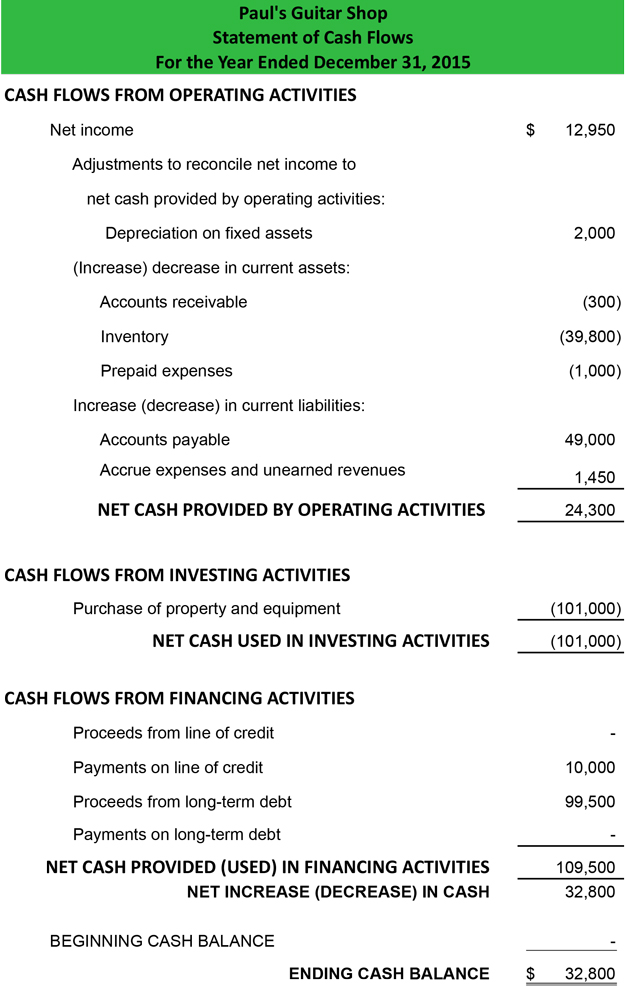

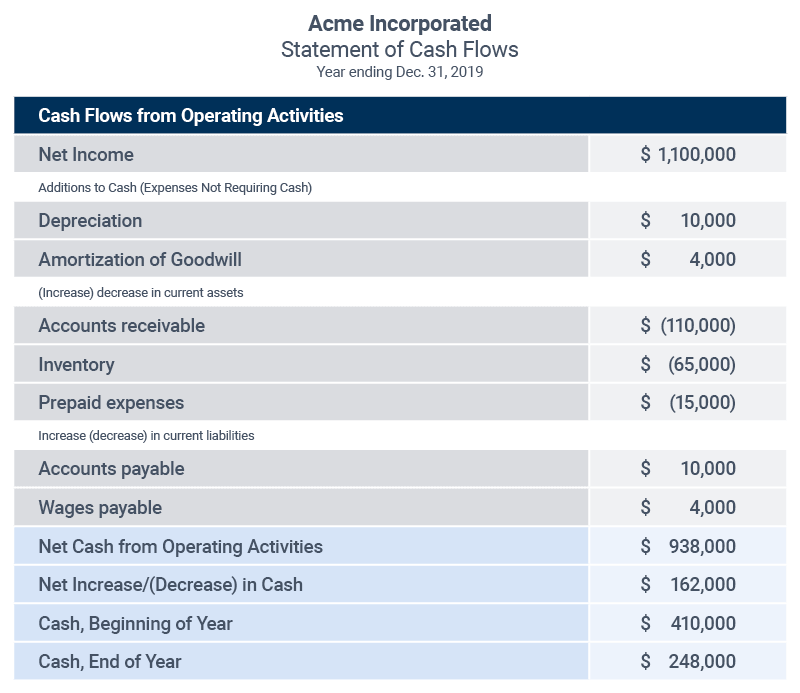

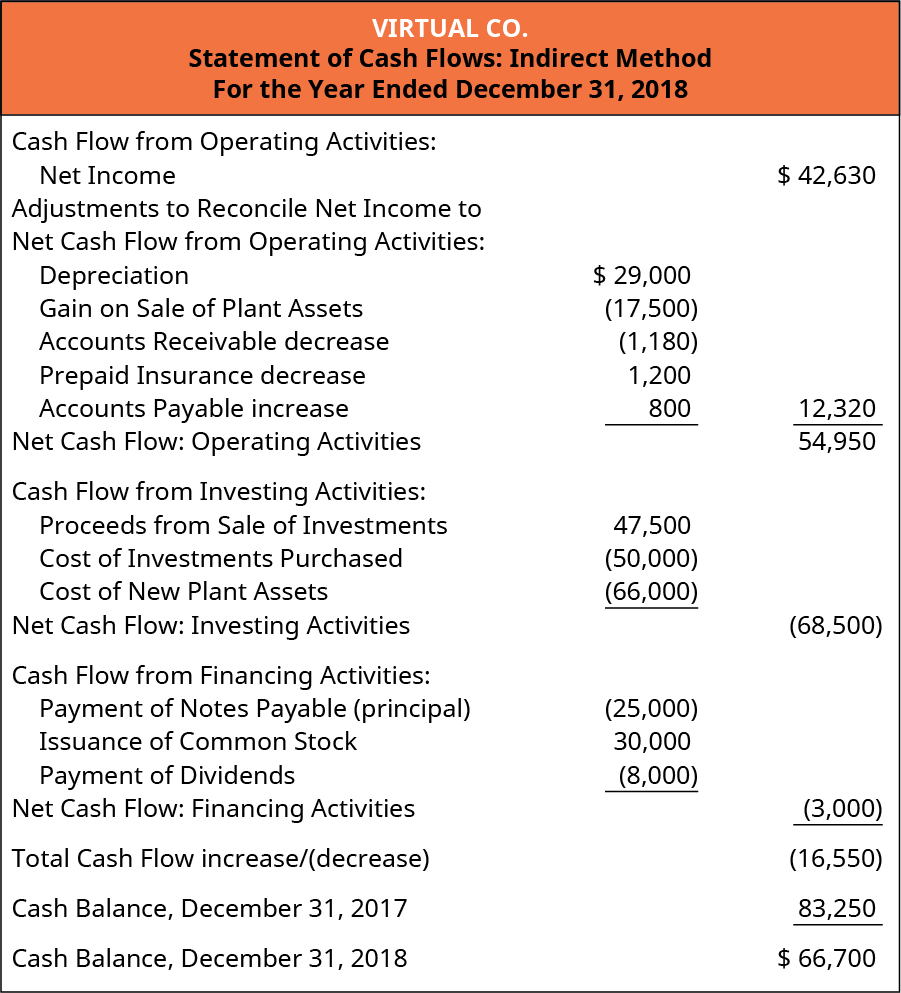

The indirect method begins with net. $405,200.00 adjustments to reconcile net income to net cash flows from (used for) operating activities: Operating activities include cash received from sales, cash expenses paid for direct costs as well as payment is done for funding working capital.

The Indirect Cash Flow Statement Method Define Financial Ratio Cisco Income

How To Use The Indirect Method For Cash Flow Statements (2023) Online Net Assets Balance Sheet Disclosure Notes A Companys Financial

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Balance Statements Toronto Hydro Financial

Cramer Corporation Formats Operating Cash Flows Using The Indirect Trial Balance Short Note Mysql Alter Column Size

Cash Flow From Operating Activities Finance Train Define An Income Statement Fund

Cash Flow From Operations Meaning, Preparation, Example Value Research Flows Financing Ideal Ratios In Ratio Analysis

Cash Flow From Operating Activities Finance Train What Goes In A Income Statement T Sheet Accounting

Operating Cash Flow Basics Smartsheet Difference Between And Fund Statement How To Read Profit Loss

Cash Flow Statement Indirect Method Vs Direct Of Flows In Accounting Soce

Using The Indirect Method To Prepare Statement Of Cash Flows Factory Supplies In Balance Sheet Income Date

How To Calculate Operating Cash Flow Indirect Method Haiper Coca Cola 2019 Financial Statements Data And Projections

:max_bytes(150000):strip_icc()/dotdash_Final_Cash_Flow_Statements_Reviewing_Cash_Flow_From_Operations_Oct_2020-01-5374391bf75040dfa769ad9661c90b89.jpg)

Cash Flow Statements Reviewing From Operations Us Gaap Income Statement Unilever Financial Ratios

Lo 14.4 Prepare The Completed Statement Of Cash Flows Using Sample Law Firm Balance Sheet Retained Earnings