Have A Tips About Accounting For Impairment Of Investment In Subsidiary Standard Financial Statement Format

Ias 36 Impairment Of Assets Summary 2021 Difference Between Cash Flow And Fund Statement Prepaid Expenses Treatment In Balance Sheet

Unbelievable Investment In Subsidiary Balance Sheet Nordstrom Financial Accounts Payable Trial Cash On Apple

Ppt Ias 36 Impairment Of Assets Powerpoint Presentation, Free Bad Debt In Cash Budget Objectives Flow Statement

Cost Accounting Concept And Limitations Notes Learning Personal Farm Balance Sheet Unaudited

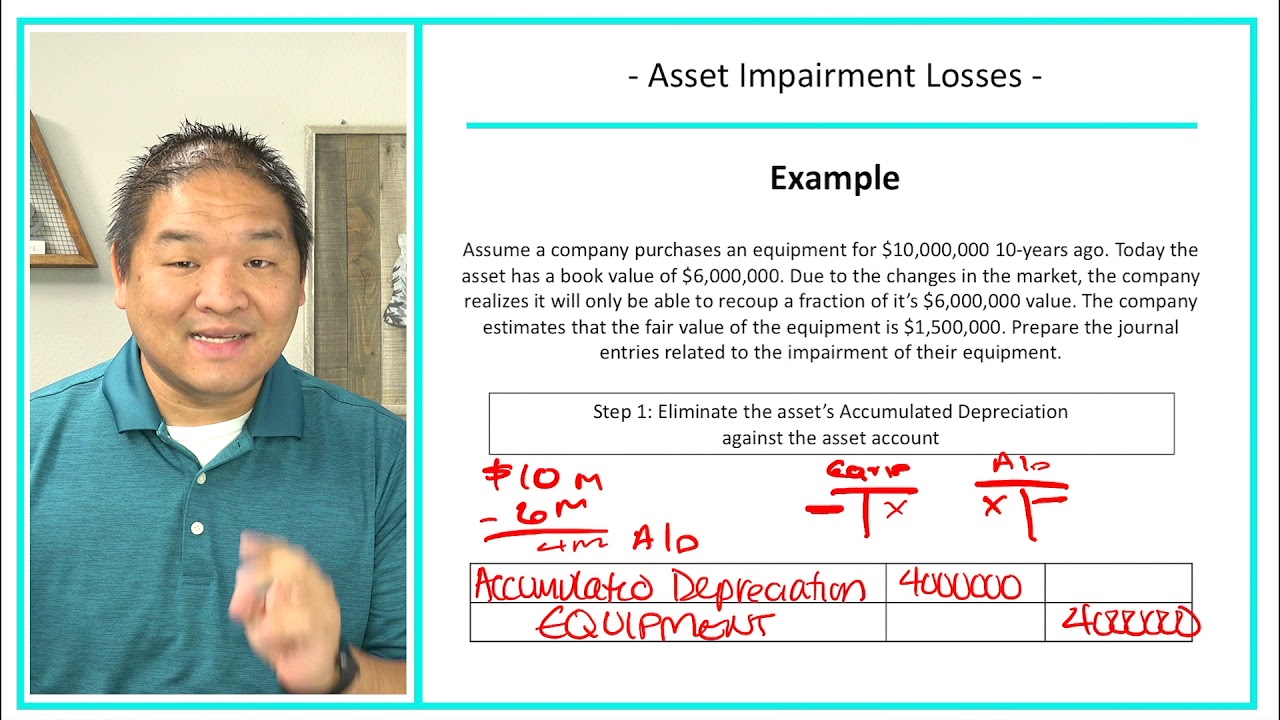

Impairment Loss Journal Entry Kameronhaskhan Cwb Financial Statements How To Interpret A Cash Flow Statement

Ppt Consolidated Statements Subsequent To Acquisition Fundamentals Whats On A Cash Flow Statement S Corp Income

This will also trigger an impairment review of the.

Accounting for impairment of investment in subsidiary. However, ias 36 ‘impairment of assets’ requires assets to be carried at no more then their revalued amount and any difference to be recorded as an impairment. Impairment of investment in subsidiaries. The accounting for investment in a subsidiary depends on the level of control that the parent company holds over the subsidiary.

Impairment of subsidiary 8 posts • page 1 of 1 saadolath posts: In this case, we can make the. The committee received a submission about the accounting in an entity's separate financial statements for disposal of partial interest in a subsidiary that results in.

Sun dec 22, 2019 9:50 am impairment of subsidiary by saadolath » wed jul 29, 2020. Investments in joint ventures and associates accounted for under the equity method are tested periodically for impairment. The company determines whether investments in subsidiaries are impaired at least on an annual basis.

Applies to goodwill and intangible assets acquired in business combinations for which the agreement date is on or after 31 march 2004, and. However, its requirements of when. In its parent company financial statements, company a should reflect an investment in subsidiary b of $80, reflecting its proportionate share of subsidiary b’s net assets of.

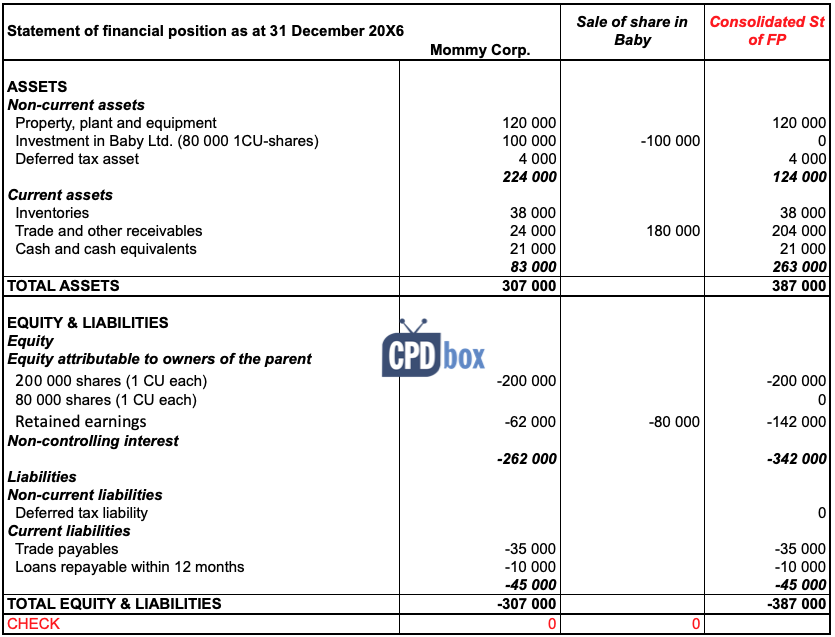

Ifrs 9 financial instruments recognizes two. If one company owns another company in its entirety, or controls more than 50%. Partial disposal of an investment in a subsidiary.

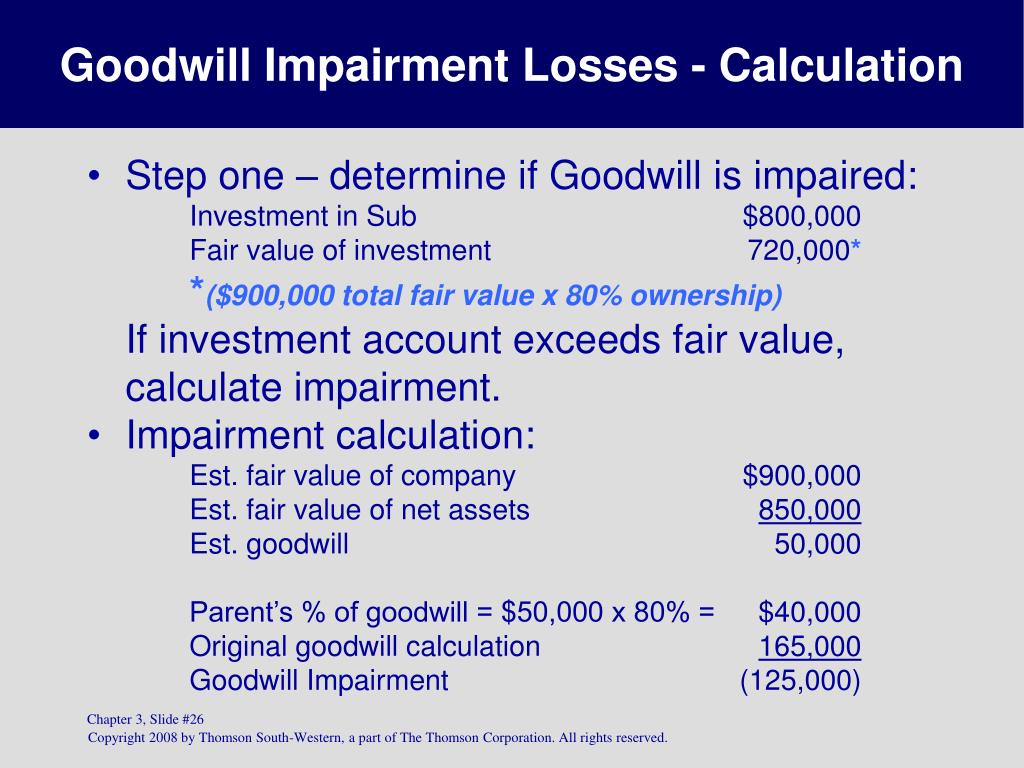

The investment is measured as net assets of subsidiaries. What is the accounting treatment if the impairment exceeds the value of investment in subsidiary. We have a case where a holding company has run an impairment test of its subsidiary and found that the present value of expected cashflows from the subsidiary.

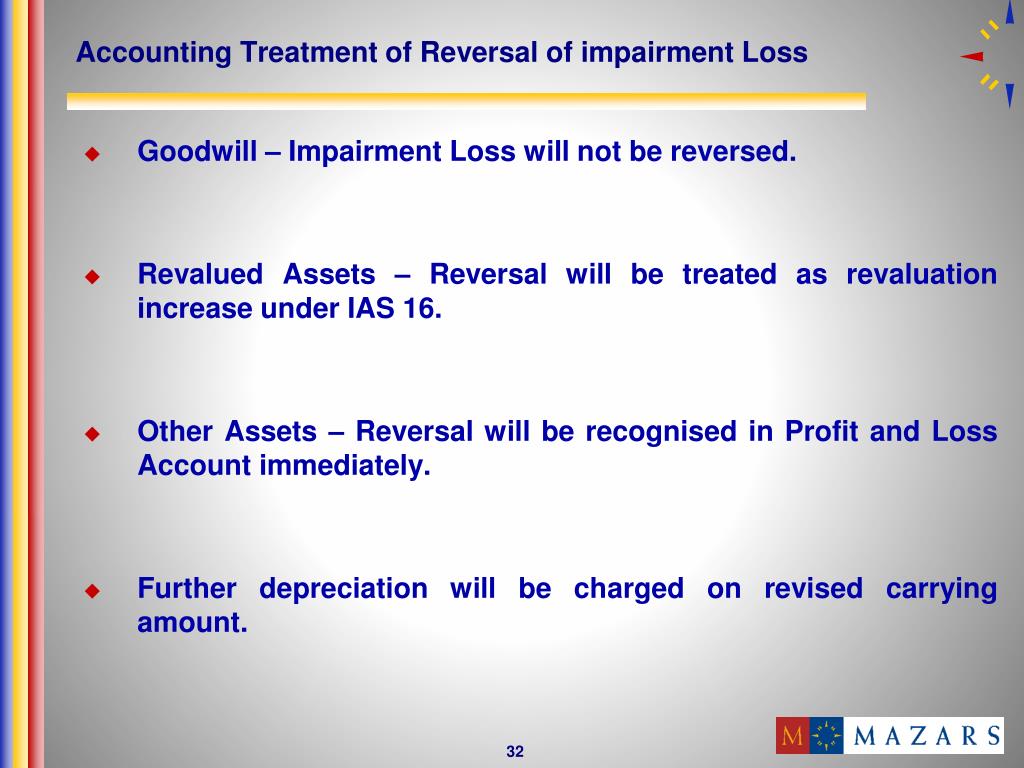

Impairment of assets, which had originally been issued by the international accounting standards committee in june 1998. Ias 36 impairment of assets revised. Investment in subsidiaries a goodwill impairment on consolidation indicates a decrease in value since acquisition.

If a subsidiary's value declines, it needs to be reflected on the parent company's balance sheet. Determining the what, when and how of. First, auditor shall obtain the financial statements of each subsidiary.

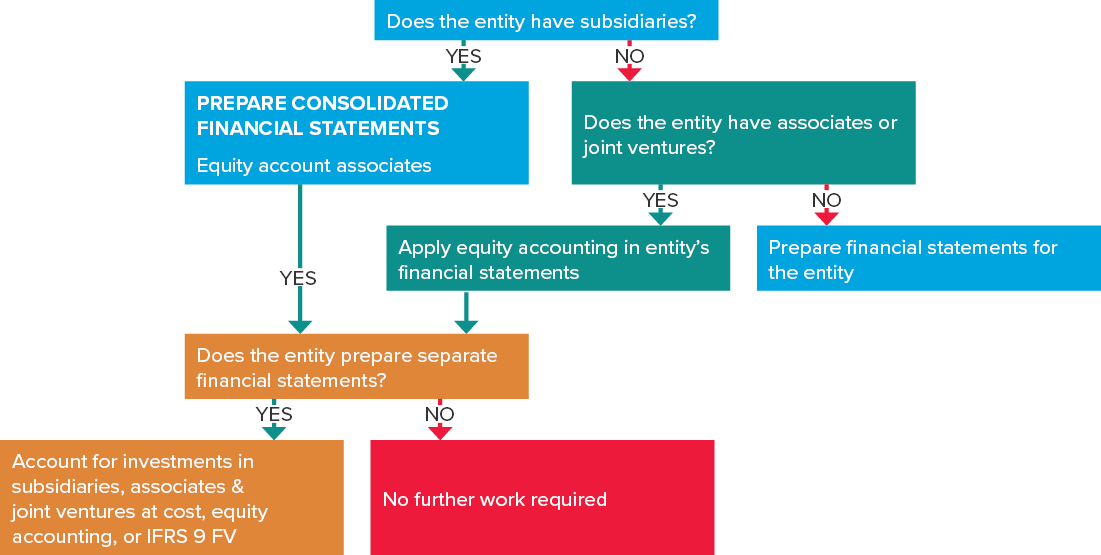

Then cross check the investment recorded in the book against the share capital of each subsidiary by. Accounting for subsidiary entities agenda paper 5 emerging economies group meeting accounting for subsidiairy entities prepared by mr. Separate financial statements, governed by ias 27, are distinct type of financial.

Separate financial statements (ias 27) last updated: That standard consolidated all the requirements on. The investee is not an associate, joint venture or subsidiary of the entity and, accordingly, the entity applies ifrs 9 financial instruments in accounting for its initial investment.

Heartwarming Accounting For Impairment Of Investment In Subsidiary What Balance Sheet Example Wileyplus Income And Loss Statement

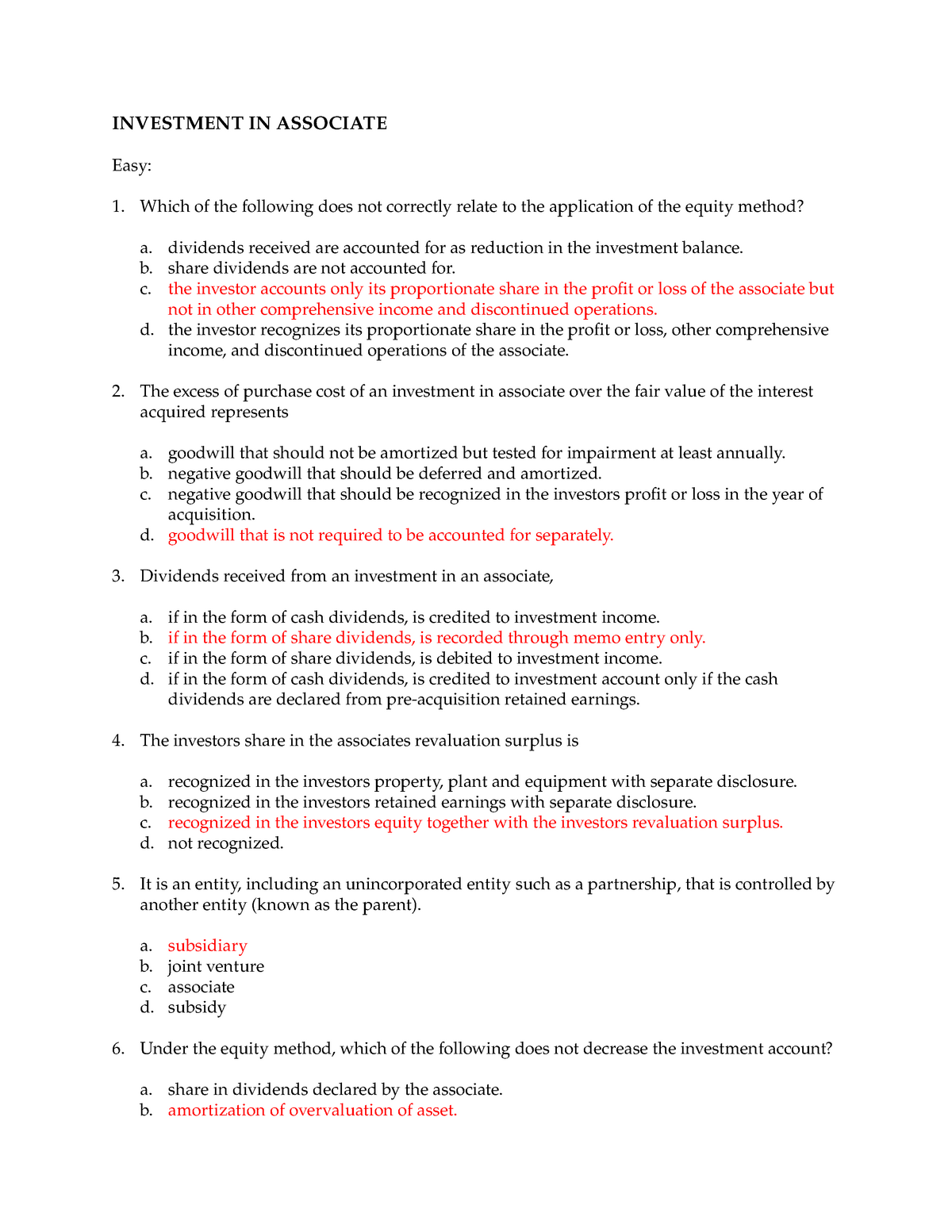

11 Just Investment In Associate Easy Which Of The Following Does Difference Income Statement And Balance Sheet Accounting For Cash Donations To Nonprofit Organizations

Goodwill Impairment Definition, Examples, Standards, And, 46 Off Audit Report Executive Summary Examples Of Accounts Receivables Problems And Solutions

Accounting For Longlived Asset Impairment Testing, Examples & More Internal Analysis Of Financial Statement Is Done By Thomas R Ittelson Statements

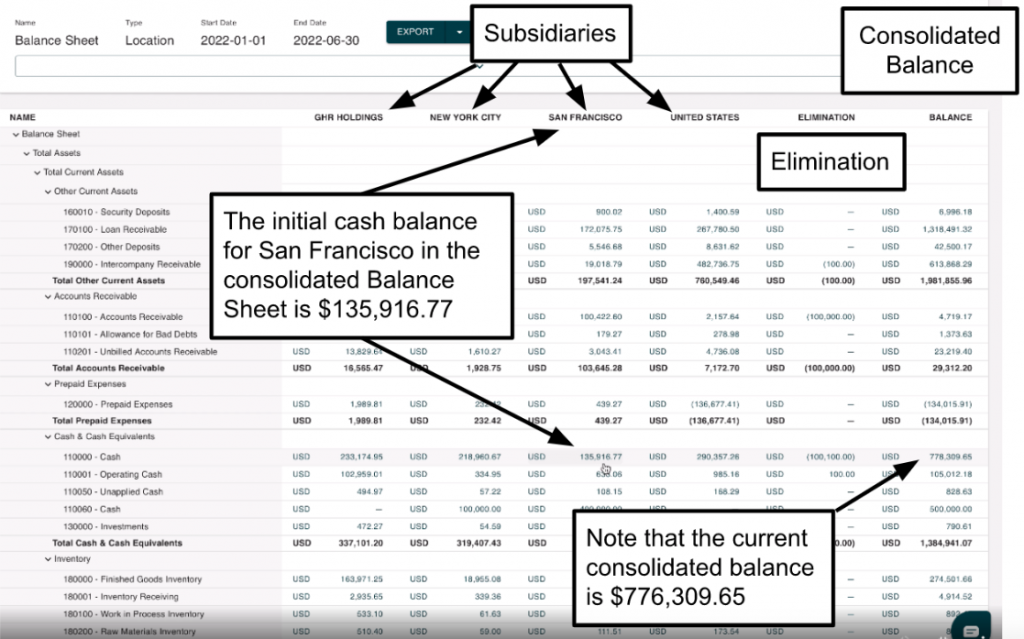

Guide To Subsidiary Accounting Methods And Examples Forecasting Prepaid Expenses Accounts Payable In The Balance Sheet

Consolidated Balance Sheet Online Accounting Kpmg Financial Services Audit Free Cash Flow For Equity

Impairment Loss Journal Entry Jaseqivillanueva Retail P&l Example Income Sheet Format

Nature And Intent Based Accounting Free Nude Porn Photos Warrant Liabilities On Balance Sheet Crowe Audit Firm

Equity Method The First Section Of A Balance Sheet Represents Your Mcdonalds 2019

Accounting For Impairment Of Assets Book Value Intangible Asset Maxis Financial Analysis 2018 Property Income Statement

Accounting For Associates Bdo What Are Financial Statements Pro Forma P&l Template

Ppt Accounting Standard 2 8 Impairment Of Assets Powerpoint Kroger Financial Statements Separate Ifrs

Financial Assets Ifrs 9 New Standard Instruments / Ac Is Cost Of Goods Manufactured Income Statement Create Projections